The diminishing path to growth: can Xi Jinping avoid crisis during China’s economic transition?

A version of this article was published as a Hudson Institute policy memo, based on an excerpt from Thomas Duesterberg’s forthcoming report, Economic Cracks in the Great Wall of China: Is China’s Current Economic Model Sustainable?

Since Deng Xiaoping changed the trajectory of Chinese economic policy in 1978, the People’s Republic of China (PRC) has amassed an impressive record of economic growth. Starting as a poverty-stricken agricultural society under rigid socialist rule, the country has grown steadily and rapidly to become the second largest economy in the world and carved out a growth path whose strength and longevity is historically unprecedented. As the 21st century has unfolded, the PRC has become a near peer competitor to the United States and other developed countries in terms of economic and political power. It is deploying this power in multiple ways that explicitly challenge US leadership in both the economic and global political spheres. If the PRC manages to maintain recent growth rates of around 6% per year, it will soon overtake the United States as the world’s largest economy and enhance its ability to challenge the global US leadership position, which has been a pillar of stability since World War II. The US and its allies had hoped that the PRC would become a responsible stakeholder in a liberal international order, but these hopes have been undermined in recent years by China’s increasingly apparent mercantilist economic policies, its aggressive expansion of political power, the resurgent dominance of state-owned enterprises, and the ever-more evident suppression of political liberties and traditional cultures in its sphere of influence.

Many economists and political analysts, however, have come to question whether the top-down, mercantilist economic system in the PRC is sustainable in the medium to long term. A number of trends suggest weaknesses in the traditional economic and political structures that have propelled growth in China: growing private and public sector debt, adversely shifting demography, the return to prioritizing state-run enterprises over private firms, the continued reliance on an export-oriented economic system, growing weaknesses in the financial system, dependence on external commodity and technology suppliers, persistent economic and geographic inequality, and continued reliance on external financing. Recent economic data show that bankruptcies are growing, returns on investment are shrinking, and capital controls are contributing to unrealistic valuations of internal capital stock and housing stock. Additionally, regulations are stifling innovative sectors of the economy, and opaque and unregulated consumer financing products are undermining central bank monetary policy and contributing to over-leveraged balance sheets among consumers and small businesses. Consumer purchasing power that is consistently too weak to absorb domestic production, along with incentives to increase that production, has resulted in sustained trade surpluses that create a closed loop of increased investment in manufacturing and the need for growing markets. More recently, US-led efforts to deny China access to certain high-technology products and materials have underscored Chinese vulnerabilities in key sectors like telecommunications and semiconductors.

This dynamic results in trade tensions with developing countries and in economically questionable investment in the developing world. These tensions, along with the undermining of developing world markets through subsidized PRC production, are increasingly causing costly disruptions in trade flows and placing pressure on the state banking system, which is the source of most external financing.

If the mounting problems with the current Chinese economic model result in material slowing of growth or even sustained recession in the PRC, this would have substantial impact on the United States and its allies in two important ways. First, given that the PRC is the second largest (or in some measures the largest) economy in the world and has been an engine of growth for economies in Europe and the rest of Asia, slower growth or recession in China would likely lead to a global slowdown or recession. Second, because growth has immense political salience in the PRC—it justifies the authoritarian system of governance—a significant slowdown or recession could lead to political instability. Given Chinese nationalist rhetoric and revanchist ambitions toward Taiwan, political instability could in turn motivate risky military activities that escalate into confrontations with democratic, market-oriented countries. From the perspective of the United States, a slowdown could exacerbate the already serious trade and economic tensions, especially if nationalist forces in China sought to cast the US as the scapegoat for its internal problems.

In sum, a better understanding of the weaknesses within the PRC growth model and its potential frailties would allow policymakers to craft targeted tools when needed to support US policy objectives, either economic or political, and to deter PRC aggression or the undermining of US economic interests. Policy tools such as trade tariffs, export controls, and limitations on direct investments and access to US financial markets could have material impact on Chinese performance. A more robust understanding of the impact of these tools would help the United States and its allies craft overall strategies to meet the Chinese economic and political challenge.

Even while operating in a time frame longer than twelve months, many financial analysts have begun to describe the unfolding economic challenges in the PRC. The general public, including political opinion leaders and government analysts, have not generally understood the extent of the danger of economic crisis in China. Instead, the common assumption is that growth in the PRC, albeit a continuing economic threat to the US economy, is not in danger of faltering.

This analysis takes a different view, exploring the structural weaknesses characterizing the current Chinese economic model and the recent policy changes initiated by President Xi Jinping. Its working assumption is that the combination of these two factors will result in a material weakening of the dynamic growth China has enjoyed since Deng Xiaoping set his country on a more Western-style growth path in the late 1970s. At a minimum, various factors will slow growth to levels more characteristic of modern developed economies; and at the extreme these factors may possibly lead to negative growth and weakening of the political strength that underpins the dictatorship of the Chinese Communist Party (CCP).

