Natural gas pricing mechanisms and the current crisis: drivers and trends

The European Union is facing the worst energy crisis since 1973 and has entered into a new phase of its energy system. Such transformative and challenging times are visible in the European gas prices, which have steadily recorded historically high levels since 2021. The rise of gas prices has several energy, economic and political consequences. They have caused an increase in electricity prices as well.

Given the pivotal role of gas in the European energy and economic system, gas prices have become a key political issue as their significant increase can dampen economic activity, affecting both the consumption side (by reducing households’ real disposable income and purchasing power) and the intermediate goods channel (by forcing industry and firms to reduce productivity and face higher costs). In short, the extraordinary spikes could deeply undermine European economies and social stability.

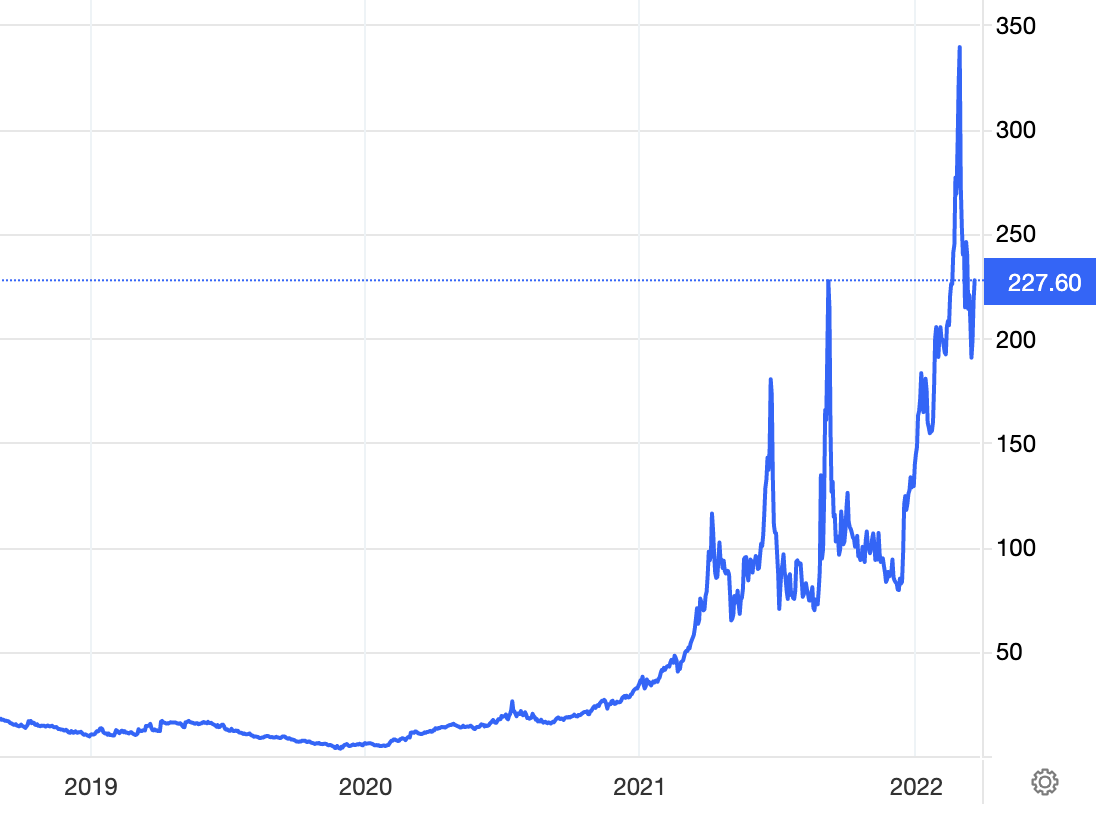

For these reasons, European governments have considered several measures to tackle rising gas prices. The great variations in gas prices over the past year (from 40 € per megawatt hour, MWh in August 2021 to record levels 339 €/MWh in August 2022) have generated questions on how gas prices are set and what the main causes of the recent spikes are. Furthermore, gas pricing mechanisms are particularly relevant for both suppliers and consumers and entail several consequences, worthy to be addressed given the extraordinary times.

Read also: The Ukrainian conflict and the long story of energy pipelines

Throughout the past three decades, gas markets and prices have evolved, underpinned by economic and political factors. Natural gas has been characterized by a regional peculiarity compared to other internationally traded commodity markets, such as oil. This is mainly due to the fact that gas has higher transportation costs given its gaseous nature, compared to the liquid nature of oil. This explains why most of gas is consumed and produced locally or regionally (rather than globally as for oil) making international gas trade historically quite limited.

Generally, natural gas prices fall into three categories depending on the degree of regulation, the competitiveness of the market, and market liquidity: i) government-regulated prices (usually based on cost of service); ii) price indexation to competing fuels (usually oil-indexed); and iii) spot market pricing in competitive gas market.

