Why the US needs to play a larger role as swing producer of oil and gas in the current crisis

In response to Russian aggression in Ukraine, European nations have drastically reduced imports of crude oil, refined petroleum products, and natural gas from Russia. The 2021 levels of these energy imports were around 2.2 million barrels per day (mbd) of crude oil, 1.2 mbd of refined products, and 155 billion cubic meters (bcm) of natural gas on an annual basis. In addition to extreme difficulties in obtaining new sources of natural gas and to a lesser extent oil, the price increases throughout Europe since the onset of the war have been of historic proportions. In the days following the invasion, natural gas prices shot up by 62%, and UK energy prices were up by 150%. The full impact of the war, along with the related need to rein in the highest inflation numbers in over 40 years, has pushed Europe into a recession that threatens households and small businesses as well as European manufacturers’ ability to remain competitive. As a result, if the region cannot quickly assemble alternative supplies, the European commitment to assist in containing Russian aggression may weaken.

The United States has the capacity to serve as a short- to medium-term swing producer to fill much of the reduced supply of both oil and gas. But the US has not yet exhibited the political will to ramp up production of these commodities at the scale needed in the current crisis. This paper explores why the US should redouble efforts to compensate for the loss of crucial energy supplies that Europeans (and other allies who oppose Russian aggression) will suffer. If the US were to take advantage of its massive reserves of oil and gas, this policy would also be a more environmentally benign solution for the shortages than tapping reserves in the Middle East or Venezuela.

Swing Producers

Alternative sources of crude oil and refined products are more readily available than natural gas since the latter requires costly new infrastructure to be put in place. Building new pipelines, liquified natural gas (LNG) facilities, and transportation infrastructure and ramping up production all require permitting and financing that is difficult to obtain, at least in the developed world.

Saudi Arabia and other OPEC members were the traditional swing producers of crude oil and some refined products until the fracking revolution in the US. OPEC has decided to cut back production in the current situation, apparently at least in part to placate its Russian fellow traveler. Both the Saudis and the Emiratis, despite embarrassing entreaties from the Biden administration, have publicly sided with President Vladimir Putin on the question of supplies in the short run.

