When China’s economy met the virus: the challenge of deglobalization

For global-minded thinkers, the past half-century has been a mixed-bag: ideological contests were being resolved, struggles against hunger and disease appeared on the cusp of solution, and technology was promising to rewire lives in empowering ways; yet inequality was soaring alongside rising “returns to knowledge,” new vulnerabilities accompanied innovation, and efforts to slow climate change were grossly inadequate. Still, East and West were working much more effectively together, and drawing closer over time. Indeed, engagement with China was one of the foundations for globalization.

In recent years, initial doubts about this partnership with China have turned into a full-blown breakdown in confidence, foremost with the United States but with other nations as well. In 2020, the crisis brought about by the Wuhan coronavirus cleaved China from interaction with the world to an extent never imagined. In time, the virus will recede and be managed, but the more fundamental forces prying China and the West apart will remain. Political scientists and historians remind us that incumbents and rising powers usually suffer from tensions, and often severe ones. For those hoping to steer this clashing couplet back to a rational partnership, an honest and objective stocktaking of the prospects for globalization is essential.

GLOBALIZATION STARTS AT HOME, BUT DOMESTIC ACTIVITY IS SLOWING. China is not just a beneficiary from globalization, reflecting foreign firms’ investment activity in China for instance; the country is also a major contributor. China’s wealth and competitiveness permit its firms to venture abroad and its official lenders to offer Belt and Road development loans and other assistance. But after a four-decade run of success, debt and other problems built up along the way are now limiting China’s potential growth. In fact, China’s GDP data are too smooth to be true. Headline GDP growth has not ranged outside 6.1% to 7.0% in 17 quarters, despite obvious evidence of economic volatility. There is an awkward code of silence in official policy debates—an omertà—in discussing economic problems, and this is eroding Beijing’s credibility. This was true long before “coronavirus” was a household word. The health emergency is putting much heavier short-term pressure on economic activity, bringing it – in fact – to a standstill. And this crisis is a microcosm of the larger threat to domestic growth quality: reluctance to be transparent about the problem of the virus in the early stages undermined a timely response, which allowed the problem to go unaddressed and get out of hand.

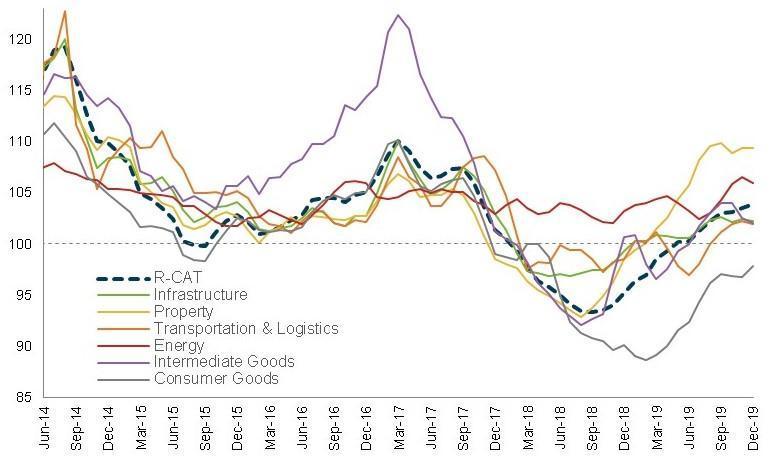

Our Rhodium China Activity Tracker (R-CAT), based on a weighted average of official industrial output statistics, reveals more than the headline data (Figure 1). The R-CAT shows a broad cyclical rebound driving growth from the 2015 doldrums; but it also shows a sharp fall in activity by the end of 2017. This reflects Beijing’s deleveraging campaign, which squeezed that risky shadow banking sector (which works with small borrowers and private corporations) as well as the underregulated interbank markets and the property sector. Beijing started to tighten credit conditions in late 2016 and within two years had halved the pace of credit growth, from around 16% to 8% in 2018. None of this shows in official GDP.

