Green lighting from America: the green transition and Transatlantic ties

While Europeans fled to the sea and mountains to escape the long heatwave that characterized last summer, the US government passed the Inflation Reduction Act. Along with the Bipartisan Infrastructure Law and the Creating Helpful Incentives to Produce Semiconductors Act (CHIPS and Science Act), the Inflation Reduction Act is the third piece of legislation since the end of 2021 that aims to improve the economic competitiveness, innovation and industrial productivity of the United States. Although they have partially overlapped priorities, the three laws constitute a federal fund of approximately $3 trillion in stimulus spending.

While the most recent law explicitly refers to the reduction of inflation, it could be more of a slogan than an appropriate technical-administrative denomination. The anti-inflationary effects of the law are minimal, deferred, and would derive from the limits on the prices of drugs and from interventions that favor greater energy efficiency and a shift in the production of electricity towards renewable sources. Also on the growth front, the direct effects of the Inflation Reduction Act should be modest and concentrated in the second half of the decade.

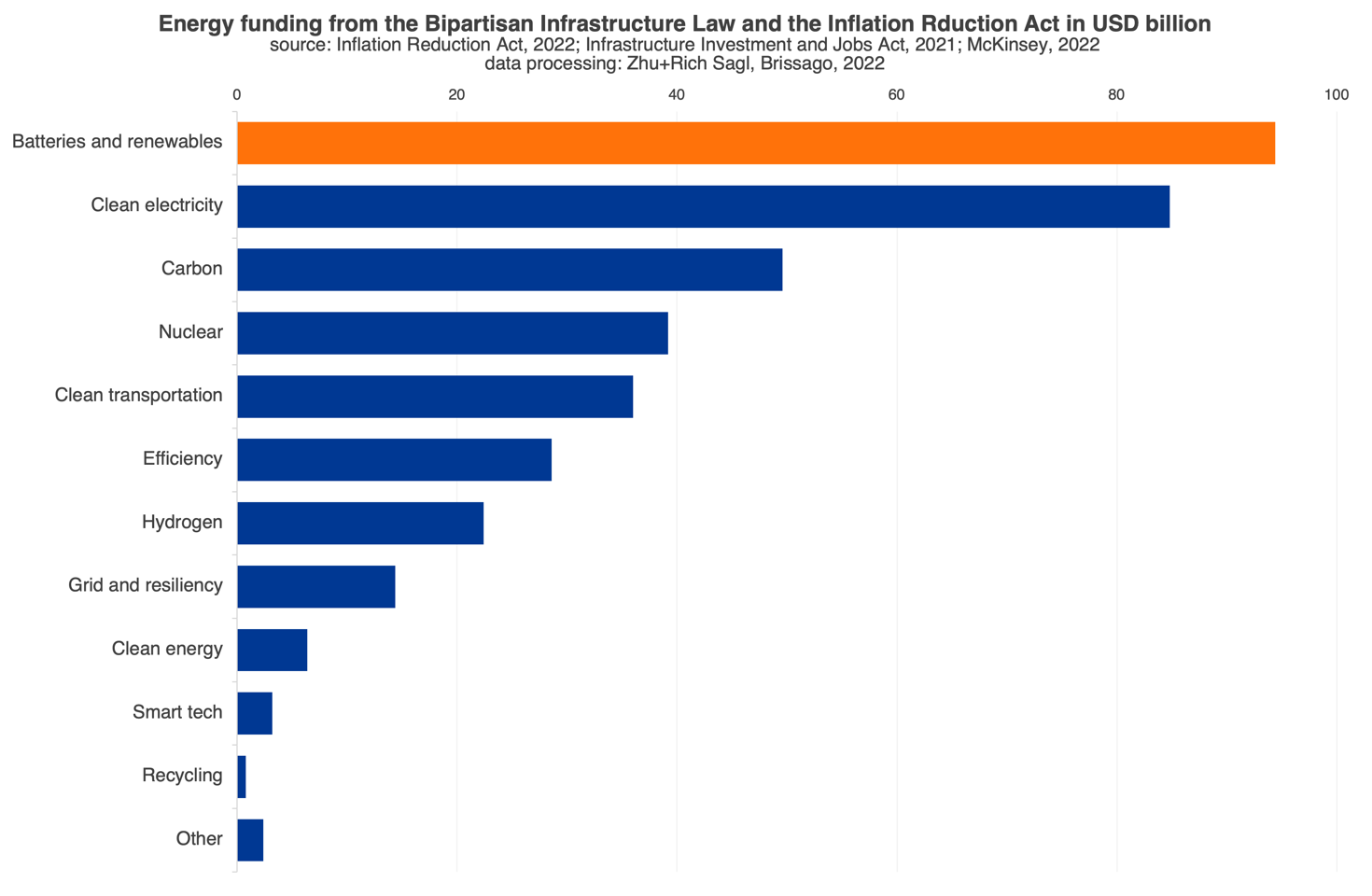

In addition to the usual macroeconomic criteria for evaluating a fiscal package such as growth, inflation, redistributive effects, deficit and debt, the novelty of the Inflation Reduction Act is that it adds another dimension to fiscal intervention, precisely the environmental impact. The law, as passed last August, will raise $738 billion, of which $394 billion will be earmarked for action to reduce greenhouse gas emissions, in so resulting the largest piece of legislation on climate change in US history. The funds will be disbursed through a combination of tax incentives, grants, and loan guarantees.

