Many observers have recently announced or conjectured about the end of globalization. Such evaluation appears to be a gross generalization that is not confirmed by the current state of world trade. Despite the 2008 global financial crisis’s impact on trade and the more recent crisis related to the pandemic and to the Russian invasion of Ukraine, the theory of an upcoming end of globalization is not confirmed by data nor by economic and geopolitical considerations. At the same time, some changes in the speed and structure of global trade and countries interdependence appear plausible, mostly pushed by technology and by risk management and decarbonization policies.

In the last several decades, the world has gone through an increasingly fast process of globalization, meaning the growing international integration of markets for goods, services and factors of production (labor and capital). As a consequence of commodity market integration, prices of identical (or similar) commodities and goods in different country markets have tended to converge over time, contributing to growth in real incomes. Economists (with very few exceptions) have acknowledged the advantages of free trade, open capital markets, and international migration in producing an optimal allocation of the world’s resources. But while the economic benefits in the long run are generally agreed upon, many components of civil society fear globalization because of the fast changes it brings in the structure of national economies and a reduction in the living standards of some groups – while other groups and the economy at large gain.

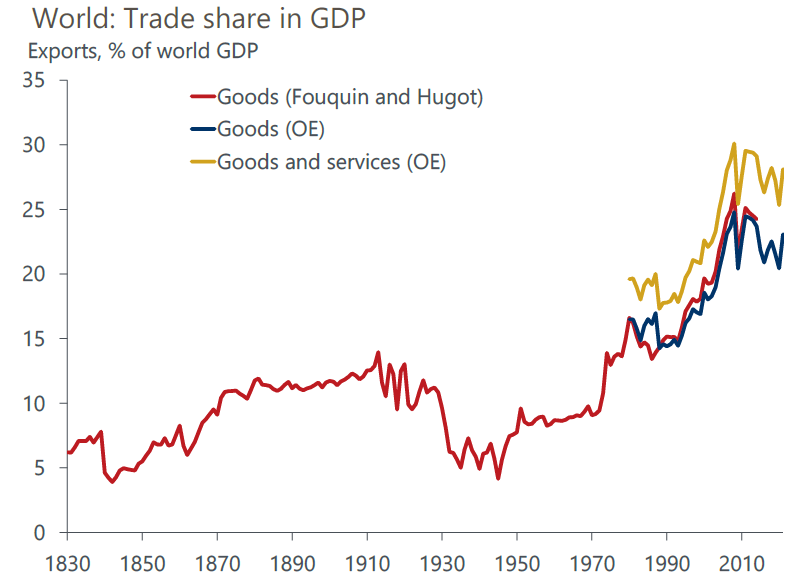

The globalization process has taken up speed and has become evident since China entered the World Trade Organization (WTO) in 2001. However, the process had already been in place at considerable speed in the previous decades and it was not at all a new phenomenon in history. As can be seen in Figure 1, major jumps in the exports share of GDP took place in the second half of the 1800s until World War I and then after World War II, in particular after 1975, after the collapse of the Bretton Woods system.

Globalization is not a new event in history

Although the process of international integration began with the opening up of the world in the Age of Discovery in the 16th Century, the major spurt in the pace of global integration through trade and capital markets opening did not really occur until after the Napoleonic wars. The growth of trade from 1500 to 1800 averaged a little over 1% per year, increasing to 3.5% between 1830 and 1914. This significant shift in international commodity market integration was mainly due to dramatic technological advancements in transport, as well as to big reductions in tariff protection (only partially reversed in the last decades of the 1800s).

Free trade gained pace across Europe (at the time the dominant economic global power) beginning with the Cobden Chevalier Treaty of 1860 between Britain and France. Within the next two decades most Europe countries reduced tariffs (to the 10-15% range from about 35%) with the adoption of bilateral agreements incorporating Most Favored Nation clauses. The liberalization process was reversed after 1879 with the introduction of tariffs by Germany and France, followed by other countries, under the pressure of landowners who were against declining wheat prices and land rents – although the level of effective protection (with the principal exception of the US) remained low until 1914.

Following World War I, nationalistic protectionist policies, the 1929 crisis and World War II, trade and globalization revived with the signing of GATT (General Agreement in Tariffs and Trade) institutionalizing the principles of open trade. However, despite an initial post-war jump, exports as a percent of GDP resumed the levels of the beginning of the 20th Century only in the mid-1970s, following the collapse of the Bretton Woods system of fixed (or quasi-fixed) exchange rates.