The credit squeeze caused the sharpest industrial slowdown in China since the global financial crisis. By our measure, industrial output growth fell from circa +8% year-on-year (y/y) in Q3 2017 to a -8% y/y trough in September 2018. Property was the hardest hit sector, given developer dependence on shadow financing, as Beijing continued to control property market speculation throughout 2018.

Figure 1 – R-CAT and industry subindicators

Beijing eased monetary conditions from January 2018 to keep borrowing costs from causing a crisis. By May 2018, corporate credit growth started accelerating again, and overall activity growth improved (fell at a slower pace) in late 2018 and into 2019. From April last year, overall activity crawled back into positive territory for the first time in more than a year. Infrastructure construction led the improvement, as Beijing permitted more local government bond issuance to increase investment activity. Consumer goods output is still in contraction, especially in China’s auto sector which is finally starting to turn around from multi-year lows. But, moreover, the recovery did not stop bond defaults (including by government related firms) nor did it stop the first bank failures since the 1990s.

The property sector has played the biggest role in recovery so far, but this is at its limit. In the deleveraging pain of 2018 developers started pre-selling unbuilt units to generate cashflow. They don’t have enough credit presently to complete all those units, and demand for property to actually live in is actually weakening. Coupled with marginally weaker fiscal support in the rest of 2019, trade war impacts, and slower credit growth as financial sector defaults introduce counterparty credit risks, cyclical momentum recovered from a low base but remained tepid.

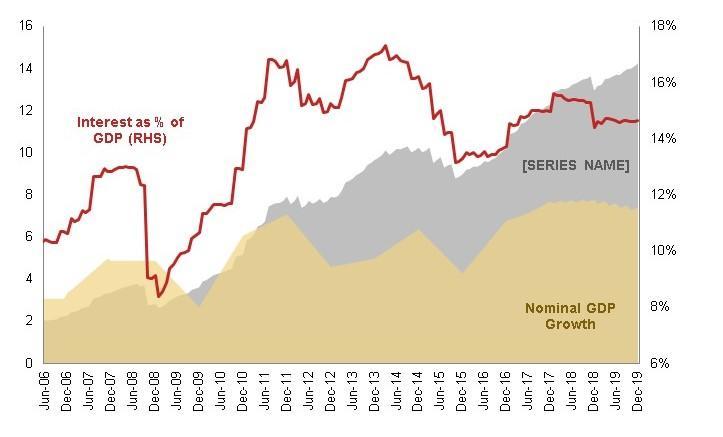

For 2020 China can try to stimulate to buy another year of ostensibly steady growth, or it can return to a greater focus on deleveraging and reduce the severity of a future financial crisis: it cannot do both. As visible in Figure 2, the cost of debt service alone – not even counting loan principal – has grown to twice the value of total national GDP growth every year. This is unprecedented, even for China. And now the coronavirus has forced Beijing’s hand: property developers were forbidden to hold open house showings all across the nation for a long time, and construction workers were kept off the job. As property construction slows, so does GDP. The adjustment challenges China must now deal with as a result of these conditions will force changes in its pattern of globalization.

Figure 2 – Annualized interest on credit and nominal GDP growth

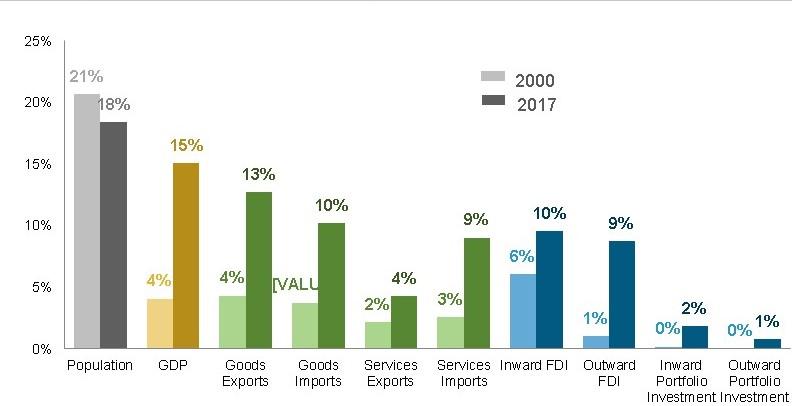

HOW MUCH MORE GLOBALIZATION COULD THERE BE? Before touching on some of the elements of China’s global engagement that are now pulling back as a result of these home-grown challenges (and external pushback discussed below), let us consider where China is and is not already globalized. How much further does China have to go? Figure 3 shows China’s weight in a variety of global economic activities, recently compared to 2000.