At the beginning of the gas industry in the middle of the XX century, exchanges were mainly conducted through gas pipelines. The dominant mechanism for the international gas trade in Europe was related to long-term contracts and oil indexation. This model, which originated in Europe in the 1960s and spread to Asia, was in contrast with a mechanism based on hub pricing and trade markets, developed in the United States. The use of long-term contracts responded to exporters’ need to have stable demand and secure financial income in order to motivate capital intensive investments, such as developing gas fields and transport infrastructure like pipelines. Oil indexation, instead, was also motivated by the desire to make gas competitive via-à-vis other fuels to be displaced in thermoelectric and heating sectors. This pricing mechanism did in fact facilitate the rise of the gas industry, guaranteeing security of supply and relatively predictable prices.

Over the past decade, however, the gas market has started to become more similar to the global oil market. Rising LNG traded volume has contributed to making gas markets more interconnected. While piped gas generates a rigid interdependence between suppliers and consumers, LNG gas provides more flexibility with suppliers being able to respond better to variations in different gas markets (and prices). This was accelerated by the shale gas revolution, which allowed the US to become a gas exporter, creating a situation of global gas oversupply.

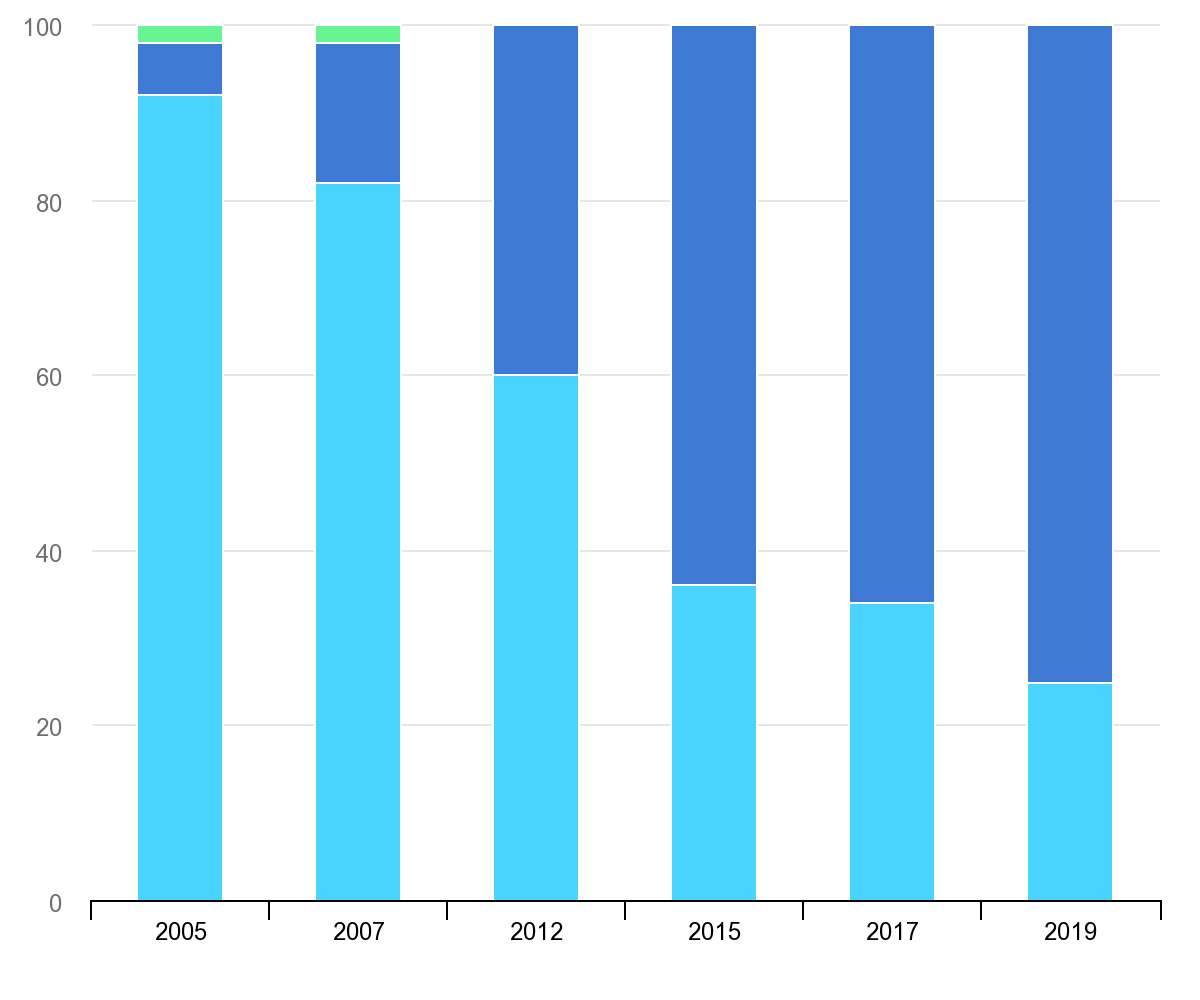

The oil-indexation pricing mechanism dominated gas trade until 2009-2010. Since then, the model started to weaken due to several factors, such as liberalization of gas markets, regulatory pressure and oversupplied gas market, which led the expansion of spot-indexed[1] gas supplies and especially gas-to-gas competition. This deep transformation is visible in the evolution of import prices in Europe, with the share of oil-indexation falling from above 90% in 2005 to below 25% in 2019.

Nonetheless, many import contracts feature hybrid formulas combining hub indexation and oil indexation. What is clear is that these formulae (hybrid- and hub-indexed) are more reflective of the actual supply-demand fundamentals of the importing market. In Europe, the main liquid hubs, where gas is exchanged and prices are set, are: the National Balancing Point (NBP) in the United Kingdom and the Title Transfer Facility (TTF) in The Netherlands. Established in 2003, the Dutch TTF has now become the reference for European gas prices.

Spot markets brought large benefits to consumers. However, the new model performed well during previous periods characterized by oversupplied markets (and low gas prices) and a stable energy relationship with the main suppliers (such as Russia). This landscape was changed in 2021. Indeed, Europe had come from years of low gas prices (between 2012 and 2020 the price hovered at around €20 MWh). The lowest point was experienced in 2020 (the TTF set natural gas prices at around €3.5 per MWh in May 2020) when lockdowns and restrictions in the attempt to limit the COVID-19 pandemic had dramatically and artificially reduced energy demand and prices.