Also, international financial markets enjoyed two eras of globalization, from 1870 to 1914 and since 1973. The pace of international integration of finance follows a U-shaped curve,1 with integration interrupted by the imposition of capital controls and other impediments in the era of the World Wars, the Great Depression, and the Bretton Woods system.

The pendulum from free trade agreements to protectionism resulted historically from a cycle of market openings followed by reactions from the industry groups whose interests had been negatively affected. Today, following three decades of fast growth in trade and financial integration, it appears legitimate to ask whether the coming decades will see a return of protectionism and the end of globalization. So far, the developments witnessed in global trade point to a slowdown in the importance of trade as the engine of world growth, but not to a reverse in the process of integration.

Slowdown in globalization after the 2008 crisis

Globalization has slowed since the global financial crisis of 2008-2009 (see Figure 1), weighing on economic growth, especially in emerging market economies. The deceleration in globalization has in part been a natural economic outcome, reflecting industrial upgrading in some emerging markets, internalization of the environmental impact of transport, a shift of production closer to markets, and technological progress. But it also reflected policies that erected barriers to trade and investment, such as tariffs in the US-China trade war.

Economic globalization accelerated in the 1990s and 2000s with the burst occurring because of major trade liberalization, the opening of the former Soviet Union and Eastern European economies in the 1990s, China’s accession to the WTO in 2001, and rapidly falling costs of transport and communication. As supply chains for many products became global – with components crossing several borders before assembly stage – international trade expanded rapidly as a share of GDP. Other dimensions of increased economic interaction were the increasing share of traded services (financial, ICT and tourism in particular), rising foreign direct investment (FDI) and portfolio investment, migration and associated income flows.

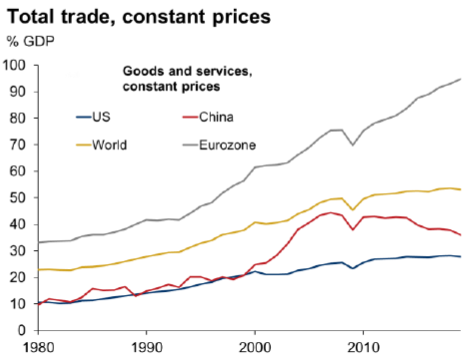

Since the global financial crisis, changes in economic and political dynamics have significantly slowed economic globalization, but less so than the headline numbers suggest. Some observers have concluded that globalization has already gone into reverse, with international trade having fallen as a ratio of global GDP since 2008. But that conclusion is based on data in current prices (Figure 2), which are affected by changes in relative prices. Prices of traded goods have substantially lagged those of non-traded ones, as one would expect from the convergence of global prices of traded goods and services.

As can be seen in Figure 2, in real terms the global total trade-to-GDP ratio rose 3.5 points to 53% in the decade following the crisis, compared to the average increase of approximately 10 points in each of the two preceding decades. In other words, the ratio of goods trade to GDP, while clearly slowing down, still edged up since 2010. International trade has risen as a share of GDP in the US and especially in the eurozone. But it has come down in China as its domestic economic growth has outpaced the global economy. A new trend in this period is that services trade was more resilient than goods trade and outpaced global GDP more significantly.

Indicators for other key aspects of international economic interaction also point to a slowdown in globalization. For example, after cross-border capital flows rose rapidly in the five years to 2007, reaching around 22% of global GDP, they plunged during the global financial crisis and have remained at more moderate levels since then, especially international bank lending. Inward FDI as a share of GDP lowered significantly around the world after 2010, except for Latin America. At the same time, some Asian emerging market economies have moved up the value chain and expanded their domestic supply chains. This has reduced their reliance on imported intermediate inputs.

The second set of reasons is less benign, involving policies to erect barriers to trade and investment. Globalization has been accused of being the main contributor to job displacement in developed countries, even though other factors have been more important, especially labor-saving technology such as robots. Governments should have responded by helping displaced workers upgrade their skills and find new jobs. Instead, the public backlash against economic globalization reduced the appetite of governments for further trade liberalization while protectionism and economic nationalism have gained momentum.