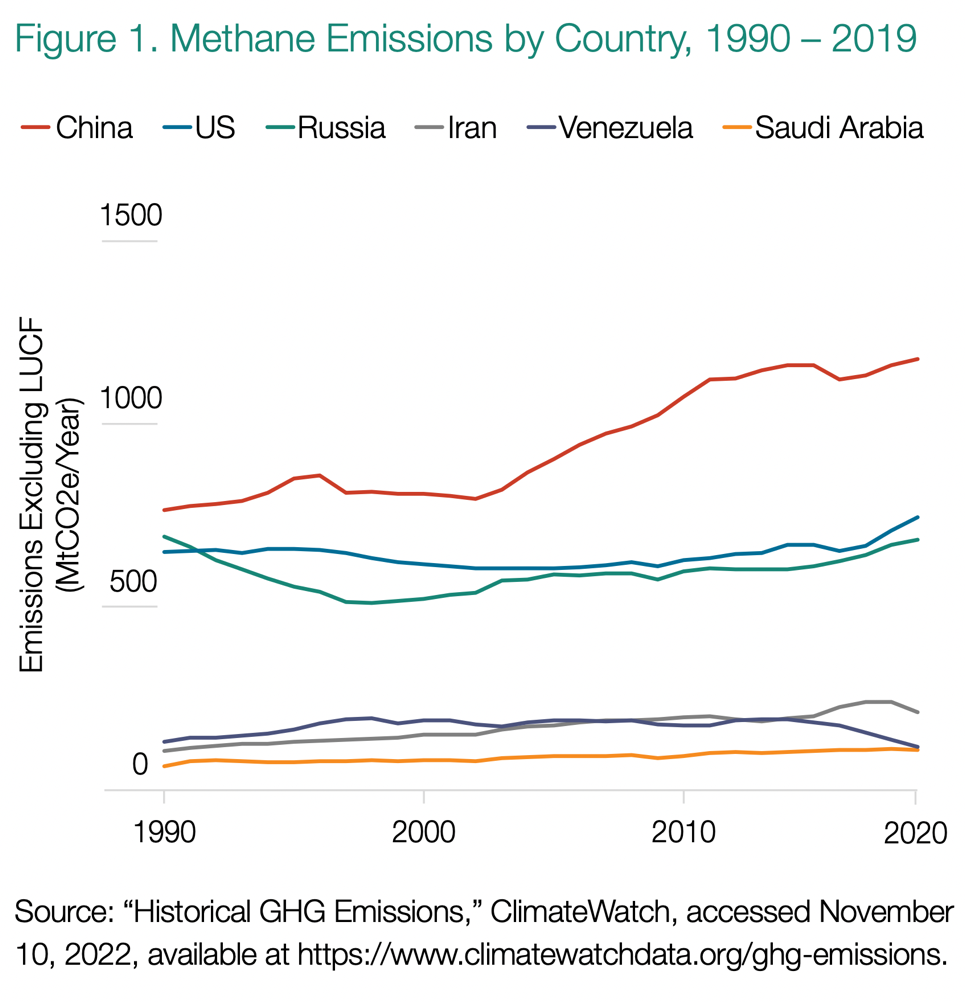

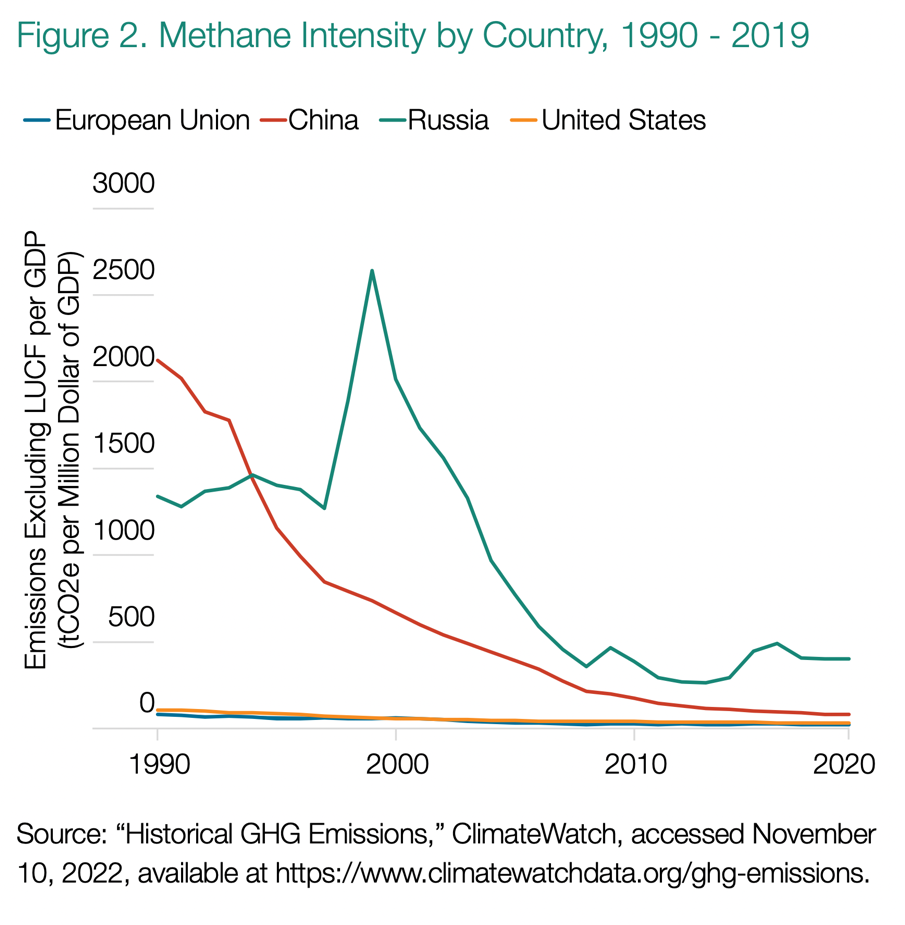

Both Venezuela and Iran, whose oil sectors are now under US sanctions, could conceivably put new supplies on the market. The ongoing negotiations to renew the 2015 Joint Comprehensive Plan of Action (JCPOA) – which the European Union and some voices in the Biden administration are promoting – and behind-the-scenes US-Venezuela talks are both intended in part to address existing shortages and high prices. In addition to how agreements with these two rogue powers would damage long-standing US policy, relying on these authoritarian states would set back any hope of progress in reducing atmospheric pollution. Figure 1 shows some of the world’s largest emitters of methane, which is 80 times more potent as a greenhouse gas than carbon dioxide (CO2). Methane is responsible for about 25% of today’s global warming, according to the Environmental Defense Fund. Russia, Iran, and Venezuela rank among the world leaders in this race to the bottom, even though the much larger US, European, and Chinese economies produce more of this gas. Figure 2 shows that, in terms of methane intensity, the US emits about 35 tons of CO2 equivalent in methane per million dollars of GDP. The equivalent number is 404 for Russia, 733 for Iran, 137 for Saudi Arabia, and 1,864 for Venezuela.