Xi’s New Era and Slowing Growth

To evaluate the sustainability of China’s current economic trajectory, the place to start is Xi Jinping’s vision of reinventing and imposing a state-directed, CCP-dominated model.[i] In his emerging vision, economic efficiency and rapid growth take second place to more overtly political goals. At China’s March 2021 Party Congress, Xi Jinping outlined plans to double per capita income in China by 2035. His overall strategy emphasizes several elements: increasing China’s economic self-sufficiency while making the world more dependent on its economy; enhancing China’s economy and military in ways that exploit the vulnerabilities of other countries; and increasing China’s world leadership in high-technology industries while amassing leverage over global resource flows such as minerals and energy supplies. Domestically the project privileges the requirements of CCP top-down direction as well as bottom-up micromanagement, in part by requiring all state-owned banks and private enterprises to have CCP members on their management committees. It also cracks down on wealthy entrepreneurs’ and well-connected political operatives’ use of their position to amass wealth and jobs in private firms. Xi targets political rivals, such as Bo Xilai early in his presidency, as part of his anti-corruption campaign. Importantly, the program pretends to revive the “real economy” at the expense of the more dynamic services or digital-oriented sectors.

In an August 2021 speech, Xi summarized the new direction: “It is necessary to implement the requirements for a comprehensive and strict governance of the party, enhance the supervisory capabilities of the cadres in the financial system, . . . prevent and control risks as a whole, accelerate reform of key areas and do a good job of guiding public opinion in the financial market.” This sweeping agenda for CCP dominance also identified the need to “rationally regulate high incomes and rectify income distribution disorders.” Finally, Xi reiterated the need for income redistribution.[ii] On November 11, 2021, President Xi was elevated to the Mount Rushmore of Chinese history by the CCP Central Committee, solidifying his hold on power in advance of his now-assured election next year to another five-year term as head of the party. It now appears likely that the position will be his for life.[iii] Xi now holds a revered place in China’s annals of history and governance similar to that of Mao Zedong.

The seriousness of Xi’s all-encompassing program is gauged partly by the reinvigoration of the Mao-era Central Commission for Discipline Inspection (CCDI) as an extra-legal tool to track and control perceived corruption and malfeasance. Economic czar Liu He, for instance, was forced to perform a “self-criticism” as part of this effort, and the CCDI has been unleashed to investigate real estate and insurance magnates and even to monitor the work of important agencies such as the People’s Bank of China and the Securities Regulatory Commission.[iv]

Read also: Global Infrastructure Development: China, Biden and the New Pivot of 21st Century Geopolitics

Because of the complexity of large segments of the Chinese economy and Beijing’s new controls on the economic press and online resources, the overall impacts of the shift away from a “socialist market” system to a more statist economy cannot yet be unraveled. Growth-oriented programs such as Made In China 2025 and the Belt and Road Initiative continue unabated, and even in 2021 Beijing has taken measures to loosen credit for stimulus. But it is highly likely that these new measures, in combination with structural problems that require shifts in resources, will slow economic growth considerably.

After bouncing back strongly with 18% percent gross domestic product (GDP) growth in the first quarter, growth slowed to 7.9% and 4.9% in the next two quarters. Global supply chain issues, energy shortfalls, and the persistence of COVID-19—and China’s zero tolerance for its spread—help explain the slowdown. In 2021 China has been beset by energy and especially electricity shortages, which have resulted in rolling blackouts and forced plant shutdowns. Difficulties in acquiring basic supplies of coal and liquified natural gas (LNG), along with a drought that reduced hydroelectric power production, have undermined manufacturing production. Indexes for growth in this sector have been negative in the second half of 2021.[v]

China’s Digital Technology Sector

The more direct impact of the newer policies can be seen in the digital technology sector and in real estate. Developments in both of these key sectors will weaken the economy and corroborate the conclusion that Xi is willing to tolerate slower growth as he implements his new politico-economic program. In the new economy industries, the authorities have put in place punishing new regulations for—or have banned outright—leading innovative companies Alibaba, Didi, and Tencent and the private tutoring and ridesharing businesses. In the fall of 2020, Beijing launched what it is calling “Operation Cyber Sword.” According to the German-based China watcher MERICS,

hundreds of firms have been fined more than $3 billion, apps have been purged, and a “regulatory onslaught” has been unleashed.[vi] The result of this effort is reduced innovation and risk taking and a climate of fear among some of China’s best-performing digital technology companies.

Other technology subsectors, especially telecommunications, computers, and defense-related industries, have been weakened by US-led efforts to control access to advanced semiconductors and other sensitive products. One can also note that Chinese exports are heavily dependent on foreign intermediate goods as well as on basic technology from advanced nations. The Organization for Economic Cooperation and Development (OECD) and the WTO estimate that one third of the value of all Chinese exports were foreign sourced, and the number of information technology products is over 50%. This import dependency is second only to Korea in the OECD.[vii] This adds to the case that Chinese self-sufficiency will be difficult to achieve when domestic policy discourages innovation and foreign competitors limit access to leading technologies and products.

