The EU and the new frontiers of sustainability

The European Commission has recently chosen to defer the implementation of the Sustainable Finance Disclosure Regulation (SFDR) to January 1, 2023 and to change the EU taxonomy from a list of “sustainable activities” to a list of “transitional activities”. The two decisions anticipate the tough negotiations likely to be held in Egypt in November 2022 at the annual United Nations Climate Change Conference (the 27th annual Conference of the Parties or COP27).

The current transition year can serve investors and companies to arrive better prepared to the ESG (environmental, social and governance) reporting obligations and engagement, and to understand which are the next frontiers of ESG. There are three of such frontiers or main challenges: the first is to create a level playing field, the second is to achieve a reliable data framework, and the third is to measure impact.

Regarding a level playing field, investing in privately held companies and in companies that produce or outsource in certain permissive jurisdictions is a way to elude the reporting regulatory requirements and the increasing scrutiny of investors. A solution is to harmonize regulations. The compliance to the EU taxonomy and similar other regulatory frameworks should be extended to bank lending books and to non-pooled private equity and private credit investments. To harmonize regulations, single countries should agree on shared objectives, and this is what COP27 is expected to deliver.

Read also: An outlook on the green transition after COP26

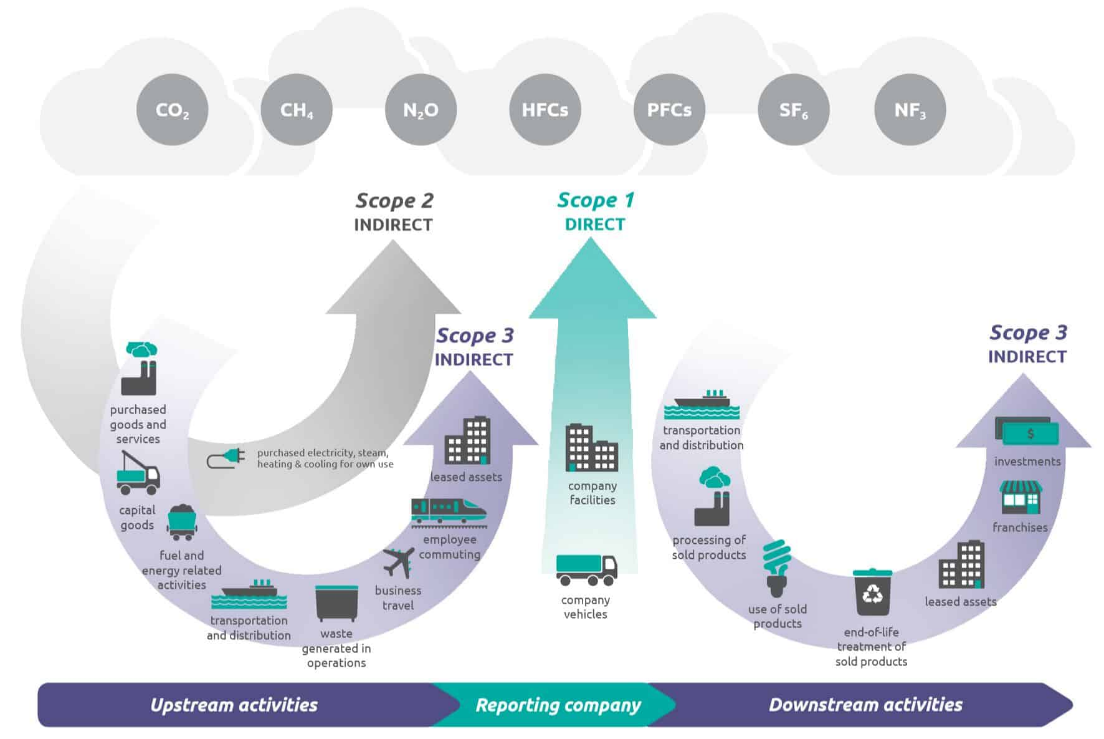

Taking advantage of both different jurisdictions and differences in reporting for public and private investments is intrinsically the same task: public companies disclose the geographical breakdown of their long-lived assets much better and more often than privately owned companies. Also, some companies can be ESG compliant while its privately held suppliers are not. The Greenhouse Gas Protocol already requires that companies break down the metrics for direct emissions (defined as Scope 1 emissions), indirect emissions (Scope 2 emissions), and emissions caused by its value chain (Scope 3 emissions). However, the companies have limited agency in demanding such data from suppliers, when not regarding a conflict of interest.