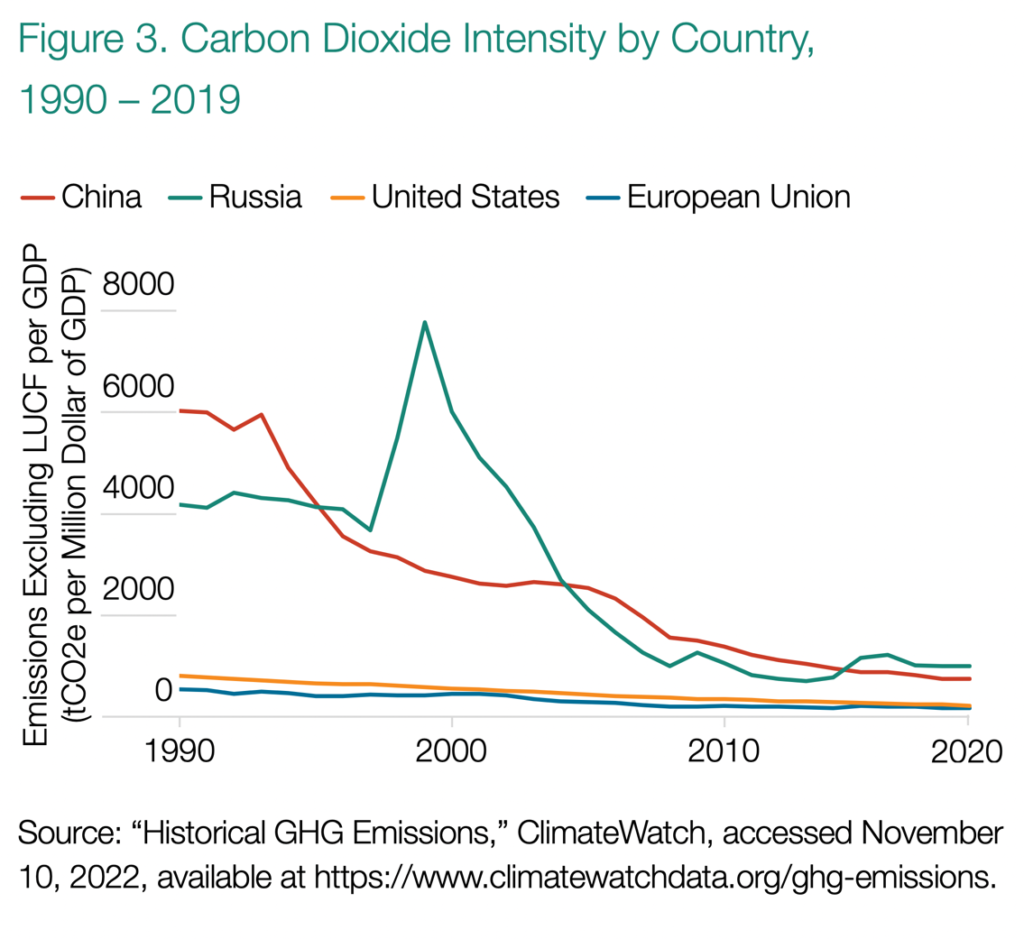

Figure 3 gives similar comparisons for CO2 intensity for leading countries. Again, Russia is much more profligate in its performance than the US or EU, releasing about 1,006 tons of CO2 per million dollars of GDP. Iran, Venezuela, and Saudi Arabia spew out 2,162, 1,756, and 651 tons of CO2 per million dollars of GDP, respectively.