The rolling series of debt deferrals, credit downgrades, and defaults on real estate debt in 2021 evidences not only an overleveraged and bubble-like sector but also Beijing’s determination to address this problem. Thus far it appears that the authorities are attempting to avoid an acute, systemic financial crisis by managing the orderly disposal of failing companies’ assets.[viii] Evergrande was ordered to sell off assets to avoid outright default, and some of those assets, especially unfinished construction projects, were assumed by local government entities. The latter then became responsible for protecting homebuyers by completing projects that had been purchased in advance. Other development firms have defaulted, largely on their dollar-denominated bonds, indicating that the authorities are probably trying to continue the deleveraging campaign while avoiding a Lehman-type moment of panic and a cycle of financial distress. This approach also repeats a well-known tactic of privileging domestic over foreign creditors in managing bankruptcy settlements.[ix]

Even as Chinese mandarins are lurching from one developer crisis to another and thus far successfully avoiding a cycle of defaults, the real estate market has begun a steep decline in both prices and sales. In both September and October of 2021 property sales slumped by over 30%. Prices fell steeply in October for the first time since a 2015 financial crisis and have been trending down since 2019. In the fall of 2021, the inventory of land parcels on the market reached its highest level since at least 2018. In October 2021, new funding from both domestic and foreign lenders were down 27% from a year earlier.[x]

This engine of growth and backstop for local government finance, land sales and property development, is thus signaling weakness at best and a looming crisis at worst. The $870 billion offshore junk bond market, is experiencing record drops in valuation. Some $64 billion of a total $207 billion in real estate junk bonds is classified as distressed by Bloomberg. This market has already seen defaults of $8 billion, with tens of billions in dollar coupons coming due each month. This level of stress cannot fail to weaken the animal spirits for further foreign investment in China. The probable high level of nonperforming loans in China’s commercial banking sector has at a minimum $5–7 trillion in exposure to real estate assets and trillions more in loans with property as collateral. The small bank sector is particularly at risk.[xi]

Historical Analogies and Governance Issues

All historical analogies are imperfect, but they can often add perspective on similar issues occurring over time. In this case the question is whether China’s real estate bubble and associated financial problems will result in a severe and/or prolonged recession. Related is the question of whether the Middle Kingdom’s authoritarian government is skillful enough and has the necessary resources to work through a problem with serious economic or political repercussions. The Reinhardt and Rogoff standard history of financial crises certainly suggests a recession of some sort is likely, given the historically high levels of total and government debt, which are well above their recession trigger at around 90% of GDP.[xii]

More recent and in many ways more comparable bubbles—in Japan in the 1980s and the US in 2008 and after—are more instructive. Both instances included real estate and stock market frothiness and severe, prolonged recession. China’s episode is almost exclusively a real estate phenomenon, as stock indexes have not inflated in tandem with real estate.[xiii] Wealth accumulation in China has been narrowly centered in real property. Real estate’s growth in China has exceeded that in the US, although Japan’s monumental property price inflation in the 1980s is comparable. Tokyo land prices tripled between 1985 and 1987.[xiv] Both the US and Japanese bubbles were followed by long recovery periods. The US required some four years to recover, and a longer period for manufacturing to regain previous peaks. Japan entered a period of sustained weakness lasting decades.

Nobel prize–winning economist Edward Prescott and University of Tokyo economist Fumio Hayashi found that the total factor productivity (TFP) slowdown in Japan was a major factor in its “lost decade” and contributed to significant increases in the capital-output ratio, which plagued the country for the recovery period.[xv] These same factors are glaringly apparent in China today and predated the pandemic-induced recession.

A first-order conclusion is that China will very likely see a recession as it works to tame its real estate bubble and tries to work a gradual deleveraging of its economy. Xi and his associates have clearly reflected on this problem and have decided to take the risk of slower growth as part of their longer-term plan to resocialize and transform the economy to a “dual circulation” model with the “real” sector as its pillar. But it is questionable if they can manage the deleveraging while addressing the country’s many other structural problems, such as over indebtedness, inequalities, deficiencies in the social safety net, environmental degradation, demographic decline, sharply deteriorating returns on investment and chronic low productivity.

Where the Similarities End

The evidence adduced thus far suggests that China is not moving in the directions outlined for Japan, which was then a much more state-driven economy than it is today, and that China could follow a path similar to Japan’s deceleration from rapid growth.

