Natural gas: changing America and the world

Natural gas is in many ways the ideal fuel. It is abundant, affordable, clean-burning and extremely versatile. It can heat homes and offices, generate electricity from highly-efficient power plants, be used as a feedstock to manufacture chemicals and fertilizers, and replace more polluting forms of fuel to power vehicles of all sorts. Thanks to the shale revolution, the United States is now a net natural gas exporter, and US LNG can change the world for the better.

In the recent past, natural gas has often been seen as a premium fuel because of its relatively high cost. As a result, the use of natural gas has primarily been limited to developed economies (with some exceptions), while developing countries have tended to rely on coal (which is cheaper and more plentiful) to meet their growing energy needs.

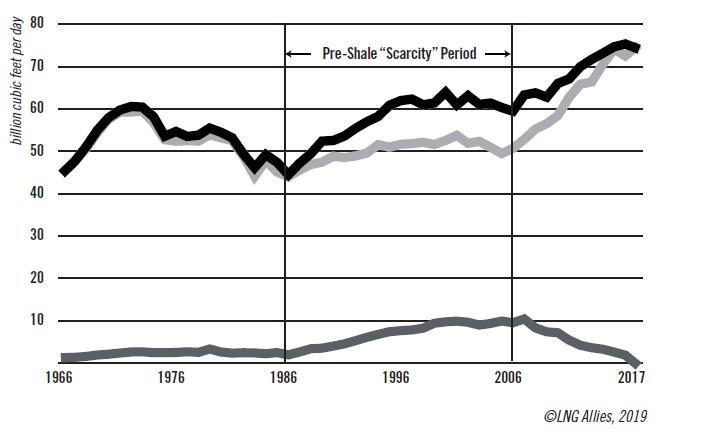

As shown in figure 1, from the mid-1960s to the mid-1980s US natural gas production and consumption were closely aligned. However, for the two decades beginning in 1986, demand increased faster than supply. As a result, substantial volumes of pipeline gas were imported to the United States from Canada, and 11 major terminals were built to import liquefied natural gas (lng) from countries such as Qatar, Nigeria and Trinidad.

Figure 1 – U.S. Natural gas Production, Consumption, Imports

THE SHALE REVOLUTION. This all changed with the US shale gas revolution. Starting in the mid-2000s, American hydrocarbon entrepreneurs began to combine two techniques — horizontal drilling and hydraulic fracturing — to extract first gas and later oil from shale formations in Texas, Louisiana, Pennsylvania, North Dakota, and other states. Since then, shale gas production has grown from a rarity to two-thirds of US production. Thanks to our success in “cracking the code” on shale, the United States surpassed Russia as the largest producer of natural gas in 2009 and became a net natural gas exporter in 2017.

As US gas production rose, there was little need to import higher-priced LNG and most of the US LNG import terminals were idled in the late 2000s. (The northeastern states remain an exception.) Subsequently, the owners of the LNG import terminals began to contemplate adding export capabilities to take advantage of the surging production of low-cost US shale gas. In July 2010, Cheniere Energy filed an application with the federal government to add liquefaction capabilities to its Sabine Pass facility in Louisiana. Applications from other import terminal owners soon followed.

Government approval is needed because the Natural Gas Act of 1938 requires authorization from the Federal Energy Regulatory Commission (FERC) – or from the US Maritime Administration (MARAD) in the case of a floating offshore facility – to construct an LNG export facility; it then requires authorization from the US Department of Energy (DoE) to export the gas itself.

Under United States law, LNG exports are presumed to be “in the public interest,” unless the DoE finds otherwise. For nations that have a free trade agreement (FTA) with the United States that includes the “national treatment of natural gas,” such exports are automatically deemed to be in the public interest and must be approved “without modification or delay.” For nations without ftas, the doe conducts a “public interest” review in which “interested parties” can express their views.

To support its public interest reviews, the doe commissioned six macroeconomic studies on LNG exports between 2012 and 2018. All six studies found that: 1) the macroeconomic benefits of LNG exports are “net positive” for the United States; 2) nearly all of the gas to be exported will come from additional production (rather than from domestic demand); and 3) the effect of LNG exports on prices to US natural gas users are minor.

