World trade, inflation and global growth

The recovery of the world economy in 2021 has been more sustained than previously expected thanks primarily to the positive outcome of the current vaccination campaigns in many large, advanced countries. This has made it possible to accelerate the reopening of production activities and significantly reduce restrictive measures on the movement of individuals.

The official figures for the first three quarters of the year indicate that global GDP in 2021 is likely to grow between 5.5% and 6% in 2021, maybe even exceeding it. In this largely positive context, the recent problems related to supply bottlenecks, global trade and the ensuing price rises represent risks that should not be underestimated, especially for the manufacturing sector.

Read also: The inflation scare and healthy economic growth

Global trade has recently slowed after a strong start in 2021 with a peak in March and a very healthy second quarter. Exports from the most advanced and emerging economies are back to pre-crisis levels – with the UK being a notable exception. Trade growth rates are now becoming more moderated, gradually returning to more business-as-usual levels. Still, many disruptions are still present in some key global value chains and are expected to only ease off in 2022, with lower global demand growth rates. Industrial supply and global logistics are likely to keep struggling to respond to demand in the coming months, even as the global recovery slows. Transport costs are still at very high levels as a consequence of excessive port congestion in many parts of the world and to crude oil and natural gas price hikes, now at six- to seven-year highs – contributing to negatively affect global trade flows.

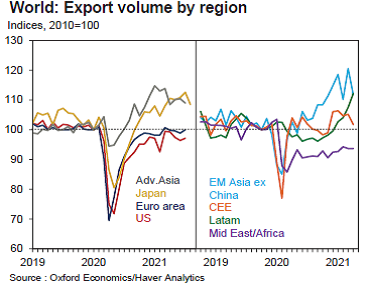

The trade slowdown is visible in both advanced and emerging economies, but with considerable variation across regions and economies. Weakness is especially notable in Asia, with advanced Asian trade down 4% since March and EM Asia (ex-China) down almost 3%. Elsewhere, the US and euro area show a fairly flat trend, while trade looks depressed in the Middle East and Africa but is rising in Latin America (Figure 1).

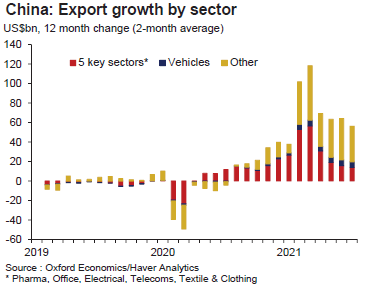

On top of the obvious “base effect” (the comparison with the pandemic-depressed trade in the first half of 2020), one of the important factors behind the stalling growth in world trade is the slowdown in China’s exports, after the boom in 2020 and early 2021.

This surge in exports was due to elevated demand for key Chinese goods created by the coronavirus pandemic, including pharma products, some textiles and electronic equipment. This abnormally high demand is now easing off and with it, Chinese export growth (Figure 2), although export levels remain much higher than before the pandemic.

While it was expected that the slowdown in China’s exports was going to happen, other negative factors are also behind the slowdown in world trade.

Port closures and temporary factors. Congested ports around the world have created supply bottlenecks, and the ports of Shanghai and Ningbo in China were closed for some periods in recent months due to COVID-19 outbreaks and Typhoon Chanthu. August data for port throughput showed declines in China, Singapore and in US ports along the West Coast – pointing to weakness in trans-Pacific trade. Trends in Europe and India were more favorable.

Supply chain disruptions. A variety of supply-chain disruptions has also negatively impacted trade. World shipping rates have soared and the rise shows few signs of abating. Challenges are also evident with road transport. The German truck index has dropped around 5% since March.

Sector-specific problems. There are acute and ongoing issues in several specific industries, such as automobiles and semiconductors. In Germany, exports of cars have slumped by 10% since March due to chip shortages, with electrical goods sales also levelling off. Meanwhile, much more upbeat trends are visible in intermediates, consumer goods and chemicals. A broadly similar picture is visible in Japan where overseas sales of motor vehicles have dropped by around 14% since March and IT product sales are also starting to drop after a strong run.

Interestingly, intermediate exports are flattening off in Japan, possibly reflecting a broader regional trade slowdown. The challenges in the auto and electronics sectors matter because these are large sectors with complex supply chains (causing big knock-on effects on both upstream and downstream industries). Motor vehicle exports represent around 4% of world exports, while ICT goods represent over 10% of world trade. With supply issues for semiconductors likely to persist for some time, these sectors risk continuing to weigh on trade into next year.

Despite this combination of negative influences, it is still very likely that global trade of goods for 2021 as a whole will rise by more than 10%, after a 6% fall in 2020. But with trade potentially flat or declining in the second half of 2021, goods trade growth in 2022 could be in the low single figures.

To partly mitigate the negative impact of the factors above, trade in total services, which was devastated by the pandemic, has started to improve, although the recovery so far in total services exports is uneven – the US and Singapore, for example, are doing somewhat better than the UK and the Netherlands. With restrictions on travel likely to remain in place for some time, it seems unlikely that global services trade will be able to recover fast enough to fully offset flagging growth in goods trade, in the near term at least. Indeed, ongoing travel restrictions (and increased travel costs) mean that for some economies that are heavily dependent on travel and transport receipts, weak exports in these two sectors are going to be a medium-term obstacle on activity.

Read also: Global nfrastructure development: China, Biden and the new pivot of 21st Century geopolitics

Most of the above factors – other than services trade – can significantly dent the expected economic growth in 2022, making it difficult for central banks to manage monetary policy and the tapering from the expansionary policies adopted during the pandemic. To make the task of central banks even more complex, some of the factors that have contributed to the slowdown of world trade are also impacting the prices of goods and energy products, raising inflation in advanced economies as well as globally.

The risk of a resurgence in inflation is inflaming the debate on how transitory the phenomenon might be and on whether central banks should start reversing the highly expansionary monetary policy implemented in response to the pandemic. In this regard, a number of considerations in favor of the temporary nature of the inflation hike should be kept in consideration:

- The current high level of inflation is mostly due to a flare-up in the prices of several energy products and various commodities – but in order for these prices to continue to push up inflation, further flare-ups of the same magnitude would have to be seen on a continuous basis, i.e. energy prices would have to be duplicating every few months. This appears unlikely both for geopolitical reasons and because other energy sources would become price competitive, among which coal, renewables, shale oil and shale gas.

- In advanced economies, total energy products have a modest weight in the inflation basket (typically below 10%) and inflation is rather determined by the trend in prices of the tertiary sectors, which account for well over 60% of the inflation basket. The pass-through effect from energy intensive product prices to manufacturing goods and services is nowadays much less significant than it was historically. Furthermore, it depends on a number of factors that will reasonably mitigate the impact of energy price rises – such as the reduction of company margins, policy intervention, lower demand, etc. Indeed, while total inflation has recently reached worrying levels in some major areas (namely the USA, the UK and to a lesser extent the EU), core inflation is still hovering around 2%.

- In the medium term, the factors that held back economic growth and inflation prior to the pandemic will once again be prevalent, such as aging populations, excessive savings, low productivity, high debt and the consequent need for deleveraging.

In a nutshell: the extent and the duration of the supply-side bottlenecks, global trade and inflation dynamics are major risk factors. However, they all appear temporary in nature. At the same time, the price dynamic in recent months is a wake-up call that should not be underestimated and should be carefully monitored.

Indeed, trade, growth and inflation forecasts remain highly dependent on the evolution of the pandemic. A new imposition of restrictions or a deterioration in sentiment caused by a worsening health situation could slow economic activity again.