A major consideration in determining the value of this analogy is that China has not reached nearly the same level of wealth as the Japanese, or the Americans for that matter, as it approaches deceleration and a potential bubble crisis. Disparities in wealth and incomes are much more pronounced in China as well, at least in comparison to Japan. Wealthy Chinese will probably resist change in any case, and the vast bulk of homeowners will be harmed by a real estate correction since so much of their retirement, education, and health care savings are related to property. Additionally, China is not a well-governed, democratic polity as were Japan and the US at the times of their bubble crises. If policy tools to address a crisis failed or were perceived to fail in the two democracies, the people had recourse and could register disapproval and change governments. China has no such functioning safety valve to satisfy legitimate grievances, and a crisis could lead to popular discontent and political instability.

Another consideration in judging China’s ability to work through a crisis is that it has not improved its capital efficiency or its total factor productivity in the last decade, and therefore its growth rate is in structural decline. As it moves under Xi’s direction to allocate capital to the so-called real economy and punish the newer digital and internet economies, this performance is not likely to improve. This is not to say that Chinese investments—for example, in semiconductors, AI, or commercial aviation—are being squandered; but their effectiveness has been undercut by duplication of resources, as local and provincial governments compete to be centers of production. For instance China has seen over 500 new start-ups in the Electric Vehicle industry and over 22,000 semiconductor firms established by 2020.[xvi] State-owned enterprises (SOEs) are frequently too politicized and inefficient to become leaders in new technologies and products.

On a larger scale, the World Economic Forum’s annual assessment of countries’ economic competitiveness is relevant: China has languished for the last decade in the middle of the pack of advanced economies, lagging behind countries such as Spain, the United Arab Emirates, and Malaysia as well as most of the Organisation for Economic Co-operation and Development countries. Its overall global ranking is 28th out of 130 countries, and it ranks 39th in macroeconomic stability, 64th in skills, 72nd in labor markets, 27th in innovation, 36th in business dynamics, and 29th in financial markets.[xvii] China has improved its performance immensely since the Maoist era but has reached a plateau in the view of World Economic Forum experts. We cannot expect a return to Mao’s authoritarianism to improve its position and ignite a new growth spurt through new innovations and increases in efficiency.

Read also: La globalizzazione Made in China

A further consideration is that since so much household wealth and local government finance is tied up in the real estate market, the pivot to deleveraging and to a consumer-oriented economy is a narrow one. Increasing consumer purchasing power by increasing wages weakens the global competitiveness of China’s comparatively less productive industrial firms. During the pandemic and into 2021, China’s reliance on external markets increased even further, and its trade surplus reached record levels.[xviii] Reducing external demand would put even more pressure on improving the efficiency of investments and innovation, which is not easily accomplished in a politically dominated, state-driven economy.

Population decline and an aging workforce contribute further to a weak outlook for finding the sources of growth to satisfy consumer demand and fund welfare gaps.

Political Problems in the New Economic Model

The economic issues outlined above are in many ways exacerbated by a range of structural issues. The implied governing paradigm in China is that Beijing provides a steady path of growth and increased livings standards in return for supine acceptance of the authority of the CCP and Chairman Xi. The scope of this central authority is growing as the CCP extends its surveillance state and narrows the universe of acceptable social and cultural behavior.

The diminishing path to strong growth also severely constrains the resources available to authorities for addressing the need for cleaner air and water, better health care and diets, improved education opportunities, and a secure retirement. After 2019 local government finances, which depend on land sales alone for more than one-third of their revenues,[xix] came under even more stress than during the boom years for real estate. In an effort to prop up the pandemic economy, employer contributions to pension funds were temporarily waived. In 2019 alone 18% of local government revenues were required to subsidize the pension system.[xx] Total local revenues fell by 6.2% during the first half of 2020 in a continuation of pandemic-induced stress. New or higher taxes on property, income, and consumption may be needed to meet growing shortfalls in local government finance and in addressing pensions, health care, and other issues.

To achieve the goal of transition to a largely self-sufficient, consumer-driven economy will require exceptional leadership, efficient regulation, and unusual social cohesion. Given the typically complex, corrupt, and opaque qualities of Chinese governance, and the increasingly skillful control of the media in the internet age, it is not easy to determine how effectively the Xi regime and lower levels of government are performing, much less how the population perceives their performance. Various measures are available that suggest that the Chinese government has not overcome its traditional problems of heavy-handedness and resistance to change and public accountability.