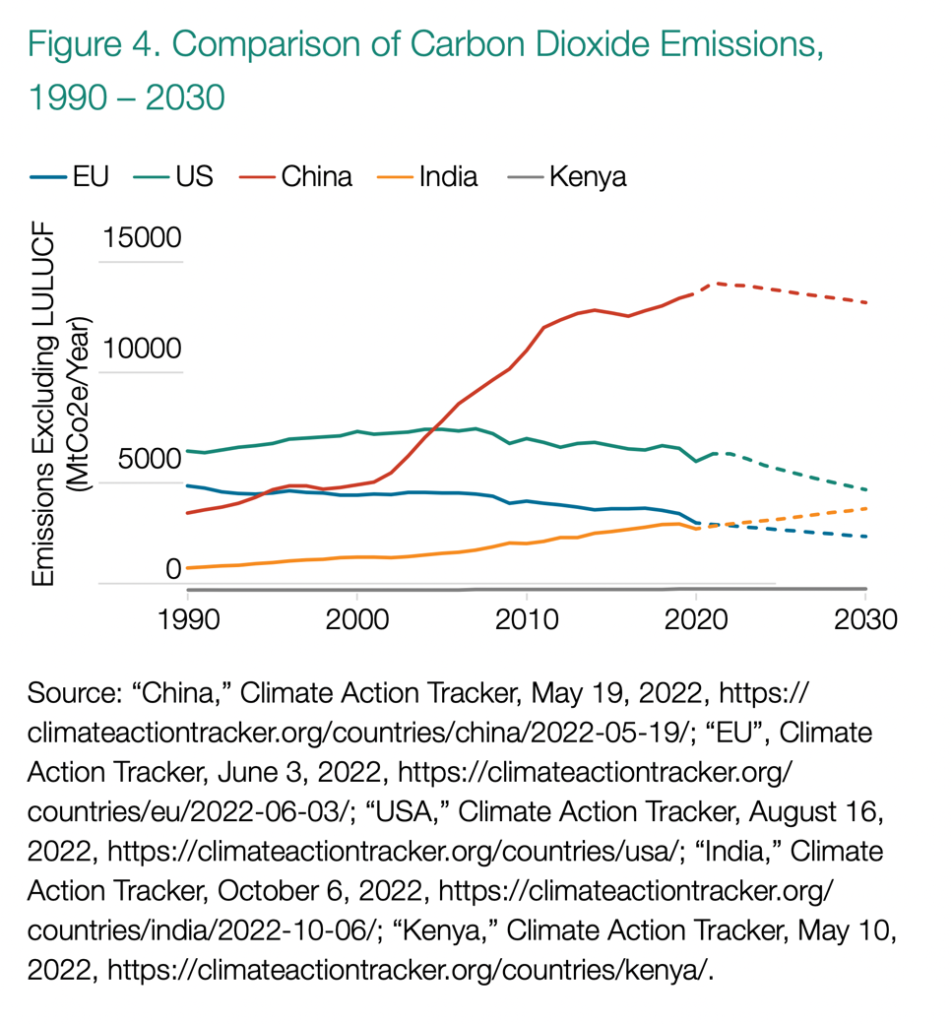

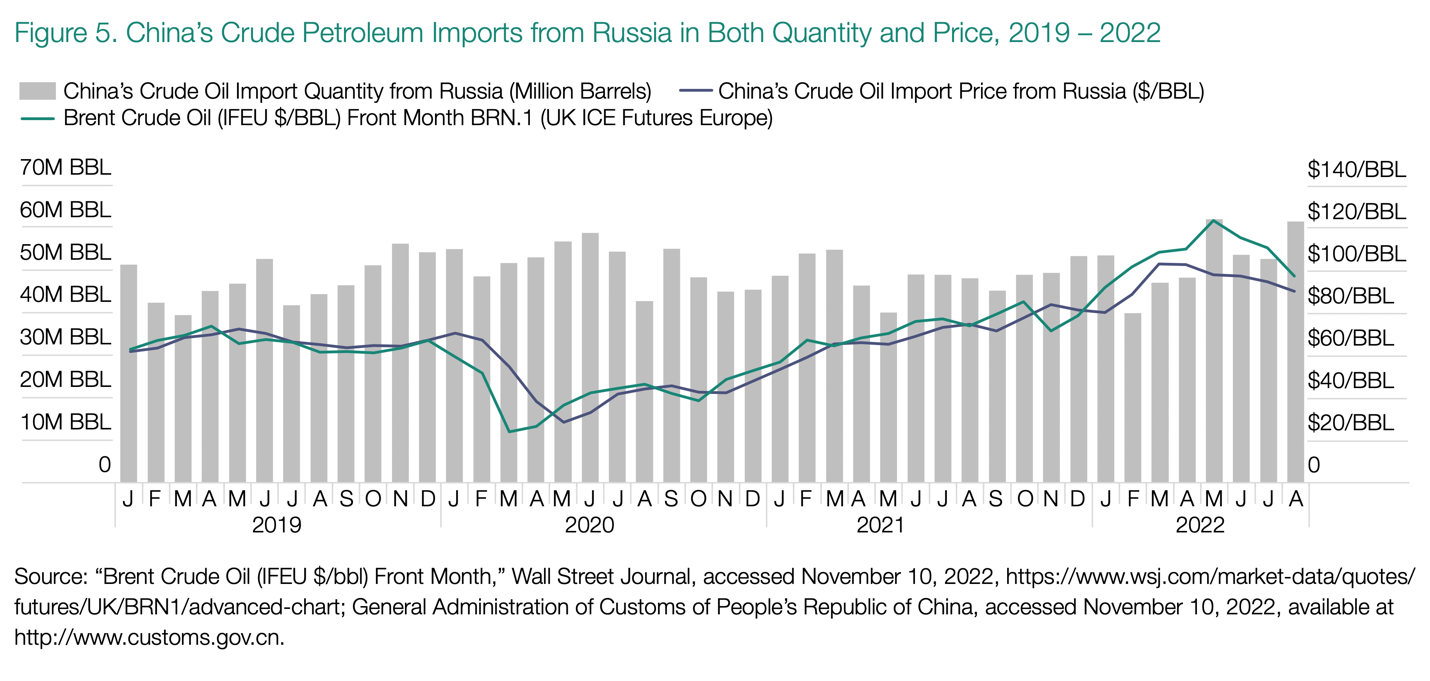

China now produces about 750 tons of CO2 per million dollars of GDP, compared to 225 for the US and 174 for the EU. China is by far the world’s largest producer of CO2, with higher levels of greenhouse gas emissions than all members of the Organization for Economic Cooperation and Development combined (see figure 4). This measurement does not include emissions that will occur after the completion of 94 thousand megawatts (MW) of new coal-fired electric generation capacity that is now under construction or the 196 thousand MW of new capacity already permitted. China is not a major oil and gas producer but has built up 30% excess capacity in oil refining, using crude oil imports in large and growing quantities from Russia, Venezuela, and Iran at favorable prices. Figure 5 shows recent data, derived from Chinese customs statistics, on the level and price of crude oil imports from Russia.

As the US and Europe have closed refineries in recent years, due in part to policies that made the financing of new fossil fuel projects uneconomic, China could possibly rush to compensate for current shortages of diesel fuel and aviation fuel. Whether for crude oil or refined products, relying on US- or European-based products is clearly preferable from an environmental point of view.

