Back to normal? Debt and the future of the US economy

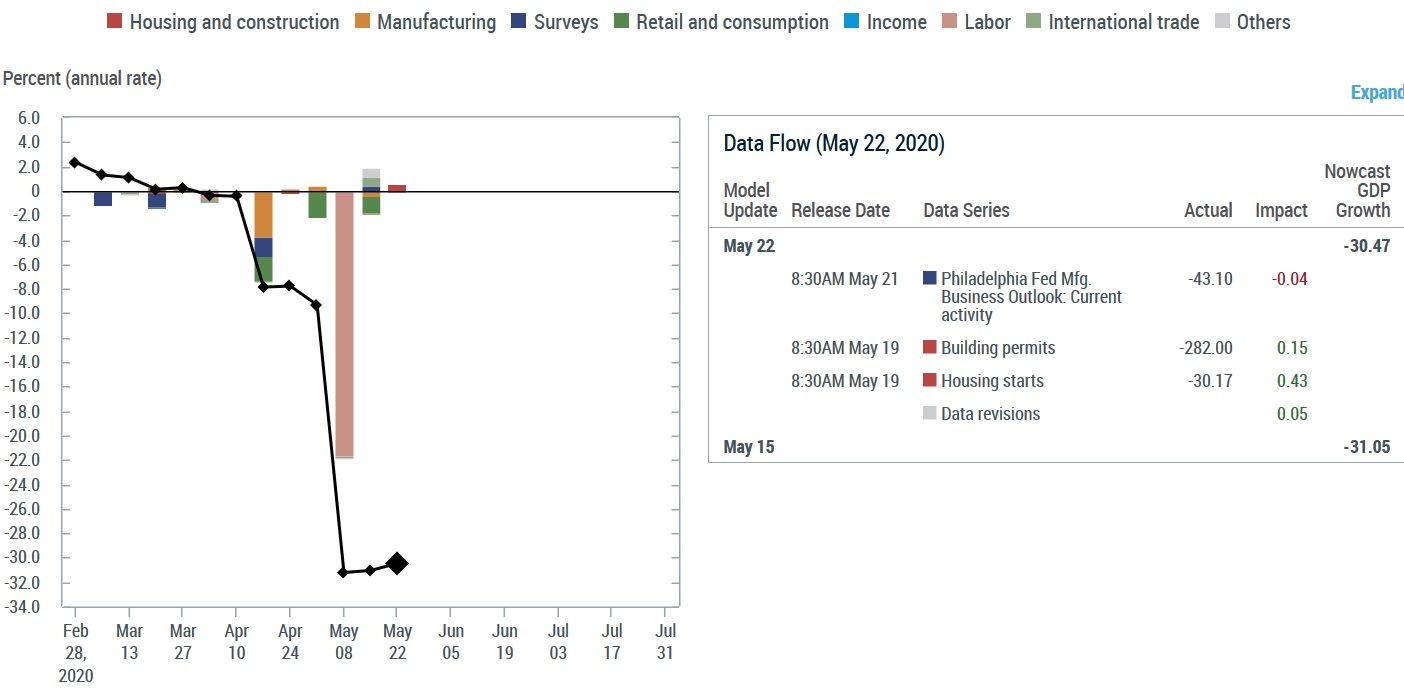

The COVID-19 pandemic has hurled the economy of the United States into the deepest downturn in decades, with unemployment approaching 1930s levels, and the drop in GDP even exceeding that of the Great Depression, according to the New York Fed’s current estimate of -31%. Most analysts expect growth to resume rapidly once the crisis subsides, but some important structural issues have now come to the fore, offering the opportunity to assess how well-equipped the US economy is to face the future.

President Donald Trump plans to run his re-election campaign on the claim that he already created the “best economy ever” once, so we should trust him to do it again after the crisis is over; a slight majority of Americans seem to agree, giving the president a 12-point margin over his likely rival Joe Biden on who would better the handle the economy. Major indicators did indeed show constant economic growth and unemployment officially at its lowest level in over 50 years until February of 2020. Yet these figures gloss over both a considerable amount of inequality – which has fueled “populist” political movements in the US and around the globe in recent years – as well as the precarious financial equilibrium of many areas of the economy, areas that in a certain sense represented bubbles just waiting to be popped.