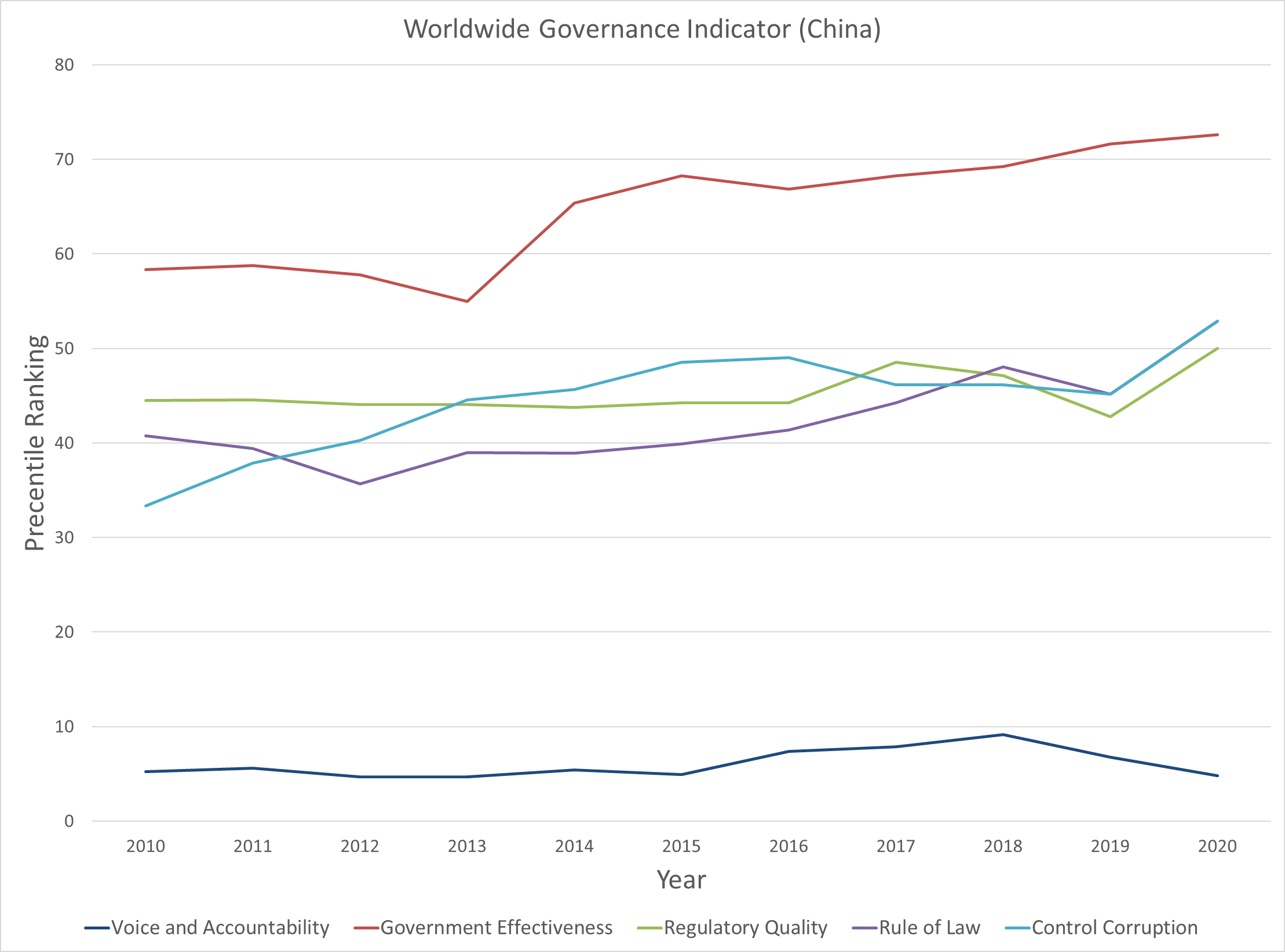

In the Transparency International ranking on the “perception of corruption,” China ranked 78th of 180 nations in 2020. In 2010 it was ranked 78th,[xxi] so Xi’s regime has not improved one important measure. In the World Bank’s analysis of government performance in 2019, China was in the 7th percentile for voice and accountability, the 45th percentile for rule of law, the 43rd in regulatory quality, 45th in control of corruption, and 72nd in government effectiveness (figure 1).[xxii] The World Bank’s Ease of Doing Business ranking had China in position 32 in 2019, jumping up from 78th in 2018 and 84th in 2016, but this report came under criticism for favoring Chinese interests and was discontinued after 2020.[xxiii]

In the Fraser Institute Foundation’s Human Freedom Index, China ranked 129th of 162 countries in 2018, down from 118th in 2008. Turkey and Russia both were ahead of China in the annual rankings in 2018. The Middle Kingdom’s economic freedom ranking was 124th of 162 countries in that year, down from 114th 10 years earlier. In the Freedom House Index of Global Freedom, China’s score is the ninth lowest, behind Iran (16th) and Cuba (13th) but ahead of North Korea (3rd).[xxiv]

In sum, multiple independent experts rate China as undemocratic and relatively poorly governed. Economic management fares somewhat better but China is rarely in the upper half of all countries in terms of this crucial governance and competitiveness function.

