The pandemic and the power sector

In this twenty-fifth year of Aspenia, CESI is stepping up to contribute to the international debate on energy. This special issue looks at climate change from a variety of angles and focuses on plans and projects to limit greenhouse gas emissions without forgoing economic development. The global pandemic – an extremely rapid, symmetrical, and multidimensional crisis – is certainly hampering progress and introducing new, difficult challenges. But our ultimate goals stand fast. CESI tries to investigate why COVID-19 has represented a stress test for the energy system and what this means for our energy future.

In a short period, the pandemic emergency has destabilized the global economy and changed the behaviors of multiple spheres of human life. The lockdown and the closing of borders, enacted to slow the propagation of the disease, have seriously affected a wide range of industries. The whole global economy is suffering, as aggregate demand has collapsed and as employment levels have taken a dive.

Recently, a wide range of analyses, forecasts, and estimates have been presented on the global impact that Covid-19 will have on various economic sectors. In June, the International Labor Organization (ilo) estimated that during the second trimester of 2020, 10.7% of working hours were lost due to the pandemic, as compared to 2019. This is the equivalent of approximately 135 million full-time positions. The study, entitled “Covid-19 and the World of Work”, identifies the geographical areas that have been most affected: the Americas, followed by Europe and Central Asia. According to ilo, the economic crisis set off by the pandemic will cause 25 million people to lose their jobs, globally.

The World Bank also highlighted the difficult situation in its Global Economic Prospects Report, also published in June. The document, which examines 183 countries, estimates that this is the worst economic collapse since the second world war. Data for 2020 indicates that global gdp could decrease by 5.2% — more than twice the collapse of the 2008 financial crisis – with an average 3.6% decrease in pro capita gdp in over 90% of countries. This means that there could be 70-100 million people surviving with less than 1.9 dollars per day and thus living in conditions of extreme poverty. Trade could fall by 13% and emerging and developing economies contract by 2.5%. However, advanced economies (with further to fall) will suffer the most marked effects.

On May 6, 2020, the European Commission published its Economic Forecast for Spring 2020 with the expected results and projections for the first semester of the year. Interestingly, the document describes the shock to the eu economy as “symmetrical”, as the pandemic has affected every member state. This forecast estimates a contraction of 7.5% in 2020 and a growth of 6% in 2021, while the figures for 2020 production will vary in each member state (from -4.24% in Poland to -9.75% in Greece). The economic recovery of each country in 2021 will depend on the national state of the pandemic, on its economic structure, and on the ability of each individual state to implement stabilization policies.

A DIFFERENT CRISIS WITH A MULTISECTORAL IMPACT. The current crisis sets itself apart from others, which have been sparked primarily by the financial system or have been due to sociopolitical reasons, with different degrees of effects on the global economy. Today’s health crisis is characterized by a vast array of dimensions – social, economic and geopolitical – involving all sectors of the economy. This is a total crisis that has had severe economic consequences for all sectors related to non-essential goods. The GlobalData Executive Briefing, updated regularly and available online, describes the situation well.

While the automotive industry has registered a loss of over 100 billion dollars just in North America and Europe, forecasts for the construction sector indicate a global contraction of 1.4% in 2020, a net change compared to the pre-Covid-19 forecast of +3.1%. The impact on retail sales is described as devastating, while there was an increase in online purchases during the lockdown period. The crisis has also heavily affected the fashion industry with the cancellation of orders following the closing of shops.

The travel and tourism sector have encountered severe backlashes. During the period prior to the pandemic, the sector had reached a 10% share of global economic activity, totaling $8.8 trillion. The decrease in airplane travel has led to a loss of $113 billion and, according to a September report by the World Travel & Tourism Council, 50 million individuals employed in this sector are at risk of unemployment (including some 30 million people in Asia alone).

Foreign trade, which currently registers -13%, has not only been damaged by the restriction in the mobility of people, goods, and services, but also by the new economic tensions between the United States and China and by general geoeconomic uncertainty. The forecast for 2021 only points to a partial recovery that will be slowed down by a weak global demand and by interruptions in the global value chain.