One might object that some publicly listed companies have off-balance sheet assets and liabilities that operate in breach of ESG principles. Due diligence should always incorporate the analysis of hidden assets and liabilities, including any off-balance sheet assets and liabilities. So professional investors can see that through, and it is a harder exercise when analyzing private equity and private credit, as well as bank loan books.

This year, some of the leading global general partners and limited partners have launched the ESG Data Convergence Project to create an initial standardized set of ESG metrics and mechanisms for comparative reporting. However, in the already crowded space of supranational organizations and accepted standards for ESG metrics, this initiative seems to avoid the comparison with the standards already in use by many publicly held companies.

Polluting or producing greenhouse gas emissions in certain countries has been historically easier than in others. If the COP27 leaders accept the same course for the future, they are deliberately choosing to drive high greenhouse gas-generating economic activities towards unregulated markets.

The second frontier is the importance of a reliable data framework. Now, we have little reliability on data. As the S&P Global Head of Sustainable Finance, Bernard de Longevialle, has recently told the Financial Times: “The risk is that it is garbage in, garbage out.”

It is relatively easy to make a comparison of the greenhouse gas needed to produce, operate, recycle and replace electric vehicles as opposed to combustion engines, but not all industries offer as many data points as the automotive industry.

Approximately 13,000 companies reported environmental data through the Carbon Disclosure Project (CDP) in 2021, as opposed to the 17,000, cumulatively worth $21 trillion, that are still failing to report.

There are several reporting frameworks and standards for ESG corporate disclosure, such as the CDP, the Climate Disclosure Standards Board (CDSB), the Global Reporting Initiative (GRI), the Sustainability Accounting Standard Board (SASB), the International Integrated Reporting Council (IIRC), the Task Force Climate-related Financial Disclosures (TCFD), and from the second half of 2022 the newly created International Sustainability Standards Board (ISSB). Such frameworks and standards are based on the United Nations’ Sustainable Development Goals defined in 2015.

While all the first ten companies in the 2021 CDP A-list have developed their environmental management systems based on the international standard ISO 14001, none of them have a certified system for the monitoring, quantification and verification of their greenhouse gas emissions, such as the ISO 14064. The founder of TCI (The Children’s Investment Fund Management, a value-based hedge fund), Chris Hohn, has highlighted the risk of greenwashing because some companies refuse to disclose emissions, but the next step of his “Say on Climate” initiative should also require that portfolio companies obtain independent verification for their emissions data.

Read also: Ensuring energy security in a carbon-free economy

The third challenge or frontier is to measure impact. I believe – and I am in the company of Harvard Professor George Serafeim on this topic – that the next frontier of sustainable investing is measuring impact.

The European Parliament and Commission have been using impact assessment studies for nearly 20 years in their decision making. Such studies gather qualitative and quantitative elements and employ operations research tools to score and quantify the impact of a certain legislative innovation on the whole spectrum of interested stakeholders, similarly to the way engineers establish traffic and its economic impact for an infrastructure project.

The co-founder of GMO (a leading asset-management firm), Jeremy Grantham, doubted earlier this year that a company’s only duty is to maximize profits legally for its shareholders. It can certainly be observed that many asset owners agree on minimizing inequalities and on stopping climate change: company executives will have to maximize profits within a more stringent regulatory framework that imposes considering all the stakeholders.

From 2023, the EU Sustainable Finance Disclosure Regulation (SFDR) deriving from the principles of the EU taxonomy should be applicable to MiFID II investment firms. It will take much longer for other countries to follow suit.

Until (i) countries harmonize regulations, (ii) generally accepted measuring and reporting standards emerge, and (iii) corporate strategies are accountable to the full spectrum of stakeholders, markets might offer exceptionally lucrative dislocations across several supply chains and industry verticals. For the three conditions to be met, domestic politics and international relations will have a fundamental role.