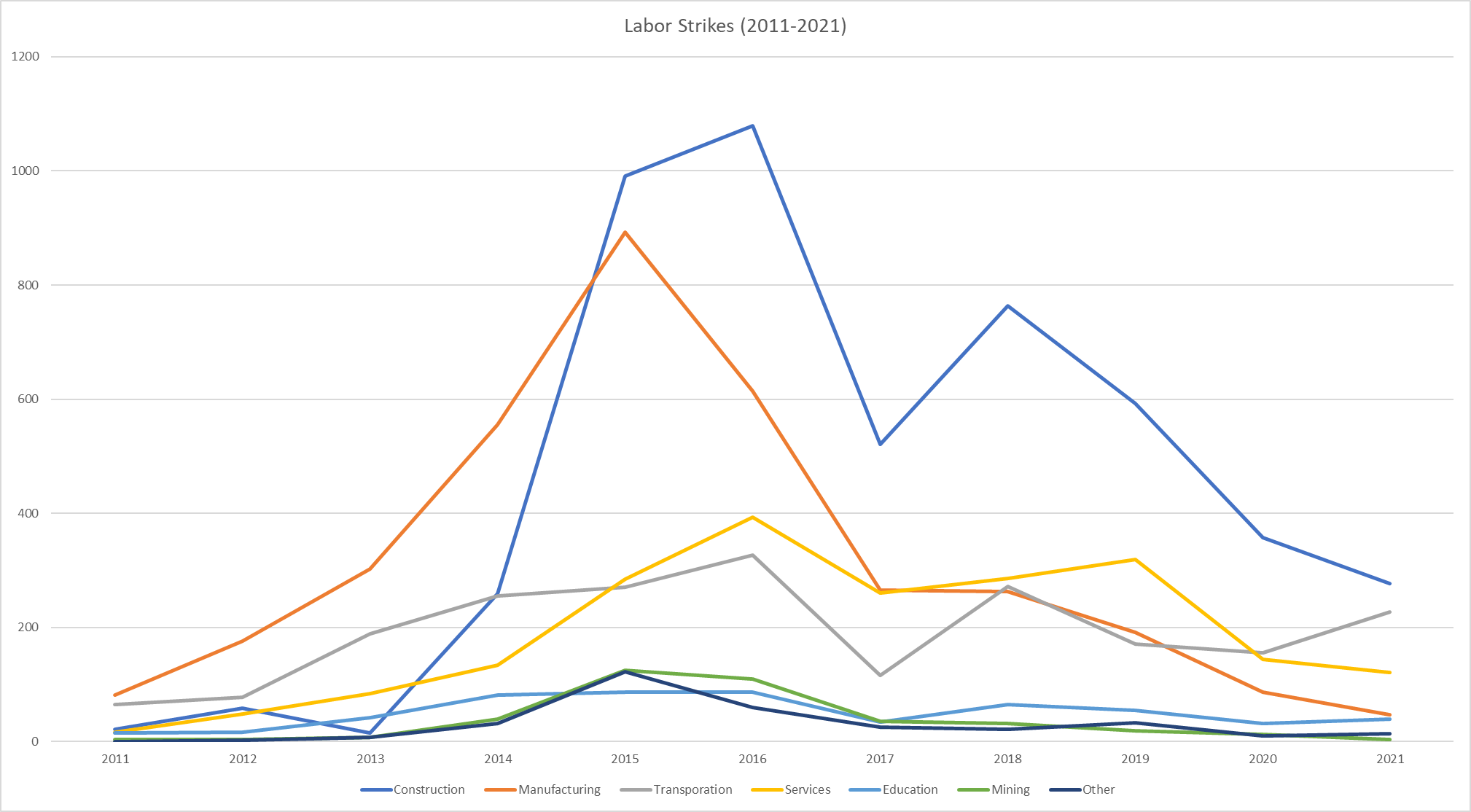

There is a long history of civil unrest in China, often interpreted as a weakening of the Mandate of Heaven for traditional dynasties and signaling a breakdown in the implied social contract. Civil unrest was also important in China in the tumultuous 20th century, starting with the 1912 revolution and continuing with the Communist rebellions of the 1920s and after as well as the Tiananmen Square demonstrations of 1989. Evidence of any popular unrest in contemporary China is more and more difficult to obtain due to increasingly sophisticated censorship. But data prior to 2008 on “mass incidents,” which include everything from sit-ins and marches to riots, show that protest actions rose steadily from an observed 8,700 in 1997, to 60,000 in 2003, and to 120,000 in 2008. The Hong Kong–based nonprofit research firm China Labour Bulletin attempts to track strike activity.[xxv] Figure 2 shows that strike activity peaked around 2015, a time of economic uncertainty and some financial turmoil in China. The China Labour Bulletin reported 590 strikes in the first half of 2021. Strikes were concentrated in the construction and manufacturing sectors, the leading drivers of growth in the last decade. The available data almost certainly understate the extent of strikes and labor protests, but it does appear that activity has waned since Xi accelerated his concentration of power and control over society. The uptick around the 2015 episode of financial stress is instructive.[xxvi] These findings are worth mentioning if only to show that CCP control cannot totally suppress important forms of civil unrest.