Figure 3 – China’s place in the global economy

Source: World Bank, IMF, UNCTAD, Rhodium Group.

The headwinds China now faces have a complex mix of causes. There are the domestic adjustment challenges noted above. There is also resistance coming from abroad. China’s trade surplus has long been among the world’s largest, but advanced economies are confronting that aggressively: not just in terms of border barriers like tariffs and quotas but on deeply systemic elements like soft budget constraints for state firms. Both the intensity of national security limits on exposure to China and the breadth of areas deemed germane to that screening are increasing hugely. Worries about inadvertent exposures to risks associated with China’s model (like poorly managed disease spread, or spillover of debt crises) are growing.

Regardless of the reasons, the straight-line increase in China’s globalization is changing. We prefer to evaluate what that could mean through a four-channel framework: trade, investment, ideas and people flows.

TRADE: AT THE HEART OF THE MATTER. China’s economic miracle depended on trade, and the nation’s growth today remains more trade-intensive than acknowledged. In 2019, net exports contributed 0.7 percentage points to China’s 6.1% GDP growth, its highest contribution in more than a decade. The net exports component of GDP is even more important now in light of limits to investment-led growth as we have known it.

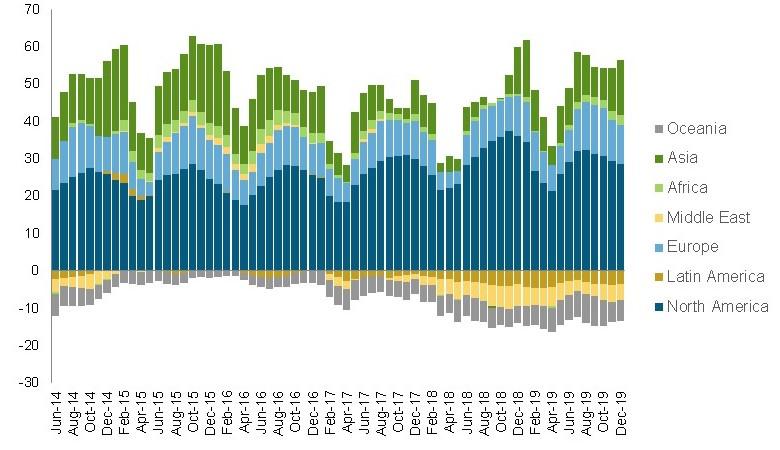

Figure 4 – China’s monthly merchandise trade balance by region

Source: General Administration of Customs, RHG calculations.

Not only is China trade-dependent but its greatest dependence is on the United States. China maintains deficits with commodity exporters in Latin America, Oceania and the Middle East, and a weak European growth outlook limits potential for China there (see Figure 4). But China’s US surplus is equivalent to more than 70% of its total merchandise surplus – up from only 50% in 2016 – despite trade war rhetoric. Trade disruption still to come will cause yet unrecognized economic pain in both nations.

China’s current account surplus hit $350 billion in 2007 – a peak of 10% relative to GDP – with one-fifth of merchandise exports headed to the US. Since the financial crisis, credit rather than trade expansion drove China’s economic growth, with net exports contributing negatively in seven of the last ten years. The first quarter current account balance even briefly dipped into deficit in 2018 for the first time since 2003.