OIL INDUSTRY EMERGENCIES. Undoubtedly, the implications for the energy sector have been significant, with multiple aspects involved due to the wide variety of areas comprised within the energy ecosystem. One of these, the oil & gas sector, has suffered not only because of the pandemic, but also due to new tensions around this product. On the one hand, the price of oil has fallen precipitously due to a 30% contraction in global demand (especially from China, which alone accounts for 10% of global oil imports). According to the International Energy Agency, global oil demand has fallen to just 90,000 barrels per day since the beginning of the crisis. On the other hand, the excessive supply of oil in global markets is leading to competition among the main oil exporters. The dynamics arising from this competition has already led to a fall in the average price of oil to just $30 per barrel.

On April 12, at another opec-plus meeting, oil-producing countries agreed on a historical cut: 9.7 million barrels per day, or about 10% of global production. These new production quotas, which started on May 1, will be valid for two years, with decreasing reduction rates. During the first two months, cuts totaled the announced 9.7 million barrels per day. The cuts are now being reduced to 7.6 million barrels per day for the rest of 2020 and then 5.6 million barrels until April 2022. Oil market estimates hypothesize a slow return to an average price of $30 per barrel in 2020 and $45 in 2021.

IMPLICATIONS FOR THE POWER SECTOR. Considering the whole energy sector, the current pandemic represents the most severe drop in primary energy demand since World War ii, according to the IEA Global Review 2020 (published in April). This analysis underlines the fact that each week of full lockdown causes a decrease of 25% in energy demand, whereas a partial lockdown induces just a 18% reduction, per week. The study estimates a worldwide contraction of 3.8% of primary energy demand, which will reach a 6% reduction for the entire year of 2020.

The most surprising data, however, concerns global co2 emissions, which are expected to decrease by nearly 8%. If this estimate is correct, that would mean their lowest level since 2010. This would be the greatest reduction in emissions ever recorded – six times larger than the previous record of 400 million tons in 2009, also caused by a global financial crisis.

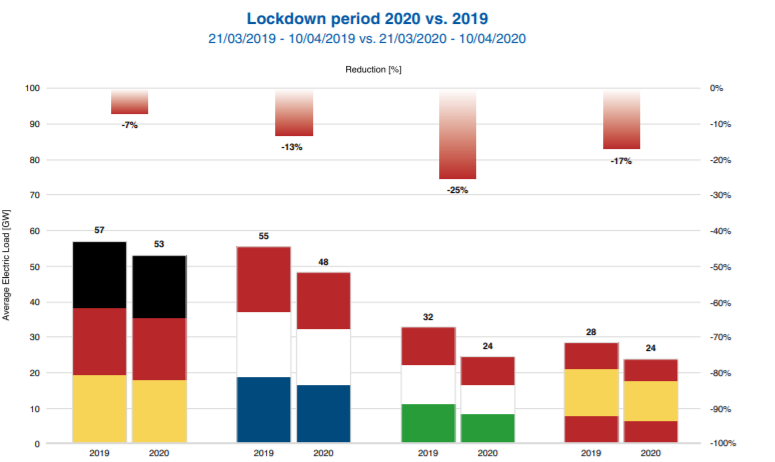

Narrowing in on the electricity sector, cesi has developed an extensive study to quantify the effects of the pandemic on European power systems, with a focus on Italy, Germany, France and Spain. The analysis reveals that during the lockdown, Italy experienced a decrease of 25% compared to the same period in the previous year, the deepest relative reduction in Europe. Germany, France and Spain registered a decrease between 7% and 17%. Today, as our societies emerge from the lockdown period, Italy’s recovery is not aligned with other European countries: Italy registered a reduction of 13% compared to 8% in Germany, France and Spain.

One of the effects of the decrease in demand has been a serious reduction of day-ahead market prices on energy markets. During the lockdown, the prices in France and Spain decreased by 63% and 62% respectively. Germany had a reduction of 55% whereas Italy’s prices were 49% lower. The lack of alignment between Italy and the other three countries is clear: Italy’s day-ahead market price was 24 euro per megawatt hour while the others presented a price between 14 and 19 €/mwh.

