Homes for Americans: a worsening problem

“Right here in America, if you own your own home, you’re realizing the American dream.” Former President George W. Bush said in a 2002 speech. Indeed, is there a better embodiment of the American lifestyle than a single home with a picket fence surrounding a lawn? Yet, Americans are struggling like never before to get into the homeownership game.

And it is not that Americans do not buy homes because they prefer to rent them. It is that there are no homes—to buy or rent—that they can afford. Recent estimates by Up for Growth, a non-profit focused on affordable housing, reveal that the overall shortage of housing is close to four million homes across the nation, and things are even worse considering that some of the available inventory is unaffordable to most. Overall, as many as seven million homes are missing for low-income people in the US.

That leads to a whole host of problems, from young people’s inability to form new households and move out of their parents’ homes, to difficulties in moving to follow better professional opportunities, to all out homelessness.

US v. Europe

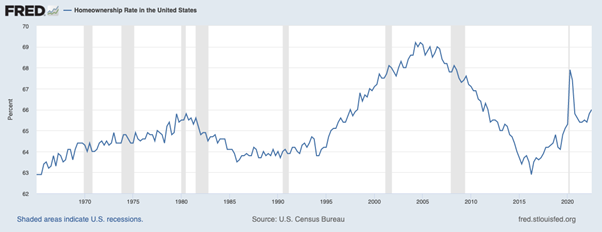

Historically, home ownership in the US has ranged between just above 60% in the 1970s to the peak of the subprime mortgage-fueled real estate bubble, when ownership was around 69%.

Even then, it was still below the typical rate of home ownership in countries like Singapore (90%), or many European countries such as Italy, Belgium, or Spain, all countries where more than 70% of the population lives in a home that they own.

This is not necessarily a problem: the percentage of people owning homes does not always correlate with the standard of living of a country, especially where it is easy to rent. Think about Germany, where about 50% of the population owns a home, or Switzerland, which at 34% has the lowest home ownership rate of western Europe.

Yet, in countries like Germany or Switzerland the low rate of home ownership does not translate into trouble finding housing, as it does in the US where there is a historical shortage of affordable homes and rentals.

It is almost twice as difficult to afford a home today than it was only a few years ago in 2013. The causes are varied, though two stand: the fallout of the Great Recession of 2008-2009, which was caused by a real estate bubble and spurred more than a decade of underbuilding; and the concomitant explosion of the adult population.

Rent is too high. And forget about buying

That, for one, translates into homelessness: a 2019 study, for instance, found that much more than mental health problems, including addiction, housing prices are a predictor of the rates of homelessness. More than half a million Americans do not have a home—and they are in all corners of the country.

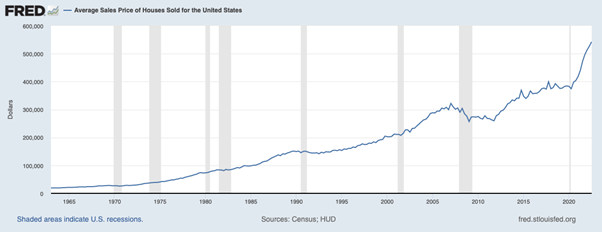

Historically, housing shortages and homelessness were concentrated in coastal areas and big cities, where real estate prices are often sky high. However, recently they have reached the rest of the country. In the second quarter of 2020, the average home sold for $374,500. Two years later, the price is up almost 50%, with the average home sold for $543,000. Rents have gone up accordingly.

To be fair, homelessness rates in the US are broadly in line with those in many European countries, and while they are getting worse, the overall numbers are still below historic peaks.

Meanwhile, the lack of affordable homes has begun to impact even on those who are housed. Younger people, for instance, who cannot afford to buy or even rent, are unable to leave their parents’ homes, get married, or start families. Regarding renters overall: Nearly half the US population is housing-cost burdened, spending over 30% of their income in rent, and with increasing prices many are forced to cut spending on other basic needs, such as food, clothes or transportation.

The barriers to creating housing inventory

The problem, experts say, begins with inventory: there are not enough homes available, especially affordable ones. The US has a gap of millions of homes, and its construction rate of 110,000 homes a year will do little to fill it. That is due to several overlapping problems.

First, according to Chris Herbert, who manages the Center for Housing Studies at Harvard University, are regulatory barriers that make it hard to develop the kind of small, dense housing that comprises the bulk of affordable homes. In cities like Atlanta, Georgia, which is almost 81,000 homes short, it is only possible to build big apartment buildings downtown, and large single-family homes elsewhere. This means there is no in-between choice for people who might not have the budget for a home, or to buy downtown where prices are higher. In addition, local owners often oppose change to the existing regulations. It is the old NIMBY (Not In My Backyard) issue: people who own houses in a certain area oppose construction around them, particularly of the kind they perceive would lower the value of their property. They are often able to mobilize enough political and financial capital to stop developments and zoning updates.

Those developments that are happening delayed by the lingering pandemic supply chain disruptions. Anything from lumber to fixtures takes longer to be available and costs more, further driving up the costs of any new inventory.

Finally, there is the demand. It soared during the pandemic as Millennials, the largest generation in America’s history, fully entered adulthood. Those who found themselves with more disposable income as they were no longer spending outside the home, and in need for more space to work remotely, began buying homes, and quickly. Low-interest mortgages helped them move quickly, and they bought the available homes, driving prices up 30% in just two years. Housing vacancy went down to 0.8% for buyers (and 5.8% for renters), driving prices further up, and rising interest rates pretty much erased what little opportunity was left for millions to afford a mortgage, and a home.

What are the solutions?

One thing is sure: high demand for homes is not going away anytime soon, or not until it is met by similarly high supply, and at reasonable prices. This can be achieved but requires intervention in different areas: increase in housing inventory, and support in making such housing affordable.

When it comes to making more units available, the first order of priority is zoning reform. It does not need to be drastic either: Where rules allow single-family homes, for instance, reform could expand to build one extra unit within the same plot. Small buildings could be allowed in residential neighborhoods without disrupting their character, or livability. It is a goal that requires political will: convincing current owners and residents to support policies that expand the populations of their neighborhood is not an easy feat.

In some cases, especially in cities, updated regulations could also make it easier to convert units from commercial to residential, or make apartment buildings out of old hotels, as New York state has begun doing. This would maximize the existing inventory that is sitting empty and might prove especially valuable if there is a reduction in demand for commercial real estate as more companies continue to allow work from home. Local governments can also lower construction fees, which can be hefty—in some areas of California, for instance, they reach $100,000 per unit. These costs are passed down to owners or renters and could be easily reduced. Other measures, such as giving more incentives to the construction of affordable homes, using easier-to-built modular homes to bypass supply shortages, or helping first time buyers with down payments, can also address issues of inventory and consumers’ ability to access it.

But until these interventions are in place, with a severe shortage and interest rates around 7%, the situation is likely to get to a point where the buyers left cannot afford the few houses they can find, leading the market to stagnation.