But this official, aggregate picture is misleading. China’s trade imbalance is higher than reported, and the persistent asymmetries with the US and Europe remain toxic despite the overall fall in China’s surplus to GDP ratio. The falling trade surplus in recent years was partially driven by a services trade deficit disguising “hot” money outflows. Independent estimates show China’s 2018 trade surplus higher by $85 billion – 1.4% of GDP instead of the official 0.8% of GDP. Rising import prices also weighed down the trade balance: while the goods surplus was around 3% of GDP in 2018, the manufacturing surplus was more than double that level, with commodity net imports equivalent to 4.2%. In the first half of 2019, net exports contributed more to GDP growth than in any first-half period in the last decade as its US surplus swelled under tariffs.

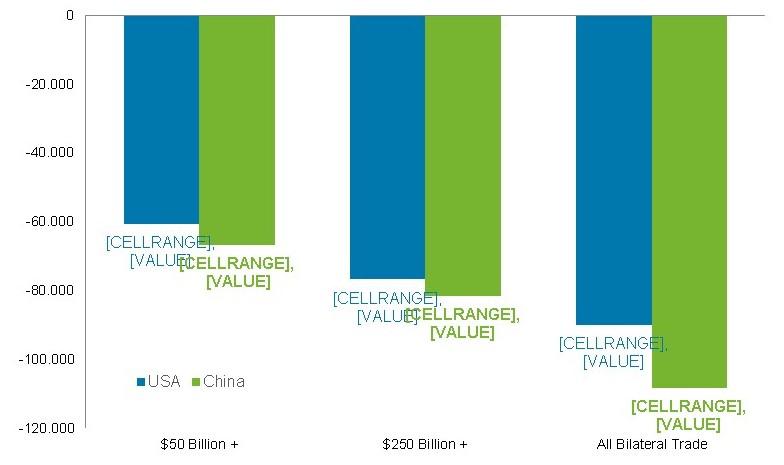

This degree of US-China trade interdependence means the cost of decoupling is high – higher than anyone wants to talk about. Our estimations show the current 25% tariff in place will cost the US $77 billion in foregone GDP in 2020; that number rises to $90 billion if threatened tariffs on all bilateral trade proceed (Figure 5). China’s GDP is hit harder, by nearly $82 billion in 2020 or 0.5% lower than status quo ante baseline. Cumulative foregone US GDP from 2018 to 2020 is roughly equivalent to the 2019 California state budget, or the economic damage wrought by Hurricane Katrina.

Figure 5 – Estimated impact of tariff escalation on annual GDP in 2020

Source: GTAP model, RHG calculations. Model takes 2017 as a base year for status quo ante conditions, and scenarios estimate impact of 25% tariffs.

This does not tell the whole story. Estimations of the costs of a “trade war” so far – even those of RHG – are rough and limited, measuring only what we know how to measure. Trade connects to almost all aspects of our lives and social systems, and our productivity and national security are deeply intertwined with global supply chains in ways that economic models do not capture. The true cost of decoupling would be even more sobering than the already disconcertingly large projections of impacts on trade flows alone.

INVESTMENT: IF YOU OPEN WILL THEY COME… OR GO? In trade, China has already shaken the world; in investment – as Figure 3 made clear – the impact has not really started yet. There are two investment channels that concern us when talking about China’s financial globalization: direct investment (companies investing to build businesses) and portfolio investment (financial investment in stocks and bonds). In both cases China is still greatly underweight in the world, in terms of the stock of activity. This means that for the future there is the potential for tremendous growth. But this will not be automatic tomorrow, any more than it has been in the past: it requires policy reform from Beijing to build confidence among investors at home and abroad. To measure the trend in China’s investment globalization, we need to look at the sum of all cross-border investment flows divided by the value of China’s gross domestic product.

Figure 6 tells the surprising story found in these data. Over the past decade China has consistently withdrawn from the global financial economy, as cross-border activity has diminished relative to the domestic economy. From 2012-2017 this can be attributed to a series of failed attempts at financial reform: interbank market reform, equity market opening, currency internationalization and financial account opening were all attempted by Beijing but then rolled back in the face of the ensuing economic instabilities. Since 2016, these internal challenges to China’s financial globalization potential have been joined by greater external impediments, as advanced economies – foremost the United States but also Europe and others – have implemented new limits to Chinese flows to curtail investments seen as national security risks or the result of unfair subsidies. On January 14, 2020, for example, the European Union, Japan and the United States issued a trilateral pledge to counter unfair industrial subsidies and supports that harm their interests, an endeavor that will close doors to many Chinese investment outflows.