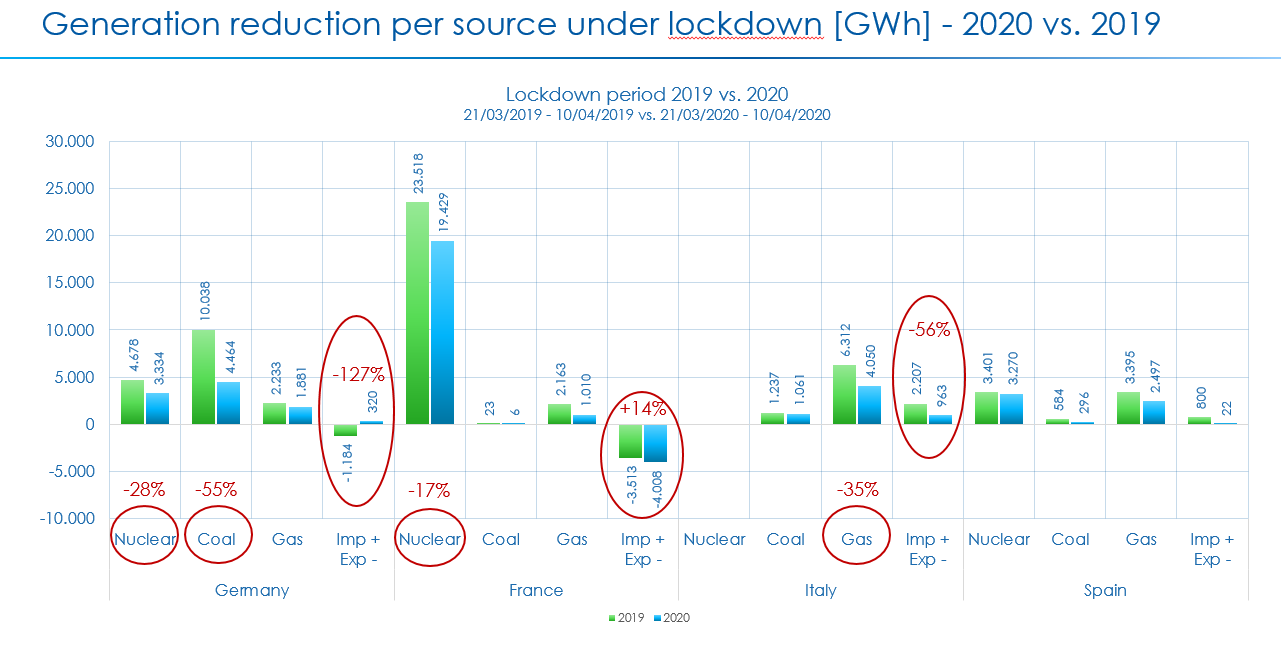

The reduction of electricity demand has also specifically affected the power generation mix in the various countries. Comparing the lockdown period with the equivalent period in 2019, Germany presents a contraction of almost 30% of nuclear energy and 55% of coal, shifting from exporting to importing energy. France shows a decrease in power generation from nuclear energy, with 17% less energy from this source; Italy presents a 35% reduction from gas-fired power plants and 56% from electricity imports.

In general, in order to balance the different national energy systems and guarantee their stability, a drastic reduction in electricity import capacity has been observed across Europe. This has led to a collapse of cross-border energy trading and market fragmentation, with an overall reduction of the Net Transfer Capacity from 7-8 gigawatts to less than 3 gw in the case of Italy.

A PREVIEW OF A FUTURE DECARBONIZED POWER SYSTEM. Despite everything, however, the pandemic has also had some positive effects on our power systems. For instance, we have witnessed a sharp decrease in emissions. We have also seen an increase of renewables. Along with the reduction in demand, this increase has led to a substantial leap in the renewable penetration index – that is, in the ratio between energy produced from renewables and the power load.

Indeed, according to IEA, renewables will be the only source of energy to increase in 2020, with a quota of global generation that is expected to grow thanks to priority in dispatching and low operative costs.