Read also: The waning of the Liberal Economic Consensus in the wake of the pandemic

The WTO noted just before the outburst of the pandemic that the rate at which new trade-restrictive measures were being put in place by its members was running at a historical high. This trend was not relative only to the USA-China trade conflict and barriers to trade and investment flows between other economies were also raised. The US and the EU have increased barriers to each other’s exports. The renegotiation of NAFTA (North American Free Trade Agreement), renamed USMCA (United States-Mexico-Canada Agreement), was pursued with import reduction and supply-chain repatriation as the main objectives of the US administration. Brexit has led to higher barriers to trade between Britain and the EU, its main trading partner.

Is deglobalization now happening?

After a decade of global trade being affected by such negative factors and policies, the COVID-19 pandemic first, and now the Russia-Ukraine war, have stepped up speculation about “deglobalization”, including economic decoupling of China from the US and its allies.

Read also: The impact of China’s economic slowdown on Transatlantic economies

Evidence of major decoupling so far is scant, especially outside the US, and some decoupling claims are clearly overblown. Some trade decoupling between the US and China has occurred since 2018 – the share of US imports from China has fallen from about 23% to 18%. But evidence of a broader impact outside sectors hit by US tariffs is harder to see, with little decoupling visible between China and other major trade partners, including the US’s allies in Europe and Asia. There has been a small drop in the share of Japan’s imports coming from China. In Canada, Europe and emerging Asia, however, the Chinese share in imports has grown – partly due to pandemic-related surges in demand for specific products.

Developments in the US electronics sector show that a significant reshuffling of supply chains and trade patterns is possible where trade restrictions are sufficiently strong – but most of the reshuffling in electronics and computing has been among import sources rather than towards domestic production, ending in a redirection instead of a reduction in global trade. Similarly, US-China FDI flows have shrunk, especially in the ICT sector, but there is little evidence of China being shunned as a global FDI destination as data of strong inflows in recent quarters have shown, with FDI into China almost regaining its 2013 historical peak level.

Heightened geopolitical risks could prompt some precautionary shifts in behavior by firms. Some surveys suggest some “reshoring” by US firms from China is occurring, but it is far from being significant.

Evidence from the American Chamber of Commerce in China for 2021 showed just 7% of firms shifting activity from China, and only 3% planning to move to the US. Some shifting of output away from China should be expected as a natural response to rising costs in China as it moves up the value chain. While global firms may be reluctant to engage in a costly reorientation of supply chains given China’s continued attractiveness as an investment location, their approach is likely to change in a structural manner.

After the lessons learnt from both the pandemic and the Russian invasion of Ukraine, a different approach of firms to global risk management of production locations and supply chains can be expected – and indeed welcome. Heavy dependence from one production site (or country) and/or from a specific supply chain have proved to be a major risk in the long term and the cases, among many others, of “Apple city” and Russian gas are simple striking evidence. However, such reorientation (for example, from China to other Far East or Latin American countries) does not imply that deglobalization is happening but only that the structure of the direction of trade may (not necessarily) change in the long term, not affecting volumes.

Other economic factors should be considered when calling for the end of globalization:

1. Russia clearly faces a major reorientation of its trade and financial links, but will have little impact on broader globalization trends, given the small size of its economy.

2. A potential “Asian” trade bloc is also unlikely to splinter world trade. Mutual trade between China, Russia and India amounted to just $200 billion in 2020, less than the total imports of countries like Thailand or Turkey. Even if that were to double or triple, it would remain a sliver of world trade. Moreover, China’s trade remains heavily oriented towards the US and its allies.

3. The dollar’s dominance as a global currency is unlikely to be threatened. Economies considering switching away from the dollar lack a credible alternative, with the dollar’s position cemented by the depth of US financial markets and the greenback’s dominance in global trade invoicing. The use of China’s renminbi as a global currency is low and has stagnated in the last few years

4. The possible redenomination of some oil trade flows into alternative currencies also poses little risk to the dollar. The oil trade represents only 10% of dollar-denominated trade flow globally, and the redenomination of a fraction of that, such as a portion of Saudi crude exports to China, would not put a serious dent in global dollar demand, should it occur.

In a nutshell, while to say “Much ado about nothing” may be premature, certainly the current evidence and economic analysis of the factors behind the slowdown in globalization do not confirm that the pendulum of world trade is moving in the direction of a closed and protectionist global environment.