Figure 6 – Gross sum of cross-border investment flows

Source: State Administration of Foreign Exchange, Rhodium Group. Excludes reserves.

The bottom line is that the potential for China’s investment globalization is vast, and flows both into and out of China could increase by trillions of dollars in the years ahead, but all this is contingent on policy reforms. The world needs to be sure of China-OECD systemic compatibility, and that is presently diminishing rather than coming together. That vast potential is also contingent on Beijing demonstrating that it can control the epidemic spread of diseases and pathogens like coronavirus, by dealing with the lax conditions that gave rise to the new virus in the first place, and by accepting the liberalization and freedom of speech necessary to permit recognition earlier. These are deeply political, social steps forward that will not be easy for a Communist Party that celebrates orthodoxy and control.

IDEAS. Derailment of the globalization trend of the past five decades could have the biggest impact on China in the realm of ideas. This channel of activity is trickier to quantify than trade or investment. The flow of ideas includes China’s ability to export and shape technology platforms like its regimes for leading companies in 5G telecommunications systems. It includes the free exchange and interaction of academic researchers and laboratories. And it includes attitudes toward embracing the Chinese political model and ideas about the acceptable levels of debt and political repression during the economic development process.

Until recently, China’s growing global presence in each of these areas was seen almost as an inevitability. Chinese firms were permitted to invest, license and operate with tremendous freedom and enthusiasm in industries at the forefront of innovation and technological development (such as the American information and communications technology sector). This permissive environment amplified the uptake of Chinese standards worldwide, and led to a tremendous amount of knowledge exchange.

Deglobalization, whether driven by nativistic campaigns rolled out by Beijing at home or by hawkish mistrust of the consequences of embracing Chinese technologies and ideas abroad will greatly reduce China’s productivity. Our 2016 research argued that a major portion of China’s innovative potential derived from partnership with foreign technology companies. While China’s indigenous innovation policies catch up to some degree, they cannot replace the value of open interaction with research activities around the world, and that collaboration is now being heavily policed not just by Washington but by Brussels and by most advanced-economy capitals. Intellectual property problems of the first order have heightened scrutiny of Beijing. Restoring the flow of knowledge and ideas is critical to China, and to the rest of the world: the coronavirus in many ways reminds us of that.

PEOPLE. Finally, the implications of deglobalization for China should be considered through the lens of people flows as well, which is something that little analysis has to date tallied. The increasingly free movement of citizens between China and the world has brought tremendous economic benefits over recent decades, both for China and the world. Tourism flows in both directions have generated hundreds of billions of dollars in new economic activity. China’s Academy of Social Science estimates that tens of millions of its citizens are working around the world in sectors such as engineering and construction services, and in manufacturing as well (in Prato, for instance). This has become a major formal and informal avenue for wealth creation for lower-skilled Chinese workers. Upwards of half a million post-secondary students from China are studying outside the country, both a boon to host-nation services exports and to China’s human capital formation. Often overlapping the education vector is the presence of Chinese researchers in R&D laboratories around the world, where they play a key role manning the front lines of commercial science in many fields.

CONCLUSIONS. Deglobalization is not just a theory or possibility, but a reality today. The pace of economic integration between China and the world has stalled and in some cases reversed. The spread of Covid-19 is a tragic unanticipated short-term amplifier of the decoupling which was already afoot. Eventually, the virus will subside and be mitigated with better containment practices and perhaps a vaccine. But the authoritarian lean in today’s China will remain thereafter. While often driven by those internal Chinese challenges and tendencies over the past decade, action to more intensely regulate the free flow of activity with China is evident not just in the United States but in most other economies. On the one hand, a stock-taking of permissive attitudes was to be expected as China grew into a more formidable economic competitor. On the other hand, much of the push back is not rooted in market competitiveness but in state-interventions or policy problems on the Chinese side, and these raise much less tractable concerns.