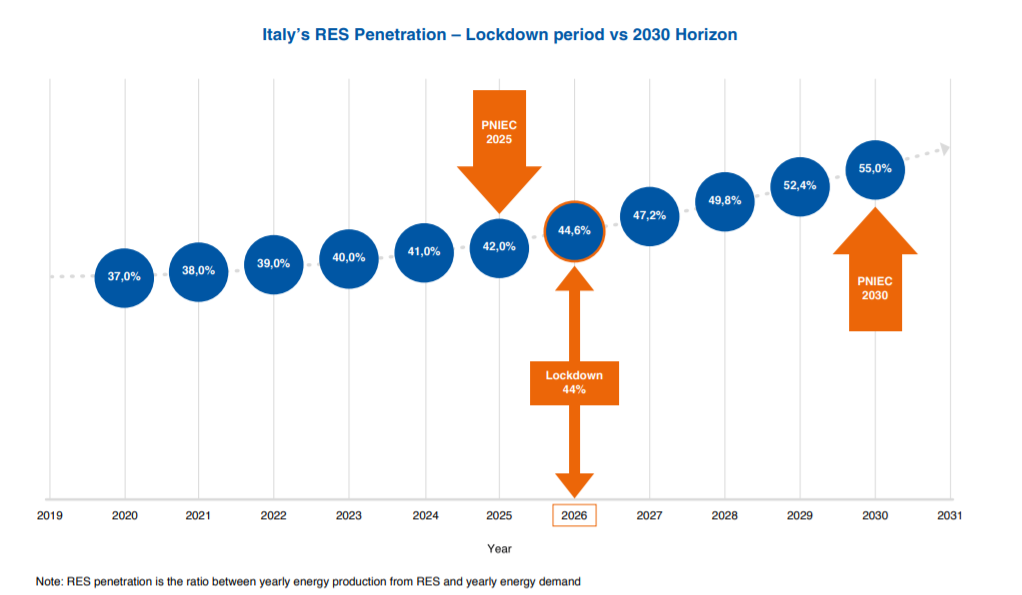

cesi analyses reveal that the penetration of renewables in Italy reached 44% during lockdown, which compares favorably to the 30% recorded in the same period of 2019. Comparing these figures with the projections of the Italian Integrated National Plan for Energy and Climate (as shown in figure 3) provides some illuminating discoveries. First, for example, the lockdown was a “sneak peek” into the future: the power system situation we experienced in Italy actually closely resembles what we expected for 2026.

Second, during the crisis and despite an unprecedented situation of a high share of non-programmable and volatile renewable generation, the Italian power sector benefited from recent investments and was able to guarantee energy supply security to citizens and firms.

Third, the cost of energy in the ancillary market increased by 57%. This was not due to the cost of renewables, but rather because of the power grid, which proved not to be ready to accommodate a large share of renewables yet. As a matter of fact, in order to ensure a security of supply with a large share of non-programmable energy resources, the grid was forced to curtail or reduce cheap energy sources – clearly a suboptimal decision. What happened clearly shows that if the power grid is not made ready to accommodate a large share of renewables – through proper de-bottleneck investments and market reforms – we run the serious risk of not fully exploiting all the environmental and economic benefits of renewable energy.

The key lesson from the pandemic, for our sector, is an understanding of how urgent interventions have become on the power grid and on the market structure. The alternative to prompt action and reform is to accept a destiny of a structural decarbonization without a decrease in energy costs for the final customer.

NEW INVESTMENTS FOR A GREEN ENERGY SECTOR AND AN EFFICIENT ECONOMIC RECOVERY. cesi analysis identifies three main elements which can secure reliable clean power by improving the grid’s resiliency:

- Adequate market design: A proper design of power markets, from capacity to ancillary service markets, is needed. A proper cross-border coupling of power markets is crucial.

- Adequate infrastructures: Additional power transmission infrastructures must be developed to allow unconstrained energy flows from areas with high production of renewables to load centers.

- Adequate flexibility: Resources characterized by proper levels of flexibility should be ensured in the system, including conventional and non-conventional storage.

These measures can be leveraged by a single cross-cutting technological element: digitalization, which facilitates running smooth and efficient power markets and systems thanks to the real-time availability of enormous amounts of data.