REAPING THE BENEFITS. Currently, the doe has issued full (FTA+non-FTA) long-term export authorizations to the 14 major US LNG projects which have received a ferc or marad license, totaling almost 300 billion cubic meters per year (bcm/y). Under these authorizations, the only nations that cannot receive US LNG are those under sanctions (for example, Iran and North Korea).

Although US LNG exports from the contiguous 48 states only began in February 2016, the United States is already the third largest LNG exporter in the world, and the International Energy Agency (IEA) predicts that the United States will become the world’s leading LNG exporter by 2024, surpassing Australia and Qatar, the present top producers. Currently, there are eight LNG export projects in operation or under construction in the United States (six large terminals on the Gulf of Mexico and two smaller facilities on the East Coast), representing approximately 108 million metric tons per annum (mt/y) of capacity. Over the past year, the largest importers of US LNG have included Spain, France, the United Kingdom, Italy and the Netherlands.

ENHANCING GLOBAL ENERGY SECURITY. It was clear from the time that Cheniere filed its first export application that adding US LNG to the global energy mix could have important geostrategic implications. In granting its order to permit Cheniere to export LNG in May 2011, the doe stated: “An improvement in natural gas supplies internationally will help certain countries that currently have limited sources of natural gas supplies to broaden and diversify their supply base. This will contribute to greater overall transparency, efficiency, and liquidity of international natural gas markets, encouraging a liberalized global natural gas trade, and a greater diversification of global natural gas supplies.” US LNG exports meant improved energy security for America’s allies.

Still, there was significant opposition to US LNG exports, both from those who feared higher domestic natural gas prices as a result of exports (especially heavy industrial energy users such as chemical companies) and from environmental groups. Beginning in 2013, several governments from Central and Eastern Europe worked with leading US energy trade associations to form a coalition to ensure they could diversify their fuel sources by accessing US natural gas. This was how lng Allies was born, with the goal of ensuring continued, and faster, approvals of US LNG exports.

This effort was a success. In addition to the eight US projects being built, six more have been fully permitted (but have not yet taken a “final investment decision”), another eight are under formal environmental review at FERC, and four have received approval to enter the mandatory ferc pre-filing process.

US LNG exports already provide an alternative source of supply and pricing in the global natural gas market. They are reducing European reliance on Russian natural gas supplies and helping to stabilize global energy markets at a time when demand for US natural gas is expected to grow, particularly in Asia.

US LNG exports are also liberalizing the global natural gas market by fostering increased liquidity and reinforcing market forces. Since US LNG has “destination flexibility” and no exorbitant “take-or-pay” requirements, it is reordering international trade flows and challenging existing natural gas suppliers and business models. In response, other major gas suppliers (such as Qatar and Russia) have had to make their contracts more flexible, further strengthening the global market and giving customers more choice.

LNG SUPPLY AND DEMAND. At this juncture, it is difficult to predict how much additional US liquefaction capacity will be built. This will depend upon the growth of LNG demand worldwide, the availability of project financing, and other factors. However, the US Energy Information Agency’s 2019 Annual Energy Outlook estimated that US LNG exports could reach 14.5 billion cubic feet per day (bcf/d) by 2029 (about 148 bcm/y) in their “Reference Case,” and 22.7 bcf/d (about 232 bcm/y) in their “High Oil and Gas Resource and Technology Case.” (This High Oil and Gas Case has been the more accurate forecast in recent years.)