There are of course many other producers of crude oil: Norway, the United Kingdom, Brazil, and various countries in Africa. The reserves of these countries are large, and for the most part, their production has not been subject to political instability, except in certain African countries. Nonetheless, there are limits to their future expansion in the near term. Much of the production outside Africa is offshore, where the fields are difficult, expensive, and time-consuming to ramp up. Many Sub-Saharan countries rely on Chinese development assistance, which has already resulted in distressed debt in 60% or more of these countries. Volumes from these areas are unlikely to meet immediate needs.

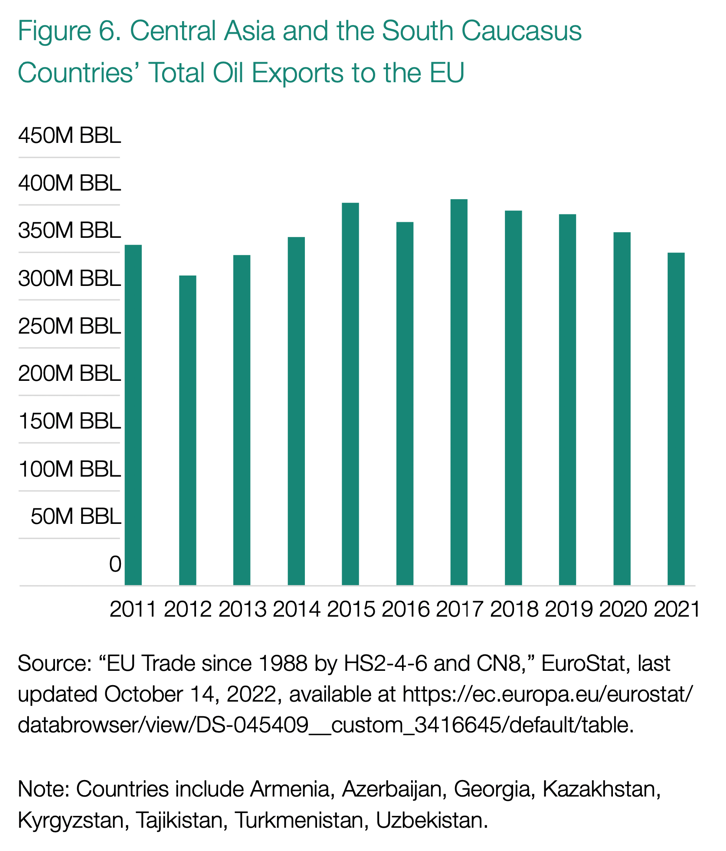

Finally, as figure 6 illustrates, Central Asia and the Caucasus have been exporting around 1 mbd to the EU. Much of this comes to Europe through a pipeline from Tengiz in Kazakhstan to the Black Sea and onto Europe and other destinations. But the pipeline passes through southern Russia and is potentially subject to sanctions from the EU and the US. Russian firms hold about 36.5% of the project while US majors own about 22%. Russia could cut off the flows through this pipeline at any time. About one-third of EU imports from the region is delivered from Azerbaijan via a pipeline from Baku through Georgia and Turkey to the Black Sea.

Huge amounts of oil reserves are available in this region but must be transported via Russia, Iran, or Russian-dominated Georgia to reach western destinations. Neither Russia nor Iran is keen on competition from non-aligned sources of petroleum, although Russia has allowed some exports of oil from Azerbaijan. Larger supplies of oil from Kazakhstan or Azerbaijan across the Caspian Sea could be delivered from pipelines through Turkey, but these too are complicated by the interests of the Iran-Russian entente.

Sources of Natural Gas for Europe

Since February 24, 2022, Europe has only had partial success in replacing the huge amounts of natural gas that either EU sanctions or Russian actions have cut off. Most of the replacements have been in the form of LNG. A relatively mild summer in East Asia and price arbitrage allowed cargoes contracted to this region to be resold to Europe, but this source of supply is beginning to decline as winter approaches. The EU also has negotiated new pipeline supplies from existing sources in North Africa and Norway. Prior to the Russian aggression, Norway regularly supplied Europe with about 100 bcm yearly. It has raised supplies by some 8% since late 2021, but this represents only a small proportion of the 155 bcm that Russia previously delivered.