Indeed, the global power industry is starting to clearly understand that data is the new oil. In the future, and especially after the Covid-19 crisis, competitive advantage will be driven by individual firms’ ability to manage data and algorithms. Alec Ross, a technology expert who teaches at Columbia University and was Obama’s senior advisor on innovation, believes that as machine automation and big data expands, the global economy will undergo a revolution driven by artificial intelligence. The enormous learning potential of these devices will have “effects on the work force as significant as the previous agricultural, industrial, and digital revolutions.”[1]

The applications of digital technologies in the energy sector are various and embrace its entire value chain: from generation to transmission and distribution, up to the end customer. Some of these innovations involve renewable energy forecasting and trading, predictive maintenance, smarter and automated operations, advanced distributed energy resources aggregation, peer-to-peer transactions, and automated energy demand management; taking advantage of all these elements would allow the potential of renewables to be realized while also ensuring the power system’s security of supply.

Introducing such advanced technologies requires investments to drive the general economic recovery. The International Renewable Energy Agency recently published the “Post-Covid recovery: an agenda for resilience, development and equality” report[2], where some of the economic impacts of clean investments are quantified. The study provides a detailed roadmap for 2021-23 with an outlook towards the end of the decade in 2030.

According to irena’s forecasts, doubling annual investments in the energy transition (nearly 2 trillion dollars per year for the next three years) would provide a significant impetus to the energy sector’s recovery, accounting for 1% of global gdp and 5.5 million new jobs over three years. This amount includes private sector investments (up to 75%) which could be raised to implement a full series of priority measures. Jobs associated to renewables could triple, reaching 30 million employees by 2030. In fact, every million dollars invested in green resources generates three times more employment than investments in fossil fuels. Additionally, in June 2020, analysts at Goldman Sachs confirmed their projection that investments in renewables will represent 25% of the total energy expenditure in 2021; for the first time ever, renewables will overtake the sales of traditional fossil fuels such as oil and gas.

R&D FOR A BRIGHTER FUTURE. From this perspective, the role of research and development will inevitably prove pivotal if we are to design the most suitable and the most beneficial solutions for future decarbonization. In fact, global low-carbon-emission energy technology represents about 80% of total public expenditures in r&d in the energy sector ($30 billion in 2019). However, the overall percentage of gdp dedicated to r&d in the energy sector has remained constant over the past decade, whereas other public research sectors (such as health and defense) have received nearly five times more funding than the energy sector.

A survey conducted in mid-2020 by the Smith School of Enterprise and the Environment at Oxford University (“Will Covid-19 fiscal recovery packages accelerate or retard progress on climate change?”) has certified the consensus on clean energy technology. Analyzing the various expense options, over 200 central bank officials, finance ministry officials, and other economic experts from G20 countries, it appears clear that the priority is to invest in clean energy research and development and in clean energy infrastructure. The shift to more sustainable energy systems, together with long-term economic multipliers, guarantees a positive impact.

According to the IEA, the European Union must grasp the opportunity to accelerate the energy transition during the post-pandemic recovery by making the most of the Green New Deal. In particular, our sector must take advantage of the economic recovery package and the additional 750 billion euro provided through the Next Generation eu (Recovery Fund) proposed at the end of May 2020 by the Commission in Brussels. By doing so, the eu could implement its decarbonization plans and meet its goals for 2030 and 2050.

Investments and technology by themselves, however, are not enough. They need to be leveraged through a clear regulatory and legislative framework, agreed by all the relevant stakeholders. This will ensure streamlined authorization procedures for implementing infrastructural projects quickly. If we truly want to support the post-pandemic global economic recovery, we desperately need uniform, simplified eu and national regulations to complement technology and financing. This is a call to action for policy-makers in Europe and around the world.

Footnotes:

[1] Alec Ross, The Industries of the Future, Simon & Schuster, 2017.

[2] IRENA, “Post-Covid recovery: an agenda for resilience, development and equality,” June 2020. See also the article in this issue by The Global Commission on the Geopolitics of Energy Transformation.

*This article was published on Aspenia magazine 89-90