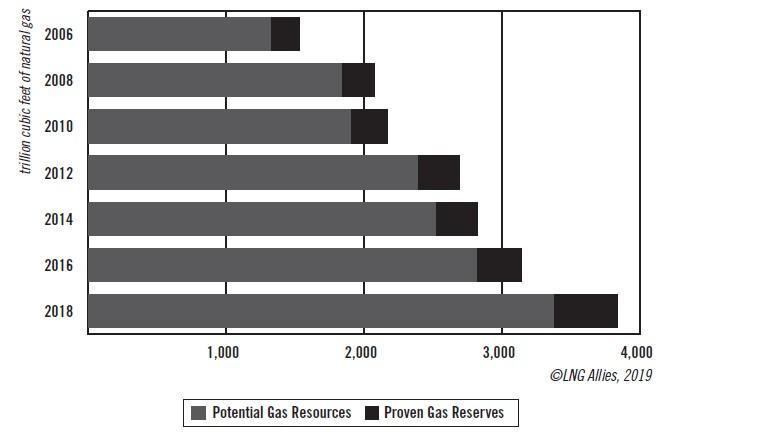

Fortunately, the United States has sufficient gas to meet domestic needs and support high levels of LNG exports without exhausting supplies or unduly raising prices at home. The Potential Gas Committee (PGC) — a group of 80 natural gas experts from industry, academia, and government — has been conducting biennial US natural gas surveys since 1964. The latest PGC assessment (September 11, 2019) found that the future supply of US natural gas at the end of 2018 stood at 3,838 trillion cubic feet (107 trillion cubic meters), an increase of 20% from the end of 2016. This is enough gas to meet domestic requirements and support robust exports for at least a century.

Figure 2 – U.S. Future Gas Supply (Resources + Reserves)*

All of this gas can be produced at low cost, meaning that US LNG will be very competitive with LNG producers elsewhere, as well as with natural gas supplied by pipeline in Europe. The 2019 Annual Energy Outlook estimated that Henry Hub prices[1] should stay below 4 dollars per million British thermal units[2] (mmbtu) through at least 2030 in their Reference Case and well below 4 dollars per mmbtu beyond 2050 in their High Oil and Gas Case, even as LNG exports increase significantly in coming years.

ENVIRONMENTAL BENEFITS. The human health and global environmental benefits from natural gas are profound. US LNG can help meet the energy access needs of the over 800 million people who do not have access to electricity today. It can also provide clean cooking fuel for many of the 2.7 billion people who cook over makeshift stoves or open fires (using charcoal, sticks or animal waste). This could help save some of the four million people who die each year as a result of indoor air pollution (a World Health Organization estimate).

Then there is outdoor air pollution, a health crisis in areas where higher-carbon fuels are still burned in old, inefficient power plants, which emit high levels of conventional pollutants, especially particulate matter. US LNG can help there, too. By significantly expanding the world’s supply of clean, low-cost natural gas, US LNG can lift millions of people out of poverty, clear the skies and save lives.

The US National Environmental Technology Laboratory (NETL) recently updated their work calculating the life cycle of greenhouse gas (ghg) emissions from US LNG as compared to pipeline gas and coal power in Europe and Asia. netl’s analysis indicates — as might be expected — that natural gas from any source is expected to have significantly fewer ghg emissions than coal for power generation in Europe or Asia. In addition, however, US LNG also compares favorably on a ghg emissions basis to Algerian LNG to Europe and Australian LNG to China; it would even result in lower ghg emissions than Russian pipeline gas to either Europe or China.

Other recent peer-reviewed studies found that life cycle ghg emissions from US LNG imported into India are 54% lower on average than emissions from Indian coal, and that North American LNG imported into China, India, Japan, South Korea and Taiwan reduced ghg emissions in all cases, up to a maximum reduction of 2.9 million tons of co2 equivalent for each million tons of LNG. The iea has estimated that up to 1.2 gigatons of co2 — or 10% of global power emissions — could be abated in the short term by switching from coal to existing gas-fired plants. Clearly, natural gas – including LNG – has an important role to play in combating both air pollution and climate change.

WHAT THE WORLD NEEDS NOW. Driven by population growth and economic progress, world energy use is expected to increase by 30% over the next twenty years; this is the equivalent of adding another China and India to today’s global energy demand. If this were not difficult enough, 80% of the projected growth in energy use will take place in developing nations, where coal is often the most readily available option.

While renewable energy may be the fastest growing source of supply in the coming years, solar and wind are intermittent sources and battery storage cannot substitute completely for all those times when the wind is not blowing and the sun is not shining. Therefore, the world needs for natural gas to remain an essential element of a powerful, low-carbon energy system.

US LNG is changing the world for the better, and the pace of change is likely to accelerate in the years ahead.

Footnotes:

[1] The Henry Hub is a distribution hub on the natural gas pipeline system in Erath, Louisiana. It interconnects with nine interstate and four intrastate pipelines. The settlement prices at Henry Hub are used as benchmarks for the entire North American natural gas market and parts of the global lng market.

[2] The British thermal unit is defined as the amount of heat required to raise the temperature of one pound of water by one degree Fahrenheit.