Managing debt in the developing world

A version of this article is published in Aspenia International 2-2023

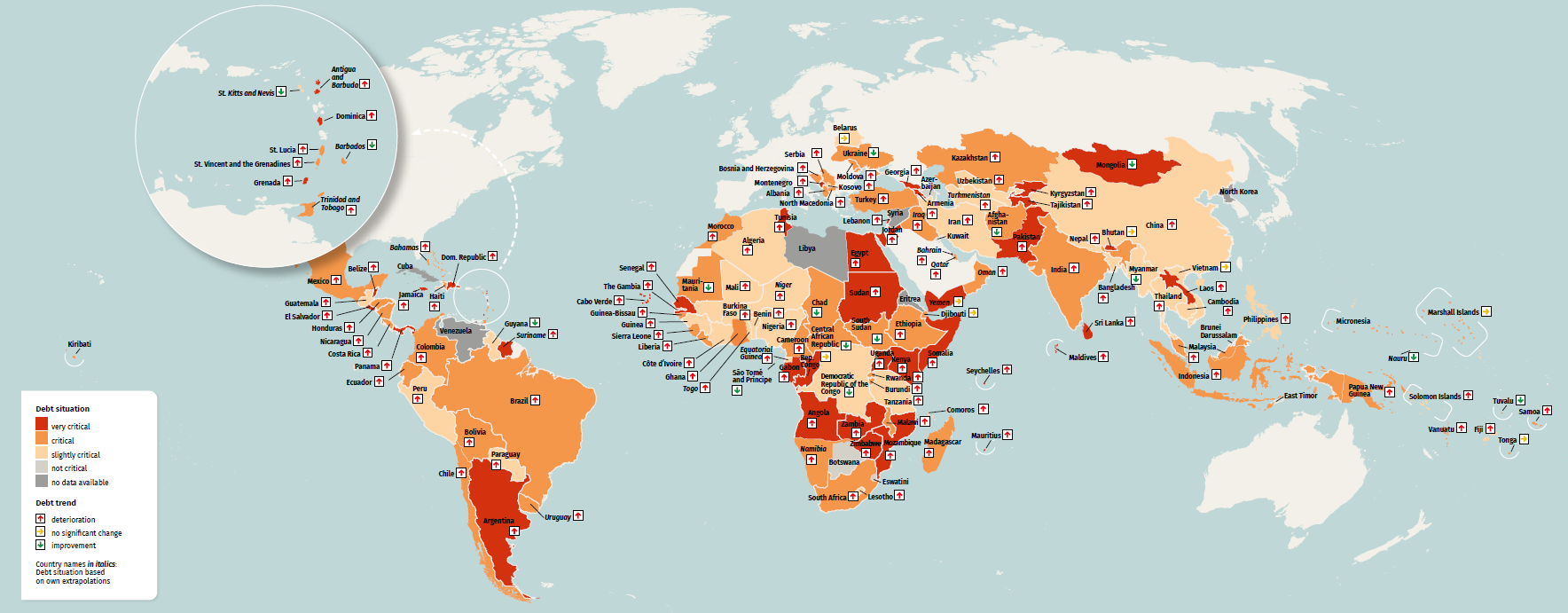

The impact of Covid-19 and then the war in Ukraine have dealt grievous blows to developing countries, especially to the poorest and most vulnerable ones. Events have conspired to rapidly increase the burden of their level of debt. The rise in interest rates, following the restrictive monetary policies adopted by all the major countries, then made these debts even harder to manage. Thus, a growing number of low-income countries (LICs, also known as LDCs, or least-developed countries) find themselves in situations of excessive debt (debt distress), and some of them have experienced a state of real insolvency (debt default).

THE DIFFICULT RESTRUCTURING OF DEBT. The crisis is serious, but it has not yet become systemic, as did happen in the 1990s. Some of the chief causes of the current crisis include the radical changes that have taken place in the structure and organization of financial markets globally over the last 15 years; these have fragmented the bloc of creditor countries and made them a heterogeneous grouping. Of these, China has become the biggest creditor of countries with average and low incomes. Beijing’s rise has been rapid, and has brought geopolitics to the fore of processes involving the restructuring of LDC debt. China has been handed the biggest share of the blame for the defaults and for the situation of deadlock in which restructuring operations are now stuck. This is only partly true. In fact, the fragmentation and political tensions that mark the current state of relations between lenders and debtors are to blame for many of the failed debt-alleviation initiatives of late.

A glimmer of hope was seen in June 2023 when initial, significant steps were taken to restructure Zambia’s debt on the part of official creditors, including China. It is a promising initiative, which should be extended to other countries in difficulty. However, many questions remain regarding the real willingness of numerous creditors to continue further along this path. Finally, it should not be forgotten that, while it is true that the excessive debt of LICs must be addressed through new financing, what are needed above all are measures and policies that can get their development processes moving again.