The main areas of allocation of funds intended for environmental protection are the production of energy from renewable sources and grid energy storage, nuclear energy, electric vehicles, advanced technologies to produce electricity, the energy efficiency and carbon capture and storage systems in existing power plants.

Of particular interest is the share of $43 billion earmarked for consumption incentives for the purchase of electric vehicles, energy-efficient appliances, solar panels, geothermal heating and domestic batteries. In the specific case of electric vehicles, consumers will be eligible for a tax credit of up to $7,500 on new vehicles and $4,000 on used vehicles.

A statement by the White House released the day before the Inflation Reduction Act was approved claims that the reduction of harmful pollution, that is greenhouse gas emissions, is by about 1 gigaton in 2030, or a billion metric tons – 10 times more climate impact than any other single piece of legislation ever enacted, that is more than the yearly carbon dioxide emissions from fossil fuels and industry in 2019 caused by France and Germany combined, precisely 0.301 gigaton the former and 0.657 gigaton the latter, according to the World Bank.

A few weeks later, Vice President Kamala Harris stated that the work done and the victories thus far won, that is the passage of the Act in the Congress, will deliver a 50% reduction in emissions by 2030 from the 2005 peak, and net-zero emissions by no later than 2050 – an outstanding achievement, even if not all agree on its actual size of emissions reduction of carbon dioxide.

Princeton University’s Zero Lab has released a preliminary report as part of the Rapid Energy Policy Evaluation and Analysis Toolkit (REPEAT) on the environmental and energy impacts of the Inflation Reduction Act. According to the report, greenhouse gas emissions in 2035 would be 42% lower than in 2005 under the Inflation Reduction Act, against a 26% reduction with unchanged policies, closing about two-thirds of the gap between projected emissions and those consistent with the objective of reducing emissions by 50% (zero-net target), allowing the United States to keep its commitment made in the Paris Agreement, that is a 50% reduction in emissions of greenhouse gases by 2030, helping to limit global warming by 1.5 degrees.

The law is aimed both at reducing carbon dioxide emissions and at stimulating American industry for the next ten years, but also at achieving independence and energy security and countering Chinese advances in sectors of primary importance, whose technical and scientific innovations ensure the green and digital transition, as well as global technological leadership.

According to Cowen Inc., a New York-based investment bank, the People’s Republic of China owns more than half of the world’s lithium, cobalt and graphite refining capacity. Furthermore, in electric battery components, it owns 75% of the cathode production capacity, 85% of the anode production capacity and 73% of the cell production capacity, a de facto monopoly.

Perhaps it is above all President Xi’s China that constitutes the real target of the Inflation Reduction Act: in the powerful effort to move the electric car supply chain to the United States and in the rest of North America, discouraging the procurement of materials and components from China, Washington’s economic and geopolitical rival that currently dominates the value chains of electric batteries and its constituent minerals. The Inflation reduction Act appears as an extension of the CHIPS Act, within a strategic plan aimed at containing Beijing’s intentions to impose its own world order.

The law has also rekindled American interest in the development and production of electric batteries to power vehicles. Federal funds will support the entire upstream chain of electric battery manufacturing, from mineral mines to refining plants, research, and development centers to battery manufacturing sites. The aim is to build a logistic-productive ecosystem capable of making the United States and its North American partners independent.

According to forecasts by Rho Motion, a London-based consultancy that conducts analysis of the electric vehicle and battery markets, electric car sales in the United States will double to almost 2.5 million vehicles by 2025. President Joe Biden wants half of US vehicle sales to be electric by 2030.

As with all treatments – to adopt a medical analogy – there can be side effects with the Inflation Reduction Act. Passing it comes with huge tax breaks and other subsidies for locating battery supply chains in the United States, as well as supporting electric vehicle deployment. Northvolt AB, the Swedish manufacturer of lithium-ion batteries for electric vehicles, European pride in the electric battery industry, supported for years by Volkswagen, BMW and the European Investment Bank, is now looking to the United States to expand its production capacity. According to the Northvolt CEO Peter Carlsson, the provisions of the Inflation Reduction Act would allow the US government to subsidize a factory in the United States up to 800 million dollars, against the 155 million euros offered by the German government.