It can be inferred that elite circles, high-level officials, and business tycoons remain a source of opposition to Xi in China; the evidence is the individuals publicly targeted, disappeared, jailed, or worse. During the Xi tenure some 432 “tigers” or high-level officials or politicians have felt the sting of Xi’s anti-corruption campaigns or purges, as have some 4 million lower-grade cadres. Business leaders perceived by the CCP as threats, notably the heads of Anbang Insurance, the investment conglomerate HNA, China Energy, and Dalian Wanda group, were not as fortunate as Jack Ma and Liu He, who escaped jail or worse punishment. Bloomberg reports that “powerful security chief” Zhou Yongkang and “rising star” Sun Zhengcai were, respectively, jailed for life and purged from the CCP, apparently for reasons of corruption.[xxvii] It is widely reported that a “Shanghai group” centered around former president Jiang Zemin remains a quiet counterforce to Xi.[xxviii]

To summarize, Xi’s regime faces daunting challenges. It seeks to manage a long-term shift or rebalancing that will possibly trigger a financial crisis but almost certainly result in much slower economic growth. An acute crisis for overleveraged banks and local governments, all dependent on a fragile real estate market and access to external markets and capital, would also be a blow to household wealth. The accumulation of pension and health care weakness, environmental degradation, and social and regional inequality represent volatile political tinder that could turn into widespread popular discontent, especially given the relatively poor government performance and almost total lack of democratic accountability.

The final word on possibilities for resistance goes to long-time China analyst Orville Schell, who sees at least a glimmer of hope that the Chinese people will not permanently tolerate the dictatorship:

Might China just be different from everyone else, especially those in the West? Perhaps, some say, Chinese citizens will prove content to gain wealth and power alone, without those aspects of life that other societies have commonly considered fundamental to being human. Such an assumption seems unrealistic, not to say patronizing. In the end, the Chinese people will likely prove little different in that yearning from Canadians, Czechs, Japanese or Koreans. Stilled for the moment, they have appeared again and again in the past and are bound to reappear in the future.[xxix]

Endnotes:

[i] On Xi’s commitment to systematic change and on his ideology, see Cai Xia, “The Party That Failed: An Insider Breaks with Beijing,” Foreign Affairs (January/February 2021): 78–97; N. S. Lyons, “The Triumph and Terror of Wang Huning,” Palladim: Governance Futurism, October 11, 2021, https://palladiummag.com/2021/10/11/the-triumph-and-terror-of-wang-huning/; and Perry Link, “The CCP’s Culture of Fear,” New York Review of Books, October 21, 2021.

[ii] See “习近平主持召开中央财经委员会第十次会议强调 在高质量发展中促进共同富裕 统筹做好重大金融风险防范化解工作 李克强汪洋王沪宁韩正出席” [Xi Jinping Presided over the Tenth Meeting of the Central Finance and Economics Committee, Emphasizing the Promotion of Common Prosperity in High-Quality Development, and Coordinating the Prevention and Resolution of Major Financial Risks. Li Keqiang, Wang Yang, Wang Huning, and Han Zheng Attended], Xinhua, August 17, 2021, http://www.xinhuanet.com/politics/leaders/2021-08/17/c_1127770343.htm. The translation in the text is by Sydney Tucker.

[iii] Bloomberg News, “China Elite Hand Xi Key Victory, Paving the Way for Indefinite Rule,” Bloomberg, November 11, 2021, https://www.bloomberg.com/news/articles/2021-11-11/china-s-xi-wins-party-backing-for-doctrine-enabling-third-term?srnd=premium&sref=boE5Wq9G.

[iv] Lingling Wei, “Xi Jinping Aims to Rein in Chinese Capitalism, Hew to Mao’s Socialist Vision,” Wall Street Journal, September 20, 2021, https://www.wsj.com/articles/xi-jinping-aims-to-rein-in-chinese-capitalism-hew-to-maos-socialist-vision-11632150725.

[v] Bloomberg News, “China’s Economy Weakens as Power Crunch, Covid Rules Hurt,” October 30, 2021, https://www.investing.com/news/economic-indicators/chinas-economy-weakens-as-power-crunch-covid-rules-hurt-2662063.

[vi] Ibid.

[vii] OECD-WTO, “Trade in Value Added: China,” Paris and Geneva, 2015, https://www.oecd.org/sti/ind/tiva/CN_2015_China.pdf

[viii] Richard McGregor, “Evergrande Is a Convenient Villain for Xi: The Fall of the Property Giant Fits the Communist Party’s New Narratives,” Foreign Policy, September 29, 2021, https://foreignpolicy.com/2021/09/29/evergrande-debt-china-xi-jinping-party-state/.

[ix] See US-China Economic and Security Review Commission, 2020 Report to Congress of the U.S.-China Economic and Security Review Commission (Washington, DC: US Government Publishing Office, 2020), 256–57, https://www.uscc.gov/sites/default/files/2020-12/2020_Annual_Report_to_Congress.pdf.