There is huge potential to increase pipeline imports from Central Asia and the Caucasus. But again, the difficulty of bypassing Russian and Iranian territory and these countries’ opposition to competition makes any near-term additions unlikely. The existing “Southern Corridor” pipeline from Baku is delivering about 10 bcm of Azerbaijani gas through Turkey and into southern Italy. Plans to increase production and pipeline throughput are in place but remain difficult due to political instability in the Caucasus and hesitations of both buyers of the gas and financial providers to undertake long-term, risky investments at this time.

Figure 7 shows the largest LNG exporters as of 2021. The Gulf Cooperation Council members have ample supplies of gas, but only Qatar ships LNG in any material amount to Europe. Its exports via LNG to Europe were about 11 bcm in 2021. Qatar has plans to expand capacity significantly, but not until 2026 at the earliest. Its plans also depend on securing long-term contracts with buyers, and European buyers remain hesitant to agree to these.

Australia was the biggest LNG exporter in 2021 but sent only 0.037 bcm directly to Europe that year. Australia has no current plans to expand its capacity for exports, and internal politics have turned against new exports in any case.

Role of the United States

The US will have the largest volume of LNG export capacity in the world when new plants that are now being built and are expected to become operational in the next two years start production. Figure 8 charts the progress of LNG export capacity in the US, which in 2022 has already become the largest exporter of this comparatively clean fossil fuel resource, with projected exports of 114 bcm. New capacity coming online between 2023 and 2025 represents more than 50 bcm of capacity. The newest facility started exporting in August and represents 17 bcm of additional capacity. The US has already exceeded President Joe Biden’s pledge in March to increase LNG exports to Europe by 15 bcm this year, and it is estimated that the total increase will reach 45 bcm in this calendar year.

Total production of natural gas in the US has reached all-time records throughout 2022, facilitating increases in exports. The US is thus poised to steadily increase its exports to Europe and the rest of the world if public policy does not undermine further gains in production or infrastructure construction. It is worth noting that, as of 2020, only 11% of total natural gas production in the US originated on federally owned lands. Reliance on private property for gas production will limit the current administration’s ability to reduce production, although it does have other means to prevent the building of new infrastructure and discourage financing of new projects. In short, the US does have the means to be a swing producer and exporter of natural gas to address the current energy crisis.

US production of crude oil and refined petroleum products remains below peak levels set prior to the pandemic. The pro-production policies of the Trump administration, as well as the de facto tolerance of the Obama years, facilitated production and export capacity growth. In contrast, the Biden administration has adopted a whole-of-government effort to discourage and prevent crude oil exploration and development, as well as the construction of infrastructure required to bring supplies to refineries, chemical plants, and export facilities. Over 25% of crude production in the US originates on federally owned lands. New federal leases for exploration and development on federal lands are at the lowest levels since just after World War II, partially explaining the loss of production in recent years. Crude oil production in 2022 is averaging about 1 mbd below the peak reached in late 2019. Total exports of crude oil and petroleum products declined in 2021 but grew to early 2020 levels during the summer months as prices rose and the administration depleted the national petroleum reserve to levels not seen since the 1980s. However, exports of crude and refined products to leading destinations in Europe are trending upward.