HOW SERIOUS IS THE DEBT CRISIS? According to International Monetary Fund forecasts, more than half of low-income countries are in danger of entering a situation of debt distress; indeed, many are already in such a situation, with the specter of the suspension of reimbursements looming over them. According to the World Bank, around 60% of the world’s least-developed countries are currently at a high risk, whereas this percentage was 40% prior to the pandemic.

Debt servicing – a measure of a state’s ability to meet the demands of foreign lenders – has become more burdensome in recent years for almost all highly-indebted developing countries. For countries that have the lowest income levels, especially, the cost of servicing their debt has risen greatly, from 4.1% in 2012 to 17.7% in 2022 in GDP terms. In parallel, the amount of public revenue set aside for paying foreign debt costs has risen considerably in recent years. It is estimated, for example, that for more than half the countries in sub-Saharan Africa, debt servicing currently absorbs more than one quarter of total public revenue. This leads to severe reductions and cuts in public spending earmarked for health, education and infrastructure, with serious economic consequences, and huge humanitarian costs.

Accordingly, it is no surprise that the excessive debt burden has become one of the biggest obstacles to the development process in many emerging countries. It is also making it very difficult to achieve, by the end of this decade, the 17 Sustainable Development Goals (SDGs) previously set by the United Nations. Indeed, some believe that it is now impossible to achieve this target.

But the current debt crisis, while high-risk and very worrying, has not yet reached the alarming levels of the past. In the mid-1990s, for example, a systemic crisis exploded with globally contagious mechanisms. That was when, at the multilateral level, the IMF and the World Bank brought in the initiative for highly-indebted poor countries (the HIPC Initiative) which led to the large-scale cancelation of debt for many LDCs (more than 30 of them), especially in Africa. This thereby released funds for their subsequent rebirth, allowing these countries to accumulate new debt, including from today’s creditors (such as the private sector and, above all, China).

However, it must immediately be added that the current crisis, while still confined to individual countries – including Zambia, Ghana and Sri Lanka, already in a default situation, and Pakistan and Egypt, which are close to defaulting – risks deteriorating rapidly in the absence of intervention. If timely solutions suited to tackling the most serious cases are not devised quickly, this crisis too could be transformed into a systemic and global event. Consequences will be dramatic: rampant inflation, social revolts, political instability, and blocked development in multiple countries in the poorest parts of the world. Some early, dire signs of such a scenario are already appearing. However, there is still time to intervene.

HOW THE GLOBAL FINANCIAL SCENE HAS CHANGED. The global financial context has changed profoundly since the major global crisis of 2008-2009, as have relations between creditor and debtor countries. In the 1990s, for example, the debt of developing economies was mostly owed to official creditors – namely, the governments of the most advanced countries – almost all members of the Paris Club (22 countries, including the United States, France and the United Kingdom). And this informal group of official creditors found and coordinated suitable solutions, drawing up debt restructuring where necessary, in the case of excessively indebted countries. This is what happened – as stated above – in the 1990s, with the HIPC Initiative, to tackle a debt crisis that had taken on global proportions.

Read also: The US-China economic link: high level diplomacy and structural problems

But an initiative of the same sort would be impossible to put forward today. The role of the Paris Club countries has been greatly reduced in the last few years: they hold barely 11% of the total debt of low-income countries, compared to 39% in the past. And players outside of this club have doubled their share. Of these, China has become the largest creditor with regard to around half the lowest-income nations, with loans issued in the last two decades totaling some 850 billion dollars. Thus it comes as no surprise that Beijing has today acquired a crucial say in all negotiations over the management of emerging countries’ debts.

Another important change in the last few years is that the debts of LICs toward foreign private sector creditors have tripled. In recent years, many developing countries have found it more attractive to get hold of financing directly on their own markets, by means of bond issues in local currency. In the past, bonds tended to be issued in dollar denominations, which cost less than bonds in local currency because they bore fewer premiums covering against the risk of inflation.

This growing level of dollar debt, however, later forced many countries in the developing world to address shocks and crises that were completely outside of their control, as happened in the 1980s and 1990s in Latin America, Asia, and many other regions. Since then, international institutions such as the IMF and the World Bank have pushed many emerging economies to create domestic capital markets, and to turn them into alternative sources of financing in local currency. The domestic debt of developing countries thus tripled, rising from 8% to 24% in GDP terms. And this ended up in the portfolios not only of commercial banks, but also of a vast assortment of private sector intermediaries such as hedge funds, investment houses, and various other financial bodies. During the prolonged phase of easy liquidity, marked by low or even negative interest rates, governments and/or companies in less developed countries had no difficulty in servicing this debt. Later on, the era of restrictive monetary policies and high interest rates kicked in, creating serious and growing financing difficulties for many countries.

This brings us to today, where we are seeing many countries with debt that has become excessive, and that would require refinancing and restructuring organized at the multilateral level. But the IMF, the Paris Club countries and the commercial banks of the London Club can no longer put together solutions. In the changed global financial context, debtor countries now have to take action on multiple fronts: alongside the IMF and the Paris Club, they need to involve the Chinese government, state banks and state-controlled commercial banks, fund managers and the various central banks of Western countries. The positions and interests of all these lenders are highly heterogeneous, while the rules of the game currently in force are those of the blame game: in other words, many players operate like free riders, trying to offload the costs of the inevitable adjustments. With the predictable result of creating obstacles and making it difficult to reach any accord about large-scale restructuring, ultimately leading to the paralysis of recent years.