Furthermore, incentives to purchase electric cars will only be recognized by tax authorities if a percentage of the critical minerals contained in the battery – such as nickel, cobalt and graphite – have been mined, refined or recycled in North America, or in a country with free trade agreements with the United States, that is Canada and Mexico, or even that the electric battery is manufactured or assembled in North America.

There is no country in the European Union that offers tax credits of €7,500 for the purchase of an electric car, a sum completely out of reach even for the Germans and French. Added to these attractive subsidies are the high costs of gas, which in Europe, even after the recent decline, remains five times more expensive than in North America. Spain’s Iberdrola, one of the world’s largest energy companies, is also increasing its share of investments in the United States following the approval of the Inflation Reduction Act, having received $100 billion in subsidies to produce hydrogen from renewables, against the €5 billion offered by the European Union.

Read also: Why the US needs to play a larger role as swing producer of oil and gas in the current crisis

Of the three recent laws wanted by the Biden administration to revive US industry, the Inflation Reduction Act is certainly the law that most upsets the political-economic institutional set-up of the European Union. The EU has accused Washington of violating the rules of the World Trade Organization, since the Inflation Reduction Act produces unfair competition, closure of markets and fragmentation of value chains between the two sides of the Atlantic. In particular, the European Commission denounces the distorting effects of the law and the risk of a race to the bottom of subsidies to businesses and consumers with a consequent flight of investments from the European market to the American market.

While the Inflation Reduction Act impacts manufacturers in sectors as diverse as advanced machinery to heavy industry, European policymakers are particularly concerned about the impact on the automotive sector, since, in a “buy American” logic, only electric cars made with components from North America or assembled there will be eligible for the tax rebate. The issue, then, may not be a European one, but simply a German one, since Europe’s largest non-German carmaker already has production units in North America. Then, recalling Chancellor Olaf Scholz’s recent business visit to Beijing, the old Italian motto “two weights, two measures” comes to mind.

Yet, the question of the subsidies provided for by the Inflation Reduction Act, which distort the free market and penalize European companies with discriminatory behavior towards European products, appears fallacious.

The $394 billion share of federal funds from the Inflation Reduction Act that goes to environmental protection, renewable energy and energy conservation is equivalent to about $50 billion a year over the eight years of 2023-30. According to the EU State aid Scoreboard 2021, in order to address the same needs envisaged by the Inflation Reduction Act, in 2020 EU subsidies were around €78 million.

Taking the year 2014 as a reference, as it was the year in which the guidelines for the state aid expenditure for environmental protection, including energy savings, came into force, subsidies increased by about 12.5%. Assuming for simplicity of calculation that the same growth rate is maintained for the two-year period 2021-22, it follows that the amount allocated by the European Union for environmental protection, renewable energies and energy saving corresponds to 100 billion as of 1 January 2023, precisely twice as much as the subsidies provided by Washington. The question of subsidies distorting the free market thus appears to be unfounded.

Brussels often forgets that outside its community market there are fierce and unscrupulous competitors who care little or nothing about its normative power, as well as its purism. The time has come for the European Union to simplify its state aid rules and adapt them to the new global context to counter both the undesired effects generated by the Inflation Reduction Act, and the unfair competition practices normally applied by other countries.

The experience of the pandemic has taught that it is essential to pool resources. European industrial policy, which is also starting to take shape albeit with ups and downs, needs financial support through the establishment of specific funds for technological innovation. The other way is the strengthening of existing funds such as REPowerEU, born as a response to the new geopolitical and energy market reality following the Russian invasion of Ukraine, which requires accelerating the transition towards clean energy and increasing Europe’s energy independence. It is not a mortal sin to support specific economic-industrial sectors to face the epochal challenges that are looming on the horizon.

Read also: Post-global America and the need for industrial policy

Still according to Cowen Inc., the United States would reach about 920 gigawatt hours of annual production capacity of electric batteries by 2031, the year in which the tax credits provided by the Inflation Reduction Act expire. Meanwhile, European producers would hit 1,186 gigawatt hours and the Chinese would remain the rulers of the world with 5,153 gigawatt hours – more than double the production capacity of the United States and the European Union combined.

A Euro-Atlantic dispute at the World Trade Organization would only ridicule the liberal-democratic model and show how ephemeral the alliance of the Western bloc is. All that remains is cooperation between North America and the European Union.

The first step would be for the United States to immediately grant European producers the same free trade conditions as on the US market for Canada and Mexico, in compliance with the requirements of the Inflation Reduction Act, to create secure, sustainable and resilient transatlantic value chains. A time-limited combination of protectionism and robust subsidies to businesses and households would allow Washington and Brussels to extricate themselves from their dependence on Beijing for electric batteries.

However, there is the risk of materializing the paradox of Achilles and the tortoise, though it is worth investing all resources to create alternative solutions to lithium-ion batteries, such as sodium-ion batteries, lithium-iron-phosphate batteries, biofuels or, finally, the king of the universe, hydrogen.