Since 2021, gas prices have been surging along with other fossil fuel prices. The initial rise was driven mainly by market fundamentals. In 2021, health restrictions were generally lifted and energy demand was free to rise again and did so strongly, underpinned also by massive recovery plans launched by governments in the aftermath of the pandemic. Moreover, a combination of causes (longer winter, technical issues and lower wind and hydro generation around the world) incentivized higher global gas demand.

Read also: Soaring energy prices and the Eastern European crisis: the need for a European market redesign?

Yet, energy supply had not managed to follow and keep pace with the rising energy demand, contributing to the energy price spike of 2021. Supply remained tight following years of subdued investment in the energy sector (caused by the combination of low energy prices and climate targets).

Then, geopolitical factors stepped in, exacerbating market weaknesses as political and military tensions linked to Russia’s invasion of Ukraine were mounting. Already prior to the conflict, Russia decided to only respect its contractual terms, avoiding selling above contract gas on the spot market, as it had done in previous years, despite high prices. Moreover, it decided to not fill its European storages in 2021, further exacerbating European energy fragility. Natural gas prices have further soared following Russia’s invasion of Ukraine in early 2022, given the risk of disruptions to trade, concerns over future supply and the European commitment to phase out Russian imports. Gas prices almost quadrupled from April to October. Since then, Moscow has decided to increasingly weaponize its gas supplies by tightening volumes in European markets. The latest move was the decision to indefinitely halt Nord Stream1. The high levels of gas prices allowed Russia to record incredible profits (with less supply).

Many observers and policymakers have expressed their doubts over the well-functioning of TTF, given the great price volatility and short-term price variability, warning about the role of financial speculation. While speculation may be part of the equation of today’s rising gas prices, given rising financialization of gas trading, it cannot be identified as the main party responsible. The success of the TTF was determined by a combination of gas infrastructure characterized by vast spare capacity on all the interconnectors), easy access to the global LNG market, robust underground gas storage and the largest European gas field in Groningen. These factors have increasingly changed. The Dutch domestic production declined and the spare capacity on gas infrastructure have become increasingly scarce given higher LNG imports and lower Russian gas flows to Europe.

The current gas crisis and its price spikes are motivated by mainly a supply-demand imbalance caused by several factors. One is the decoupling from a crucial supplier (Russia accounted for 45% of EU gas imports and almost 40% of its total gas consumption in 2021). Another is Europe’s willingness to rely more on LNG has put the EU in competition with other importing regions, notably Asia, reiterating the globalization of gas markets. So far, high gas prices have been instrumental in attracting higher LNG volumes to Europe. Lastly, the mandatory targets to refill European gas storage and universal subsidies have sustained gas demand exacerbating the issue. Given tighter gas supplies, the only way to reduce gas prices will be by cutting gas demand.

[1] Nothing prevents parties from adopting hub pricing mechanisms in long-term supply contracts.