One example of this phenomenon is the wave of debt-driven takeovers now exposing the shaky foundations of retail growth and the rental market, where the COVID-19 crisis has merely been the trigger for an emerging disaster. Two aspects are involved: 1) speculative financial mechanisms that extract value from the regular economy, and 2) the high cost of living for many citizens. Both of these factors will be exacerbated in the months and years to come by a reduction in consumption and an even greater increase of debt, absent policy changes to drive growth in a more sustainable direction.

Retail bankruptcies had already been on the rise in the United States in recent years. The New York Times recently highlighted how large retailers such as J. Crew and Neiman Marcus, which have filed for bankruptcy during the pandemic, had built up an enormous debt burden due to leveraged buyouts by private equity firms. Retailers provide a large stream of income for investors – in J. Crew’s case $760 million in dividends since 2011 – and then often go bust, costing thousands of jobs each time. The problem can’t be attributed to COVID-19; a “Retail Apocalypse” has been underway for years, demonstrating how once again, “financialization”, in which investors seek flows of short-term profits wherever available, is alive and well, with all of the related risks.

Another area where private equity is “wreaking havoc” is in the rental market. In recent years, large funds have been buying up apartment units around the United States – and in Europe, too – which of course means that they have to guarantee significant income streams to justify their investments; so they push out lower-income tenants, fueling a process of gentrification that drives up costs and makes it harder for the middle class to live close to where it works.

It’s all about making money fast: Blackstone, the world’s largest private equity firm, is now also the largest landlord for single-family rentals not only in the United States, but in the whole world. But loading up corporations with debt is a recipe for disaster: as we have seen repeatedly in the past, once the price rise in the underlying assets used to fuel speculation begins to wane, the collapse comes shortly afterwards, often with devastating consequences for the broader economy; just think of the sub-prime crash in 2007-2008.

Another area where a bubble is simply waiting to burst is that of consumer credit. In 2020, credit card debt reached an all-time high of $930 billion. What will happen now? On the one hand, close to a third of the workforce is suffering a sharp drop in income; on the other, investors have bet the future of the economy on continued income streams to pay off speculative debt.

The US Congress has moved quickly to get money flowing again, approving almost $3 trillion of spending in the past two months. That’s close to 14% of GDP, an enormous amount, which clearly presents political and administrative challenges to channel it to the most useful locations. This is supplemented by the actions of the Federal Reserve: after more than doubling in the fall of 2008, and doubling again between 2008 and the beginning of 2020, the central bank’s balance sheet – essentially a measure of how much money it injects into the economy – has jumped from slightly over $4 trillion to almost $7 trillion since just late February.

So public debt is also rising rapidly. The goal, as even many conservative economists admit today, must be to supplant private spending with public expenditures during the crisis. In Washington, though, it’s not hard to find those who are itching to pump the brakes on the current stimulus: Senate Republicans, as well as columnists in newspapers such as The Washington Post, seem to have gotten whiplash, and are now resisting new spending while awaiting the results of the initial reopening of the economy.

Cutting back on spending now would be a huge mistake. The gap to fill is enormous, and when the Fed monetizes the debt in a sovereign system, nobody needs to “pay it back“; the only requirements are to use the money to create tangible wealth, and avoid the creation of financial bubbles. It took a while, but even centrist Democrats have realized that the mistakes of 2009-2010 must be avoided; Joe Biden’s camp is now talking about an “FDR-size presidency“, while the big ideas of Elizabeth Warren and Bernie Sanders suddenly don’t seem so radical; it’s no time for a “return to normalcy”, Biden’s original message.

Yet even the notion of using government spending to hold down the fort until the economy resumes growing, is insufficient: the question is how to wield public tools to ensure that money goes to the right place. It’s one thing to prop up the securities markets, the Fed’s specialty over the past few decades; and quite another to take a New Deal approach to growing the economy: large-scale investment in infrastructure, promotion of productive industry, and a guarantee that those who are unemployed, or underemployed, can find well-paying jobs, rather than be exploited as low-cost labor to fuel bubbles that sooner or later result in widespread socio-economic carnage.

Some aspects of the CARES Act (The “Coronavirus Aid, Relief, and Economic Security” Act, passed in late March) go in the right direction: grants, not loans, to businesses, so they can not only make it through the crisis, but avoid being saddled with debt for years to come; and restrictions on how large companies can use the money they receive, such as the prohibition on stock buybacks and paying dividends. What remains is to use this opportunity to address the serious structural problems that have been papered over by speculative financial mechanisms even after the catastrophic crash of 2008. That means tightening restrictions on predatory financial practices, and directing investment towards productive areas of the economy.