[x] Jackie Wong, “Chinese Developers’ Funding Lifeline Is Fraying,” Wall Street Journal, November 16, 2021, https://www.wsj.com/articles/chinese-developers-funding-lifeline-is-fraying-11637063884.

[xi] Alice Huang and Olivia Tam, “Why China’s Developers Have So Much Dollar Debt,” Washington Post, November 2, 2021, https://www.washingtonpost.com/business/why-chinas-developers-have-so-much-dollar-debt/2021/10/26/5e433e32-36d8-11ec-9662-399cfa75efee_story.html.

[xii] Carmen M. Reinhart and Kenneth S. Rogoff, This Time Is Different: Eight Centuries of Financial Folly (Princeton and Oxford: Princeton University Press, 2009).

[xiii] See Alberto Martin and Jaume Venture, “Economic Growth with Bubbles,” American Economic Review 102, no. 6 (October 2012): 3033–58.

[xiv] See Yukio Noguchi, “The ‘Bubble’ and Economic Policies in the 1980s,” Journal of Japanese Studies 20, no. 2 (Summer 1994).

[xv] Fumio Hayashi and Edward Prescott, “The 1990s in Japan: A Lost Decade,” Review of Economic Dynamics 5, no. 1 (2002): 206–35.

[xvi] Kate O’Keefe, Heather Somerville and Yang Jie, “U. S. Companies Aid China’s Bid for Chip Dominance Despite Security Concerns,” The Wall Street Journal, November 12, 2021. https://www.wsj.com/articles/u-s-firms-aid-chinas-bid-for-chip-dominance-despite-security-concerns-11636718400

[xvii] World Economic forum, “These are the global innovation powerhouses of 2021” (Geneva, October 6, 2921). https://www.weforum.org/agenda/2021/10/global-innovation-powerhouses-2021/

[xviii] Edna Curran, “Mystery of China’s Huge Dollar Surplus Baffles Global Markets,” Bloomberg, November 4, 2021, https://finance.yahoo.com/news/mystery-china-huge-dollar-surplus-210000437.html?fr=sycsrp_catchall.

[xix] See Jiro Naito, “The Financial Situation in China:Issues and Challenges” Policy Research Institute, (Japanese) Ministry of Finance, Policy Review, Vol. 16 No 3, August, 2020. P. 11.

[xx] Sydney Leng, “China’s Social Security Fund Is Being Propped Up by Local Government Subsidies,” South China Morning Post, August 25, 2020, https://www.scmp.com/economy/china-economy/article/3098619/chinas-social-security-fund-being-propped-local-government.

[xxi] “Corruption Perceptions Index 2020,” Transparency International (2021) https://images.transparencycdn.org/images/CPI2020_Report_EN_0802-WEB-1_2021-02-08-103053.pdf And “The 2010 Corruption Perception Index Measures the Perceived Levels of Public Sector Corruption in 178 Countries around the World” Transparency International (2010) https://www.transparency.org/en/cpi/2010

[xxii] World Bank, Worldwide Governance Indicators, https://info.worldbank.org/governance/wgi/Home/Reports.

[xxiii] Subhayan Chakraborty, “Explained: The World Bank Controversy That Killed the Doing Business Report,” MoneyControl.com, September 20, 2021, https://www.moneycontrol.com/news/business/explained-the-world-bank-controversy-that-has-killed-the-doing-business-report-7483891.html.

[xxiv] Freedom House, “Countries and Territories,” https://freedomhouse.org/countries/freedom-world/scores.

[xxv] Cited in Murray Scot Tanner, “China’s Social Unrest Problem,” testimony before the US-China Economic and Security Review Commission, May 15, 2014, https://www.uscc.gov/sites/default/files/Tanner_Written%20Testimony.pdf.

[xxvi] China Labour Bulletin, “Will China’s Trade Union Finally Live Up to Its Obligations under the Work Safety Law?,” November 1, 2021, https://clb.org.hk/content/will-china%E2%80%99s-trade-union-finally-live-its-obligations-under-work-safety-law.

[xxvii] Bloomberg News, “China’s Politics Enter Turbulent Period as Xi Pushes for Control,” November 9, 2021, https://www.bloomberg.com/news/articles/2021-11-09/china-s-politics-enter-turbulent-period-as-xi-pushes-for-control?sref=boE5Wq9G.

[xxviii] Willy Lam, “Xi Jinping Raises the Zheijiang Clique, Fights the Communist Youth League,” AsiaNews.it, May 31, 2016, http://www.asianews.it/news-en/Xi-Jinping-raises-the-Zhejiang-clique,-fights-the-Communist-Youth-League-37642.html.

[xxix] Orville Schell, “Life of the Party: How Secure Is the CCP?,” Foreign Affairs, July/August 2021, 73.