Is US manufacturing reviving in the Trump Era?

Donald Trump won the US presidency in no small part by appealing to displaced or underemployed industrial workers and all those in supplier industries closely tied to manufacturing. He promised a turnaround in this sector and the return of factories from abroad. While the first two years of his term did inject some new vigor in the entire industrial sector, the last year has been less favorable. Some changes in policy direction are needed if stronger growth is to return.

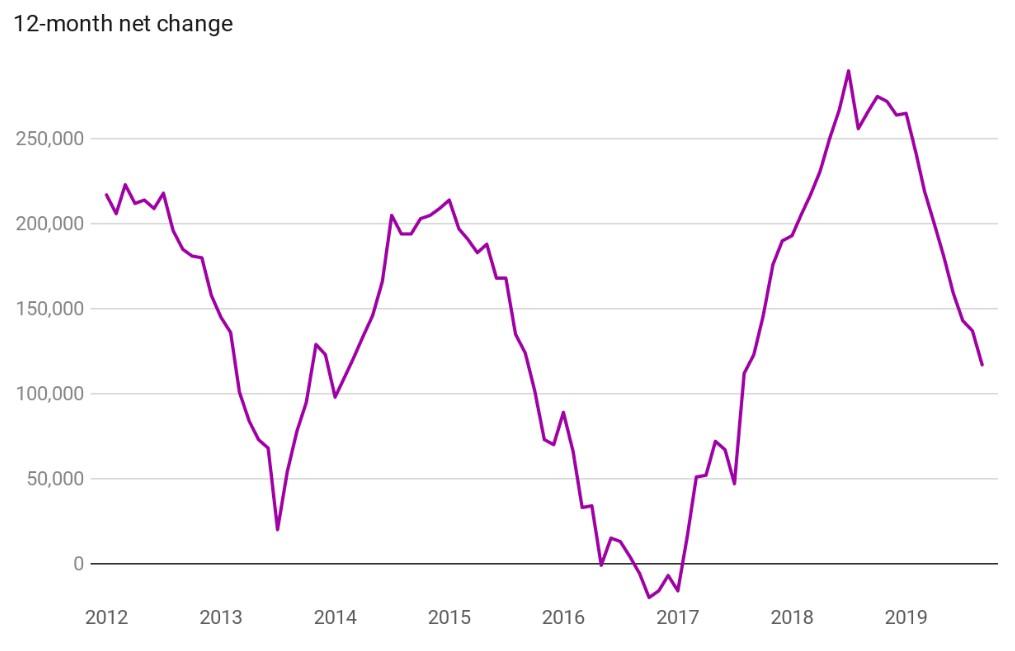

While the Obama administration witnessed a loss of almost 200,000 net manufacturing jobs and thousands of factories leaving for lower wage countries, the Trump years have produced, thus far, almost 550,000 manufacturing jobs.

Related areas such as oil and gas production, transportation and business services also benefited from a combination of more favorable tax and regulatory policy, and the general revival of what Keynes called “animal spirits.” Newfound confidence can be seen in the growth of employment in small businesses, often tied in one way or another to the industrial sector. Since 2018, wage growth in the lowest tier of workers has outpaced that of the middle and upper tiers, advancing by around 3.5% on an annual basis. Forty percent of new jobs in manufacturing are being claimed by college educated workers, with commensurate increases in wages to match skills. Trumpian rhetoric alone, albeit not subtle, clearly conveys the message that policy will be determined more by its impact on creating jobs and rebuilding manufacturing than by the softer kinds of environmental and social goals characteristic of his predecessor.

Despite the aggressive new trade policy, including tearing up existing agreements such as NAFTA and the TPP, and the imposition of broad new tariffs on metals, kitchen goods, solar panels and much of Chinese exports, US merchandise exports grew by 15% after Trump took office. Capital expenditures and intellectual property investment grew strongly in 2017 and 2018 as a new tax regime more favorable to domestic investment took effect. Oil and natural gas production boomed, spurring much of the capital expenditure growth, and the US has become largely self-sufficient in fossil fuels. It has also become a large exporter of raw and refined petroleum products, including the downstream chemicals dependent on lower-priced raw materials. By 2018, exports of oil and refined products totaled over $150 billion, making this the largest single US export category.

The cumulative effect of a global economic slowdown, the various trade tensions arising as Trump challenged perceived unfair trade practices in China, Latin America and Europe, a glut of oil and gas production, and the growing uncertainty occasioned by trade policy, Brexit, and political fragmentation in Europe and South America have slowed the momentum in the US industrial sector in 2019.

Lower oil and gas prices, leading to a decline of over half in active drilling rigs this year, and political uncertainty have undercut capital investment, whose growth was negative in the second and third quarters of 2019. Manufacturing sentiment indicators turned mildly negative starting in August, and production indicators have been largely flat in the second half of 2019. The production slowdown at Boeing and the lengthy strike at General Motors also contributed to the slowdown. Political tensions between the two major parties in the US Congress have all but paralyzed the work of the legislative branch. Any hope for a stimulative infrastructure investment program has dissolved in the wake of congressional gridlock. Housing construction, another possible source of strength, has never recovered from the psychological impact of the Great Recession. Younger workers have expressed decidedly less interest in limited geographic mobility and resigned to temporary or “gig” career paths, dampening demand for new single-family housing.

The slow but steady growth in US manufacturing has consequently stalled in the second half of 2019. Notably for the prospects of a Trump reelection, manufacturing job growth has turned negative in the politically sensitive states of Pennsylvania, Wisconsin and Michigan.

It is difficult to escape the conclusion that the resolution—or escalation—of ongoing trade disputes will have a considerable impact on any hope for continued strengthening of the US industrial sector in 2020 and beyond. While it is hard to detect any major impact thus far from the Trump trade disputes, with the exception of the heightened uncertainty which results in a subdued appetite for capital investment, failure to reach some agreement between the US and China, and the subsequent raising of tariffs and decoupling of supply chains, would cause major problems for US industry. Trade tensions with Europe could also cause disruption. Even if Trump chooses not to impose the threatened auto tariffs, differences over Airbus subsidies, digital taxes, WTO reform, aggressive antitrust actions on US technology companies, and nascent EU industrial policy, could spiral out of control and lead to recession in the world’s two largest economies.

Given the high stakes involved in these disputes, the agreements announced on December 12 are positive for manufacturing, presuming they are finalized early in 2020. The new USMCA should aid especially the auto and metals industries in the US. The first stage deal with China would eliminate forced technology transfer and give better overall intellectual property protection while increasing exports of industrial goods. Such changes should help capital goods producers. Hopefully too the common incentives for the US and the EU to work together to avoid disaster at the WTO and to meet the systemic China challenge will be sufficient to instigate a more cooperative phase of resolving long-standing differences.