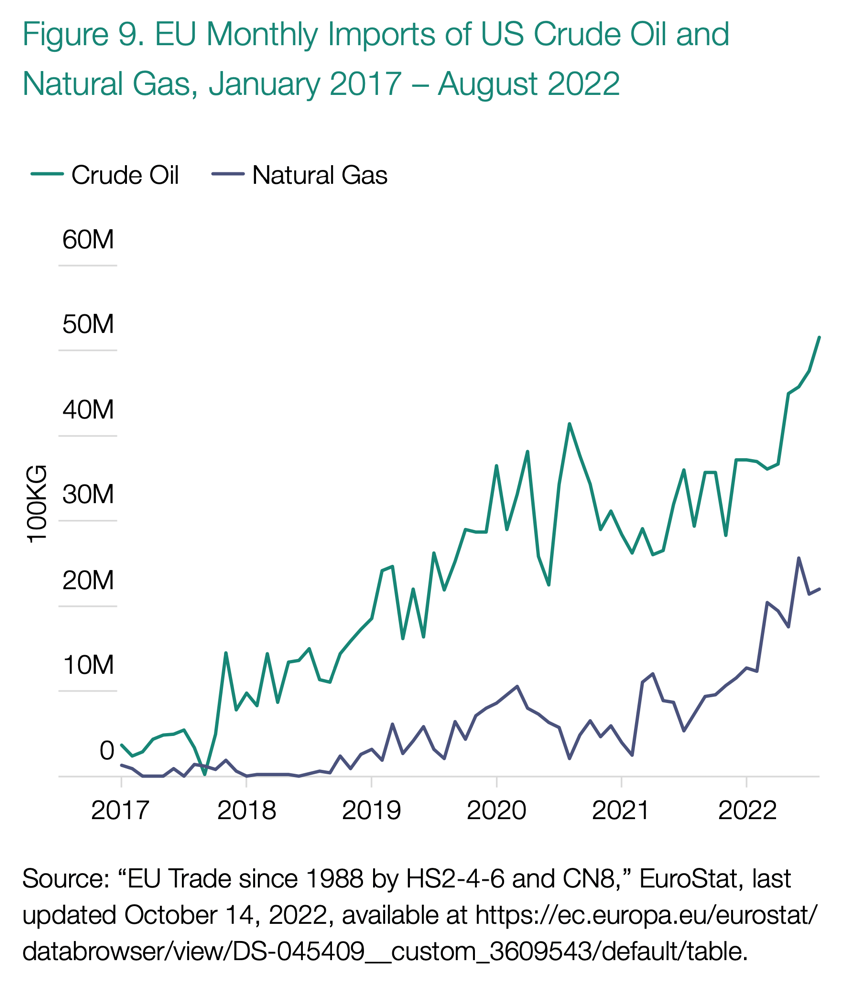

Figure 9 shows that EU imports of oil and gas from the US by volume have increased substantially in the last five years. The pace of increases has accelerated since February 24.

Where opportunities lie

Europe is in a desperate economic slump. High prices for energy are sapping the ability of homeowners to heat their homes, small businesses to remain solvent, and energy-intensive industries to keep operating. High prices are also affecting other countries around the world, including close allies in the Pacific Rim.

The US has the raw resources of oil and gas to be a bridge producer to meet much of the current shortage. The Biden administration ought to make a more substantial contribution to alleviating these problems. Instead, it asserts that the US must concentrate its ambitions and funding on developing renewable energy resources, even though these new sources will require decades to replace oil and gas power in the modern economy. Moreover, the Biden administration has ordered US foreign assistance agencies to cease support for “carbon intensive fossil fuel projects,” and urges the World Bank to do the same. Lack of Western financing will impede new production in developing countries, unless climate-profligate China moves to fill the gap.[i]

Biden’s approach also ignores the fact that renewables production relies on China—which accounts for 80% of global supplies of solar panels, 58% of wind turbines, 60% of the rare earths needed for solar energy and ubiquitous semiconductors to power the modern economy, and nearly 80% of the lithium-ion batteries needed for electric vehicles and power storage in a renewables-based electric grid. China is also the largest emitter of CO2 and methane in the world and continues to build new fossil fuel capacity.

Europe has opened the door to new supplies of oil, gas and nuclear power to meet the current crisis. The US also needs a realistic course correction to address the economic and political crisis, and to minimize the environmental damage caused by the need to ramp up production to replace Russian energy exports.

[i] Reuters Staff, “Biden orders U.S. to stop financing new carbon-intense overseas fuel projects.” Reuters, December 10, 2021. https://www.reuters.com/business/energy/biden-orders-us-stop-financing-carbon-intense-overseas-fuel-projects-2021-12-10/

-

This article was originally published here