THE URGENT NEED TO RESOLVE THE DEADLOCK. Offering solutions to the current debt crisis must remain a top priority on the international agenda of the more advanced countries and of international multilateral organizations. The vulnerability of LDCs must not be allowed to spread like wildfire and to become systemic in nature. And the fragmentation and tensions in the current global financial context, aggravated by geopolitical factors, must not hinder the search for such solutions.

It is only partly true that the blame for the current deadlock is to be laid at the door of the Chinese government. True, once Beijing achieved the position of being the largest creditor for the developing area, it preferred to go it alone, with loans that have been distinctly opaque. And in tackling the difficulties of the most debt-ridden countries, China chose to refinance their debts, rather than restructure operations, thereby seeking to ensure that its banks were repaid in full. This line of action has further complicated the search for solutions to the debt crisis of many countries. But this was not such an unusual approach. Indeed, it was in line with the classic cliché of a country that becomes a large creditor, and that decides to act tough because it is aware of its own strength – no more and no less than other big creditors have done in the past, starting with US commercial banks in the 1980s.

In the end, China, too, is realizing that it needs to compromise with other major creditors, and that it is in its own interests to do so. Indeed, it has recently signaled its intentions to this end. All efforts will need to be channeled toward the common goal, which remains reducing the unsustainable burden that debt has come to represent for many poor and developing countries.

A FEW PROPOSALS FOR COORDINATED ACTION. It is advisable at this point to pursue multiple paths when taking action in the new global financial context. These need to be somehow coordinated and streamlined, because it remains vitally important to surmount the problems of “collective action” that continue to hinder the achievement of accords between lenders and debtors.

There is already a certain level of consensus over the steps that need to be taken, at least on a number of fundamentals. For example, as regards the countries in the greatest difficulty and with unsustainable debt, there is general agreement that debt should be restructured without delay. To this end, official bilateral creditors ought to agree on a common approach that is accepted both by the members of the Paris Club and by those that are outside it, first and foremost China itself.

Read also: Financing sustainable development

Such restructuring operations would need to be developed within the context of the common negotiation framework proposed by the G20. So far those subscribing to the Common Framework have been few and far between, but it must nevertheless be reinforced. At the beginning of 2023, the World Bank and the IMF offered a timetable to improve the program, with four recommendations: a clear calendar, the suspension of debt payments during the negotiations, the institution of clear procedures and rules, and expanded requisites for admissibility. This is a positive development.

Also to this end, there seems to be agreement that private sector creditors be encouraged to take part, together with official creditors, in the debt restructuring processes by means of suitable incentives and mechanisms, given their current significance. Indeed, often it is the dissatisfied private sector creditors that end up refusing to align themselves with the conditions offered by state creditors, thereby blocking a country’s debt restructuring process. Above all, they should not be treated as residual creditors, as happened again recently. True, this was how things were done in the past, but back then the importance of private creditors was only marginal.

Another suggestion to be adopted is that creditors should reinforce those contractual terms that help debtors to overcome unforeseen and exceptional difficulties. One example of this is the suspension of debt servicing obligations for countries that find themselves dealing with catastrophic natural and climate-related events, as was agreed at the height of the Covid-19 pandemic. This should now be made permanent. Additionally, the transparency of data and of debt management procedures ought to be significantly improved, ensuring that information is more reliable than it is today, and that it can be more easily compared from one nation to another.

As already mentioned, a positive signal in this direction came in June, when state creditors, including China, agreed – after a more than three-year deadlock – on an initial restructuring (to the tune of 6.3 billion dollars) of Zambia’s foreign debt. This amounted to around 13 billion after the country defaulted in November 2020, finally taking some initial positive steps in the right direction.

AVOIDING A SYSTEMIC CRISIS. Many questions remain as to the real willingness of creditors – primarily China and many private sector operators – to significantly reduce debt burdens. This we shall have to wait and see. Also, it should be stressed that debt restructuring, while highly important, ought also to be accompanied – in order to be effective, and to restore sustainable levels of debt – by measures and policies that can ensure that the development processes of the poorest countries can get off the ground again.

In conclusion, it should be reiterated that it is still possible to avoid another systemic crisis over the debt of the poorest countries, as happened in the 1990s, on condition that action is taken immediately. New ways forward must be pursued. It is not a case of helping LDCs out of sheer generosity, nor is it a way for the advanced countries to simply clear their consciences. At the end of the day, nobody gains if a country’s debt becomes impossible to repay, and stays that way. Quite the opposite. To cite just one reason why we are all in this together: in order to be successful, policies to fight climate change will need collaboration from all countries, starting with the poorest and most vulnerable. The search for suitable solutions is thus in everyone’s interest.

*A version of this article is published in Aspenia International 2-2023